8 min read

8 min read

-3.png)

When it comes to purchasing a home, it is also about going for a home at affordable pricing, and this is where the question comes in- can you buy a foreclosure with an FHA loan? In short, yes, one can buy a home at a lesser price but also make use of FHA loan to purchase foreclosed properties. This is helpful especially if the purchased home meets certain standards set by the Federal Housing Administration.

FHA mortgage is an ideal source of finances that enables buyers with moderate income, limited savings, or a lower credit score to purchase a home. However, with purchasing a foreclosed home, there comes adequate challenges depending on if the property is sold as it is or has certain significant repairs.

Let us see how FHA financing works for a foreclosure to ensure there are no delays, unexpected expenses, and financing issues at the time of buying a property.

An FHA loan to buy foreclosure functions just as one would finance a traditional home purchase. This loan is backed by the Federal Housing Administration, which enables lenders to provide a flexible approval standard to borrowers.

FHA loans also enable buyers to possess their own property by making them eligible for foreclosed properties provided they meet the required borrower requirements while the property meets FHA property standards.

In comparison to conventional loans, FHA financing offers:

Given these benefits, most homebuyers go for standard FHA loans when planning to buy a foreclosure.

A foreclosed home is a type of property that has been taken over by a bank or lender because the previous owner could not keep up with mortgage payments. The properties seized by lenders are then listed for sale to recover the unpaid loan amount.

One can find many foreclosures through:

Few buyers also consider foreclosure opportunities given they are sold at relatively lower price in comparison with surrounding properties. The property condition differs in how the former owner has maintained it.

One can purchase a home with an FHA loan but it must meet specific eligibility conditions.

FHA appraisal is an important aspect that determines the market value. The appraiser also assesses if the home meets basic safety and livability standards under FHA guidelines.

This means the home should generally have:

However, if the home is in poor condition, lenders may also decline financing until the repairs are completed first, hence making few foreclosed properties qualify for FHA financing and few others do not.

Buyers

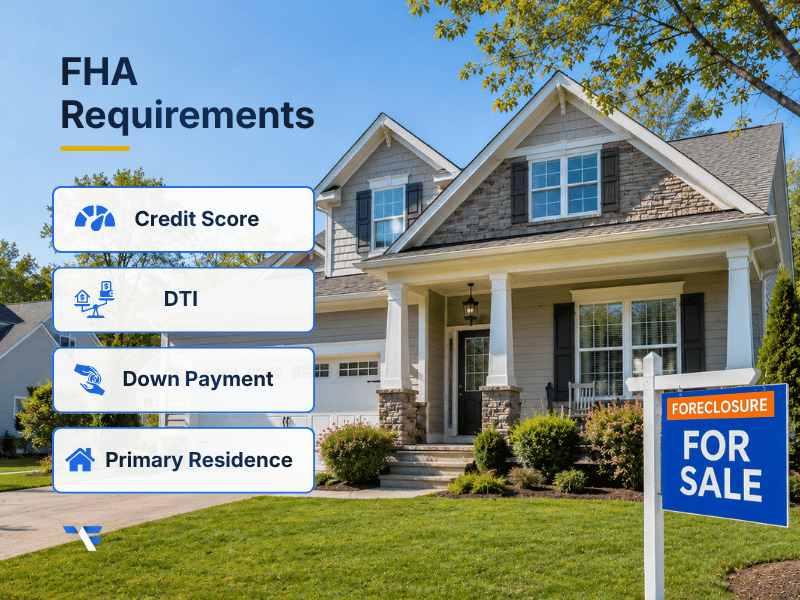

To qualify for a foreclosure with an FHA loan, borrowers must meet FHA loan requirements.

Credit Score Requirements

A minimum credit score must be met which is defined by a lender. Several FHA programs have relatively lower credit score requirements, which makes them attractive for borrowers who do not qualify for conventional financing.

Debt to Income Ratio

A borrower’s debt to income ratio defines the monthly debt obligations to one’s income. Most lenders calculate this raptor to estimate if the borrowers can manage the mortgage payments.

