4.6 from 700+ reviews

4.6 from 700+ reviews

4.6 from 700+ reviews

Key Features

- Learn what a bank statement loan is and how it helps people who don’t have W-2s or regular pay stubs.

- Understand the types of bank statement loans you can get in Florida, including refinance and low down payment options.

- Learn what lenders look for in your bank statements and how far back they check.

- We’ll walk you through how to apply and how fast you can close on your home.

- Find out who qualifies, what the benefits are, and how to get the best rate possible

What Is a Bank Statement Loan and How Does It Work?

A bank statement loan is a mortgage designed for people who are self-employed or don’t receive a regular paycheck. Instead of using tax returns or W-2s to prove income, lenders review your recent bank statements, usually from the last 3 to 12 months. They look at your deposits to understand how much money you make and how consistent your income is. If the numbers show you earn enough to afford the loan, you can get approved without traditional proof of income.

This loan is a good option in Florida for business owners, gig workers, and freelancers who want to buy a home or refinance but don’t qualify the usual way.

What Your Bank Statements Reveal to Lenders

When you apply for a bank statement loan, lenders use your bank records to understand your income. They check how much money you deposit each month and how steady that income is. They also look for regular business activity, like client payments or sales. If they see large or steady deposits, it shows you can afford your mortgage payments. Your spending habits, fees, and account balance also help lenders decide if you’re financially responsible.

Bank Statements vs. Credit Card Statements: Key Differences

Bank statements and credit card statements look similar, but they show different things. A bank statement tracks your deposits, withdrawals, and overall cash flow, it shows the money you actually have. A credit card statement, on the other hand, shows what you’ve borrowed and spent using credit. Lenders prefer bank statements for this type of loan because they prove how much money you earn, not how much you owe. That's why credit card statements aren’t used to qualify for bank statement loans.

Explore the Different Types of Bank Statement Loans in Florida

There’s no one-size-fits-all when it comes to bank statement loans. In Florida, borrowers have several flexible options depending on their needs, income history, and goals. Whether you're buying a new home, refinancing, or tapping into home equity, there's likely a bank statement loan that fits. Truss (a.k.a. TFG) is a mortgage broker and lender specializing in non‑qualified mortgages (Non‑QM) tailored for self‑employed individuals and real estate investors

Refinance Options Using Bank Statements

If you already own a home, you can use a bank statement loan to refinance. This means replacing your current mortgage with a new one, often with a better rate or terms. You might also choose a cash-out refinance, which lets you take money out of your home’s value. You don’t need tax returns, just strong bank statements to prove your income.

Qualify With Just 3 Months of Bank Statements

Some lenders in Florida accept as little as 3 months of bank statements to qualify you. This is a great option if you’re newer to self-employment or recently started earning more. The lender will check that your deposits are steady and high enough to cover a mortgage payment.

Bank Statement Loans With as Little as 5% Down

You don’t always need a large down payment. Some bank statement loan programs allow you to buy a home with as little as 5% down. That makes it easier to get into a home without saving for years. Your loan size will depend on your income, credit, and how much you can afford.

HELOCs Based on Bank Statement Income

A home equity line of credit (HELOC) lets you borrow from your home's value when you need it, like a credit card. Some lenders offer HELOCs based on your bank statement income. If you’re self-employed and need flexible cash access, this can be a smart way to get funds without refinancing your main mortgage.

Today’s Bank Statement Loan Rates in Florida

Interest rates for bank statement loans are usually a bit higher than regular loans, but they vary by lender. Your rate will depend on your credit score, loan amount, and how much you’re putting down. Checking rates early can help you plan and compare the best offers.

What You Need to Qualify for a Bank Statement Mortgage in Florida

Getting approved for a bank statement mortgage is often easier for self-employed people than going through a traditional loan. But there are still some rules you’ll need to meet. Lenders want to see that you make enough money, have steady deposits, and manage your finances well.

Minimum Bank Statement Requirements

Most lenders ask for 12 to 24 months of personal or business bank statements. However, some may accept just 3 to 6 months if your income is strong. These statements should show regular deposits that match what you earn from your work or business. You may also need to show your business license, profit and loss statement, or other documents that confirm your income is real and stable.

How Far Back Lenders Look at Your Statements

Lenders usually check your most recent 12 months of bank statements, but some programs allow as little as 3 months. The more history you can show, the better your chances of getting approved. They’ll look for steady deposits, not big one-time payments, and make sure your income is enough to cover the loan.

Who Typically Benefits From This Type of Loan?

Bank statement loans are ideal for self-employed workers, freelancers, gig workers, and small business owners. If your tax returns don’t reflect your real income, or if you write off a lot of expenses, this loan helps you still qualify based on your actual cash flow. It's also great for people with strong savings or large deposits but no traditional paycheck.

