4.6 from 700+ reviews

4.6 from 700+ reviews

4.6 from 700+ reviews

5 Key Features of This Article:

![]() Describes how asset depletion loans enable borrowers to qualify on savings and investments in lieu of traditional income.

Describes how asset depletion loans enable borrowers to qualify on savings and investments in lieu of traditional income.

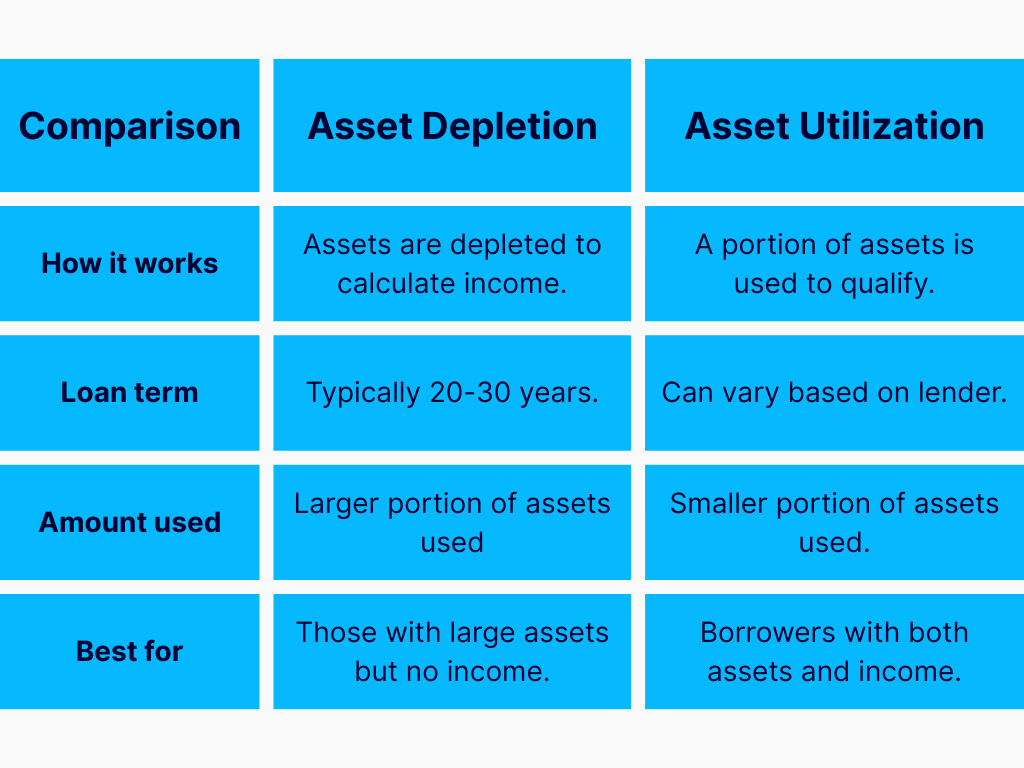

![]() Contrasts asset depletion against asset utilization with a concise, easy-to-read chart.

Contrasts asset depletion against asset utilization with a concise, easy-to-read chart.

