4.6 from 700+ reviews

4.6 from 700+ reviews

4.6 from 700+ reviews

For many homeowners in Arizona, home equity represents one of their largest financial assets. A reverse mortgage offers a way to access that equity without selling the home or taking on monthly mortgage payments. This option is particularly valuable for retirees looking to supplement income, manage expenses, or improve financial flexibility during retirement.

At Truss Financial Group, we help Arizona homeowners understand how reverse mortgages work and whether they align with their long-term financial goals.

How a Reverse Mortgage Works

A reverse mortgage allows homeowners aged 62 or older to convert a portion of their home equity into cash. Unlike traditional mortgages, borrowers are not required to make monthly payments. Instead, the loan balance increases over time and is repaid when the home is sold, the borrower moves out, or passes away.

The most common type is the Home Equity Conversion Mortgage (HECM), which is federally insured and regulated. Funds can be received in multiple ways, including lump sum payments, monthly payouts, or a line of credit.

Key Features of Reverse Mortgages

| Feature | Description |

| Monthly Payments | Not required |

| Loan Repayment | Due upon sale, move-out, or death |

| Ownership | Borrower retains ownership |

| Disbursement Options | Lump sum, monthly payments, or line of credit |

| Age Requirement | 62+ |

Arizona Home Values and Reverse Mortgages

Arizona’s real estate market has experienced steady growth, particularly in cities like Phoenix, Scottsdale, and Tucson. Rising home values mean many homeowners now have substantial equity available.

This increase in equity makes reverse mortgages more accessible and potentially more beneficial. The higher the home value, the greater the amount a borrower may be eligible to receive, subject to lending limits and age factors.

Additionally, Arizona’s popularity among retirees makes reverse mortgages a common financial planning tool in the state.

Eligibility Requirements

To qualify for a reverse mortgage in Arizona, borrowers must meet certain criteria established by lenders and federal guidelines.

Basic Eligibility Criteria

| Requirement | Details |

| Minimum Age | 62 years or older |

| Home Ownership | Must own the home or have significant equity |

| Primary Residence | Property must be primary residence |

| Financial Assessment | Ability to maintain property taxes and insurance |

| Property Type | Single-family, FHA-approved condos, or eligible homes |

Borrowers are also required to complete a counseling session with a HUD-approved advisor to ensure they fully understand the terms and implications.

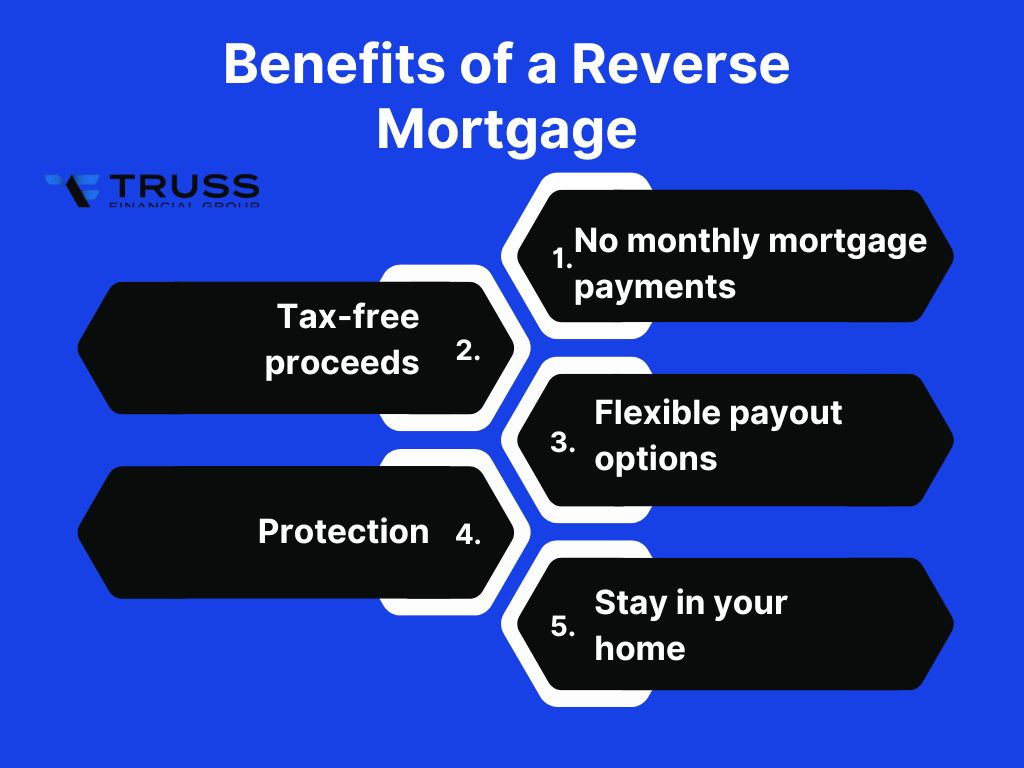

Benefits of a Reverse Mortgage

Reverse mortgages offer several advantages, particularly for retirees seeking financial stability without selling their homes.