Down Payment Requirements

Using an FHA loan is beneficial given the lower upfront payment requirements. These borrowers can qualify for smaller down payment which makes home buying easy.

Primary Residence Rules

FHA financing is meant for primary residence alone and not any vacation or investment home.

While FHA loan has its own advantages but a foreclosure can still have its own challenges.

Properties Sold as Is

Most homes are sold as is which means the seller cannot complete any necessary repairs before closing. For homes that fail FHA inspection standards, financing becomes complicated.

Significant Repairs

Certain foreclosures may include major significant repairs, which includes roof replacement, plumbing updates, or fixing structural damage. This makes meeting FHA eligibility guidelines difficult.

Competition from Other Buyers

foreclosure properties are commonly preferred by investors and cash buyers given their relatively lower price.

Delays with Bank-Owned Properties

Most banks handling foreclosures move gradually at the time of negotiation. This is why it’s essential to collaborate with an experienced agent who knows well about foreclosure transactions to navigate the process more efficiently.

Preparation is equally important when planning to buy a foreclosed home.

Work with the Right Professionals

It is essential to partner with an experienced real estate agent and knowledgeable loan officers to identify eligible properties and avoid homes that fail FHA standards.

Get Pre-Approved Early

When looking for real estate listings, one must obtain pre-approvals from an FHA-approved lender enabling one to identify their budget.

Review Property Requirements Carefully

Every foreclosure may not satisfy FHA property requirements. It is recommended to review inspection findings when considering the purchase.

Budget for Closing Costs and Repairs

Buyers must also consider the closing costs along with the home's purchase price. Along with this, possible repairs, insurance, and lender-related expenses such as lender fees must also be factored for.

FHA and conventional financing are both apt for purchasing foreclosures. However, the right choice of loan depends on the borrower’s financial situation.

An FHA loan works well for borrowers looking for:

Conventional loans are ideal for buyers who are looking to buy homes that require lesser repairs. This type of loan is also apt for borrowers with stronger financial profiles.

Choosing the right financing solution depends on the condition of the property, the buyer’s budget, and long-term goals.

For many buyers, the answer to ‘Can you buy a foreclosure with an FHA loan?’ is encouraging. FHA financing can provide a practical path toward homeownership, especially for borrowers looking for flexible approval standards and lower upfront costs.

However, foreclosure purchases require careful evaluation. Property condition, FHA appraisal standards, financing timelines, and repair needs all play an important role in determining whether the purchase will move forward smoothly.

At Truss Financial Group, buyers can explore financing guidance tailored to different homeownership situations, including foreclosure opportunities and FHA-backed financing solutions that align with their long-term goals.

1. Can you buy a foreclosure with an FHA loan if the property needs repairs?

Yes, but the property must still meet FHA minimum safety and livability standards. Homes with major issues may require repairs before approval.

2. What credit score is needed for an FHA foreclosure loan?

The required credit score can differ based on the lender, but FHA programmes are known for having lower credit score requirements than many conventional loan programs.

3. Are FHA loans only for first-time buyers?

No. FHA financing is available to eligible buyers who meet program guidelines, even if they have owned property before.

4. Do foreclosed homes always cost less?

Not always. While some foreclosures are sold at a lower price, competition from other buyers can increase the final purchase amount.

5. Why do some foreclosures fail FHA appraisal requirements?

Some homes may have safety concerns, incomplete systems, or structural damage that prevent them from meeting FHA standards.

Take your pick of loans

Experience a clear, stress-free loan process with personalized service and expert guidance.

Get a quote

14 min

-1.jpg?width=352&name=Blog%20covers%20(6)-1.jpg)

7 min

.png?width=352&name=xxxxxx%20header%20(57).png)

16 min

Discover your borrowing power and plan your mortgage journey with knowledge on your side.

Get a quoteGet a quote in 3 easy steps

Tell us what you want

Fill out our online form to help us understand your financial situation and loan needs.

We get to work for you

We review your info and look for competitive rates that match your specific goals.

You get a personalized quote

You’ll receive a customized rate quote that meets your unique profile.