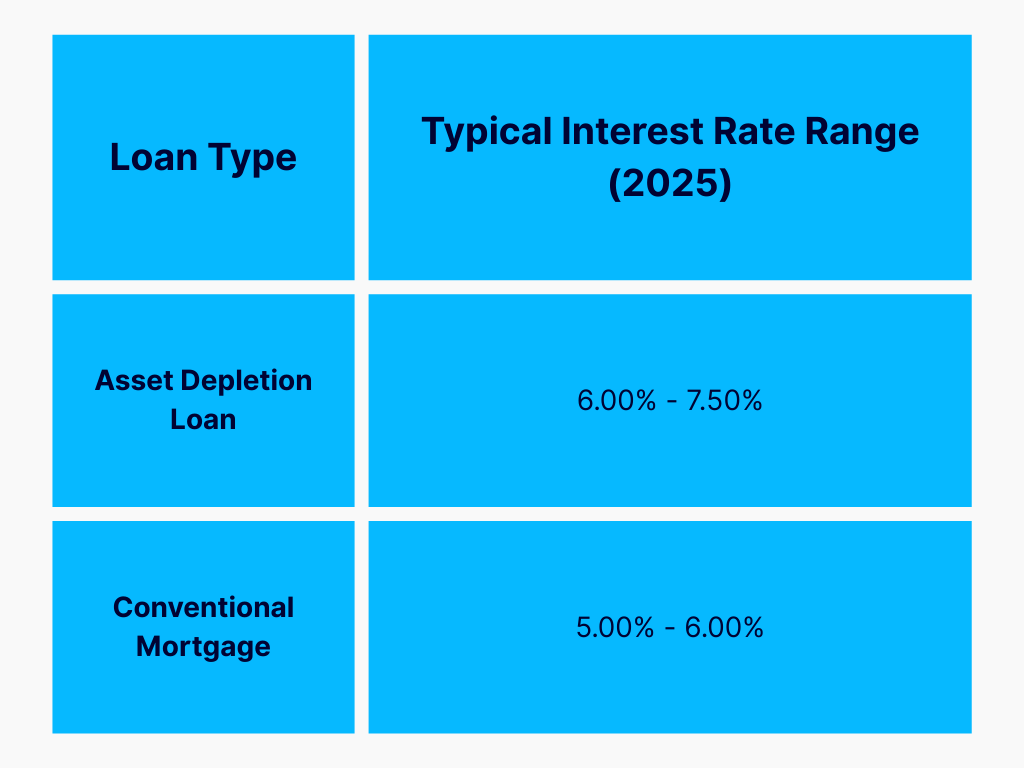

![]() Includes 2025 LOS interest rates and adjusted eligibility for California.

Includes 2025 LOS interest rates and adjusted eligibility for California.

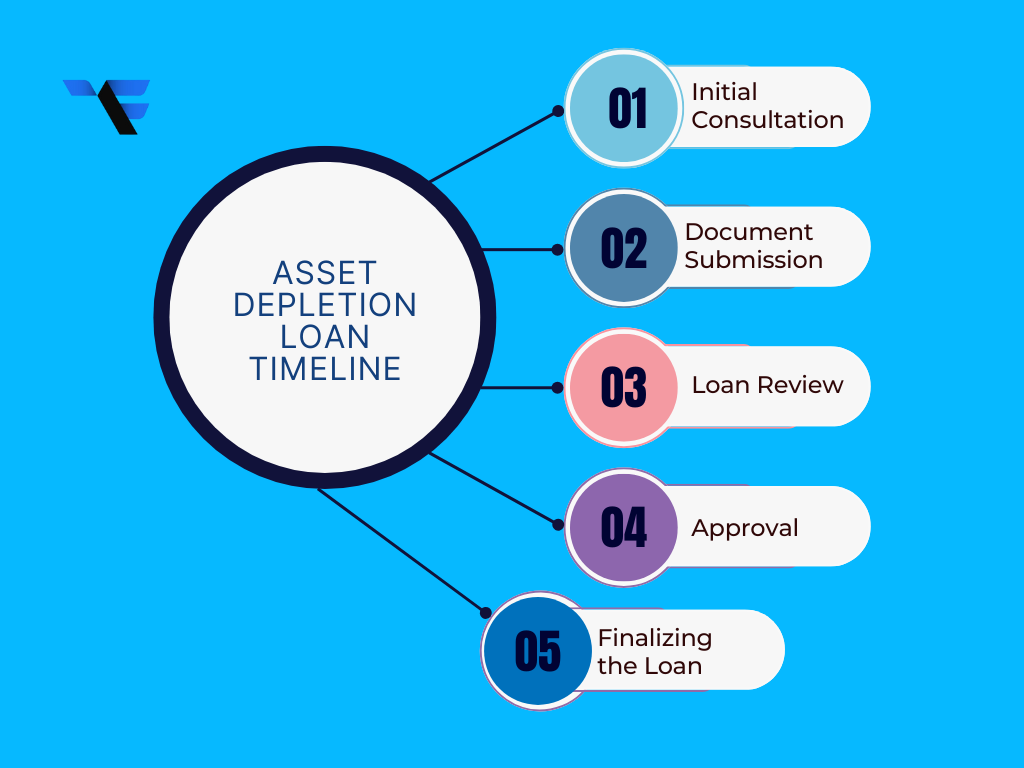

![]() Provides a basic step-by-step loan process, from consultation to the final approval.

Provides a basic step-by-step loan process, from consultation to the final approval.

![]() Provides lists of pros and cons that will enable people to determine if this type of loan is a fit for their situation.

Provides lists of pros and cons that will enable people to determine if this type of loan is a fit for their situation.

Asset depletion loans give borrowers the ability to use their non-liquid assets, such as retirement and investment accounts, to qualify for a mortgage. These loans can be helpful for borrowers without traditional income, such as retirees or the self-employed. In California, where home prices tend to be expensive, asset depletion loans can provide housing for people who have the wealth but lack the income to qualify for a mortgage.