They provide access to tax-free cash, which can be used for daily expenses, healthcare, home improvements, or debt repayment. Since no monthly mortgage payments are required, they can significantly improve cash flow during retirement.

Another key benefit is flexibility. Borrowers can choose how they receive funds, allowing them to tailor the loan to their financial needs. Additionally, reverse mortgages are non-recourse loans, meaning borrowers or their heirs will never owe more than the home’s value.

Risks and Considerations

While reverse mortgages offer flexibility, they are not suitable for everyone. It is important to understand the potential risks before making a decision.

Interest accrues over time, increasing the loan balance and reducing home equity. Borrowers are still responsible for property taxes, insurance, and maintenance, and failure to meet these obligations can lead to loan default.

Additionally, reverse mortgages may impact inheritance, as the home is typically sold to repay the loan. Fees and closing costs can also be higher compared to traditional mortgages.

Careful evaluation and professional guidance are essential before proceeding.

Jumbo Reverse Mortgages in Arizona

For homeowners with high-value properties, jumbo reverse mortgages, also known as proprietary reverse mortgages, offer an alternative to standard HECM loans.

These loans are designed for homes that exceed FHA lending limits, allowing borrowers to access a larger portion of their equity.

Standard vs. Jumbo Reverse Mortgages

| Feature | HECM (Standard) | Jumbo Reverse Mortgage |

| Loan Limits | FHA limits apply | Higher loan amounts |

| Insurance | Federally insured | Not FHA-insured |

| Ideal For | Average home values | High-value properties |

| Flexibility | Moderate | Greater loan access |

Jumbo reverse mortgages can be particularly beneficial in Arizona markets with higher property values.

Reverse Mortgage Example in Arizona

Understanding how a reverse mortgage works in practice can provide clarity.

Example Scenario

| Detail | Value |

| Home Value | $500,000 |

| Borrower Age | 70 |

| Estimated Loan Access | $200,000 – $300,000 |

| Payment Option | Line of credit or monthly payments |

The exact amount depends on factors such as age, interest rates, and equity. Older borrowers and higher home values typically result in higher loan eligibility.

Reverse Mortgage Refinancing

Refinancing a reverse mortgage may be an option if home values increase or interest rates improve. By refinancing, borrowers may access additional equity or secure better loan terms.

However, refinancing involves new closing costs and should be evaluated carefully to ensure it provides a net benefit.

Is a Reverse Mortgage Right for You?

A reverse mortgage can be a valuable financial tool, but it depends on individual goals and circumstances.

It may be suitable if you plan to stay in your home long-term, need additional income during retirement, or want to reduce financial stress without selling your property.

However, it may not be ideal if you intend to move in the near future or want to preserve maximum home equity for heirs.

Consulting with experienced professionals, like the team at Truss Financial Group, can help you make an informed decision based on your financial situation.

Frequently Asked Questions

Do I lose ownership of my home?

No. You retain ownership as long as you meet loan obligations such as taxes and insurance.

Are reverse mortgage funds taxable?

No. Funds received from a reverse mortgage are generally tax-free.

Can I sell my home if I have a reverse mortgage?

Yes. You can sell the home at any time, and the loan will be repaid from the sale proceeds.

What happens to the loan after I pass away?

The loan is repaid through the sale of the home. Any remaining equity goes to your heirs.

Are there monthly payments?

No monthly mortgage payments are required, but you must maintain property-related expenses.

Start Your Journey in 3 Simple Steps

Getting started with a reverse mortgage in Arizona is straightforward with the right guidance. At Truss Financial Group, we begin by evaluating your home equity, financial needs, and long-term goals to determine if a reverse mortgage is the right fit. Next, we walk you through available options—whether it’s a standard HECM or a jumbo reverse mortgage—ensuring complete clarity. Finally, we guide you through a smooth application and closing process, so you can access your home equity with confidence and peace of mind.

Get the information you need to make confident decisions

Discover your borrowing power and plan your mortgage journey with knowledge on your side.

Get a quote- No documents required

- No commitment

- No commitment

Get a quote in 3 easy steps

Tell us what you want

Fill out our online form to help us understand your financial situation and loan needs.

We get to work for you

We review your info and look for competitive rates that match your specific goals.

You get a personalized quote

You’ll receive a customized rate quote that meets your unique profile.