What are Asset Depletion Loans?

An asset depletion loan is another type of mortgage, one that allows you to qualify with your assets instead of your income. In this case, it calculates your income based on any assets you own, including non-liquid assets like savings, retirement accounts, or investments. It can be an excellent choice for borrowers who are quite wealthy but whose income stream is irregular.

For example, if you have a large retirement fund and various investments but no traditional monthly income, an asset depletion loan enables you to use those assets to qualify for a mortgage. Lenders essentially calculate an annual income based on the total value of your assets, which helps you secure the loan.

Asset Depletion vs. Asset Utilization

It's essential to understand the difference between asset depletion and asset utilization when considering your mortgage options:

- Asset Depletion: This method calculates a "deemed" income from your assets. Your total assets are divided by a specific number (usually 20 or 30 years) to calculate an annual income. This income is then used to determine how much you can borrow.

- Asset Utilization: Asset utilization involves using a percentage of your assets directly to qualify for the loan. For example, if you have $1 million in assets, the lender may allow you to use a percentage of that value to count toward your loan qualification.

Key Features of Asset Depletion Loans

- No Need for Traditional Income: These loans are ideal for those who don’t have regular income, such as retirees or business owners who rely on assets instead of a steady paycheck.

- Asset-Based Calculation: The lender calculates your income based on your assets. This means you can use savings, retirement accounts, and other investments to qualify.

- Longer Loan Terms: Asset depletion loans often offer longer repayment terms, typically 20 to 30 years, which helps keep monthly payments manageable.

- Flexible Asset Use: Various assets can be used to qualify, including stocks, bonds, real estate, and retirement accounts.

Asset Depletion Loan Rates in California

As of 2025, interest rates for asset depletion loans are typically higher than for traditional loans. This is due to the fact that asset depletion loans don’t rely on regular income, which represents a higher risk for the lender. However, these loans can still offer a competitive alternative for borrowers with substantial assets.

The interest rates for asset depletion loans generally range from 6.00% to 7.50%, while conventional mortgage rates are typically between 5.00% and 6.00%.

Asset Depletion Loan Timeline in California

Getting an asset depletion loan in California follows a similar process to a traditional mortgage, but with some differences. Here’s a general timeline:

- Initial Consultation (1-2 days): This step involves meeting with a loan officer to review your financial situation and determine if an asset depletion loan is right for you.

- Document Submission (1-2 weeks): You’ll need to provide documentation, such as account statements for your retirement funds, investment portfolios, and tax returns.

- Loan Review (2-3 weeks): The lender reviews your assets and calculates your income equivalency based on your total assets. They may also verify your credit score and overall financial standing.

- Approval (2-3 weeks): After reviewing the necessary documents, the lender either approves or denies the loan. Once approved, they will present you with the loan terms.

- Finalizing the Loan (1 week): After approval, you’ll sign the necessary documents, and the loan will be finalized. You’ll then be able to move forward with purchasing or refinancing your home.

Asset Depletion Loan Limits in California

The amount you may borrow with asset depletion loans is generally determined by the value of your assets. You can usually borrow as much as 80% of that value of your assets. Still, your loan limits may vary depending on the asset type, your credit profile, and the lender’s criteria.

Instead, a lender may agree to lend you some portion of your home’s value or sales price based on your remaining retirement, but they’ll probably put a maximum limit on it. If, for instance, you had $1 million in retirement savings and $500,000 of other assets, they may be willing to let you take out a loan for part of that, but not all that cash.

Pros and Cons of Asset Depletion Loans

Pros

- No Traditional Income Required: If you don’t have a regular paycheck or other consistent income, asset depletion loans allow you to qualify based on your assets.

- Ideal for Retirees or Self-Employed: This loan is beneficial for people who rely on savings or investments rather than a regular salary.

- Larger Loan Amounts: If you have significant assets, you can often qualify for a larger loan compared to traditional mortgages.

Cons

- Higher Interest Rates: These loans tend to come with higher interest rates because they are considered higher risk for lenders.

- Not for Everyone: Asset depletion loans are best for individuals with substantial assets but no regular income. They may not be the right fit for everyone.

- Limited Availability: Not all lenders offer asset depletion loans, so you may need to shop around to find the best deal.

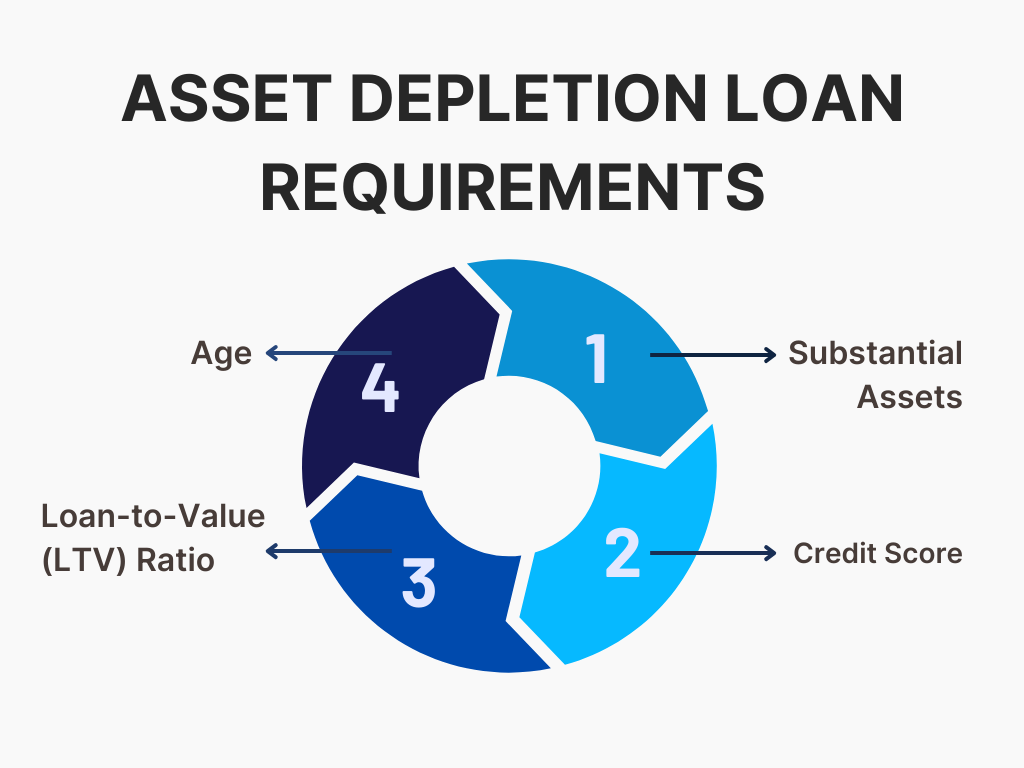

Asset Depletion Loan Requirements in California

To qualify for an asset depletion loan in California, you generally need to meet the following requirements:

- Substantial Assets: You must have a significant amount of non-liquid assets such as retirement accounts, stocks, bonds, or other investments.

- Credit Score: Most lenders will require a minimum credit score of 620, but a higher score can help you secure better terms.

- Loan-to-Value Ratio (LTV): Lenders often require an LTV ratio of 80% or lower for asset depletion loans. This means you may need a down payment of at least 20% depending on the value of your home.

- Age: There is no specific age limit for asset depletion loans, but lenders may consider your age when evaluating your assets.

Best Asset Depletion Loans in California

When looking for the best asset depletion loan, it’s important to choose a lender who understands your financial situation and can help you navigate the process. Truss Financial Group specializes in offering asset depletion loans with competitive rates and personalized service.

We offer:

- Competitive interest rates for asset depletion loans.

- Flexible loan options tailored to your specific needs.

- An efficient and straightforward loan application process.

Frequently Asked Questions

What is the minimum DTI ratio for an asset-based loan?

Most lenders prefer a debt-to-income (DTI) ratio of 45% or lower. However, some flexibility may exist depending on the borrower’s assets and overall financial profile.

Is there an age limit for asset-based mortgages?

There is no specific age limit. However, lenders may take age into account when evaluating your assets.

Do you have to be retired to use retirement accounts as assets?

No, you do not need to be retired to use your retirement accounts as assets. As long as you have access to the funds in those accounts, they can be used to help qualify for an asset depletion loan.

Conclusion

An asset depletion loan would be one of the best options for borrowers in California with a lot of assets but who do not have traditional income. If you’re a retiree or self-employed, these loans can enable you to become eligible for a mortgage. If you believe an asset depletion loan is best for your needs, then contact Truss Financial Group today to schedule a consultation and understand your options.

Get the information you need to make confident decisions

Discover your borrowing power and plan your mortgage journey with knowledge on your side.

Get a quote- No documents required

- No commitment

- No commitment

Get a quote in 3 easy steps

Tell us what you want

Fill out our online form to help us understand your financial situation and loan needs.

We get to work for you

We review your info and look for competitive rates that match your specific goals.

You get a personalized quote

You’ll receive a customized rate quote that meets your unique profile.