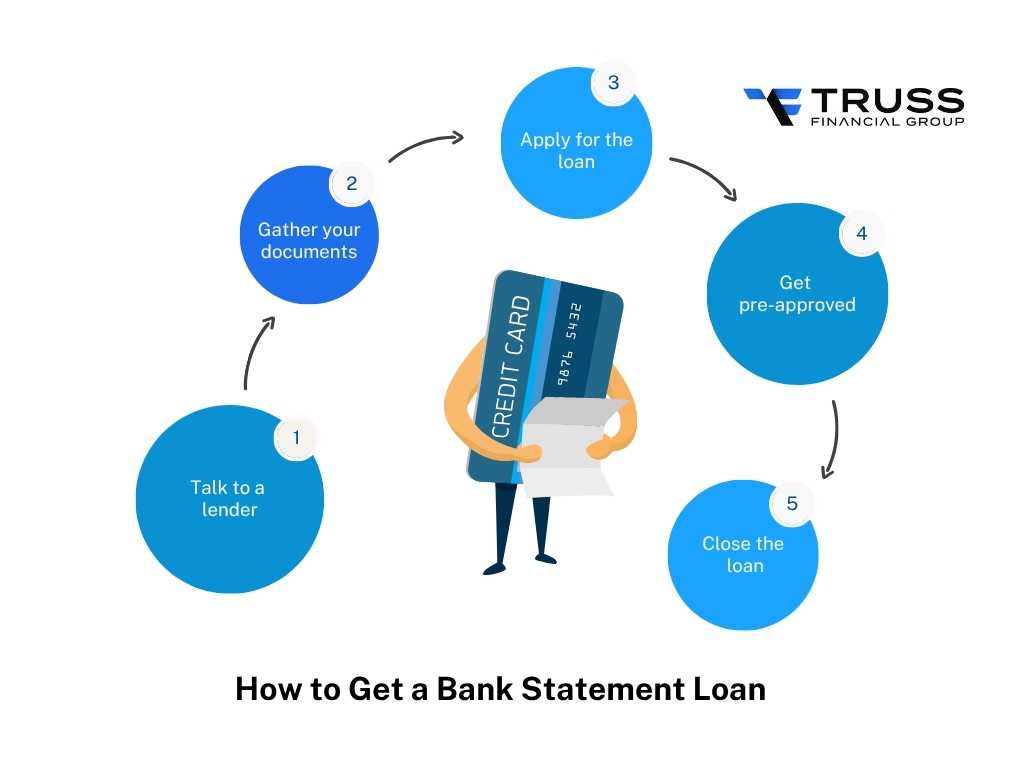

Step-by-Step: How to Get a Bank Statement Loan in Florida

Getting a bank statement loan in Florida is a great option if you’re self-employed or have non-traditional income. The process is simpler than you might think. Instead of showing W-2s or tax returns, you’ll just need to prove your income through your bank statements. Here's a quick look at how the steps usually go:

- Talk to a lender – Start by speaking with a loan expert to see if a bank statement loan is right for you.

- Gather your documents – You’ll need recent bank statements, usually from the last 3 to 12 months.

- Apply for the loan – The lender reviews your income, credit score, and financial history.

- Get pre-approved – Once approved, you’ll know how much home you can afford.

- Close the loan – After the final paperwork, your loan is funded and the home is yours (or your refinance is complete).

The entire process is designed to be flexible and fast, especially for buyers in Florida who need a non-traditional path to homeownership.

Timeline to Close: How Fast Is the Process?

Most bank statement loans can close in 21 to 30 days, which is similar to a regular mortgage. If you have your documents ready and respond quickly to your lender, the process can move even faster. Delays usually happen when paperwork is missing or bank statements need extra review.

Tips for Securing the Lowest Rate

Getting a good interest rate on your bank statement loan can save you thousands over time. Here are smart steps you can take to help lower your rate:

- Keep your credit score strong.

Even though these loans focus on your bank statements, your credit score still matters. A higher score shows you’re responsible with money. Try to pay off debts, avoid late payments, and keep your credit card balances low before applying. - Show steady income in your bank statements.

Lenders like to see regular deposits that show your income is stable. If your bank statements are clean, no overdrafts, large gaps, or bounced payments, you’re more likely to get a better offer. - Save for a bigger down payment.

The more money you put down, the less risk the lender takes. A larger down payment can lead to a lower rate and possibly better loan terms. - Keep your debt low.

Lenders check your debt-to-income ratio. If you already have a lot of monthly payments, like car loans, credit cards, or other mortgages, it can raise your rate. Paying down some debt before you apply can help. - Shop around and ask questions.

Not all lenders offer the same rates or terms. It’s okay to compare offers and ask questions. At Truss Financial Group, we’ll help you understand your options and find the best fit for your situation.

Need Help With Your Bank Statement Loan? Find Out If You Qualify Today

Not sure where to start? That’s okay. Truss Financial Group can walk you through it and check if you qualify. We’ll review your bank statements, talk through your goals, and help you build a plan that works.

Top Advantages of Bank Statement Mortgage Loans

Bank statement loans offer real benefits for people who don’t get a traditional paycheck. One of the biggest advantages is flexibility, you don’t need to show W-2s or tax returns, just your bank deposits. This helps self-employed people, freelancers, and small business owners qualify based on their actual income.

You can also get a loan with fewer roadblocks, like limited paperwork and faster approval times. Some programs allow for low down payments, starting at just 5%. Plus, these loans can be used to buy a home, refinance your current mortgage, or even take cash out if you qualify. It’s a powerful tool for those who earn well but don’t fit the usual lending box.

Understanding Your Home Equity: Can You Use It With a Bank Statement Loan?

Yes, you can use your home equity with a bank statement loan, especially through a cash-out refinance or a HELOC (Home Equity Line of Credit). Equity is the value of your home minus what you still owe. If your home is worth more than your loan balance, you may be able to borrow against that value.

For example, if your Florida home is worth $500,000 and you owe $300,000, you might access up to $200,000 in equity. With a bank statement loan, the lender checks your income through deposits, not tax forms. That means even if you write off a lot on your taxes, you can still tap into your equity if your statements show enough income.

Beyond Bank Statement Loans: Other Non-QM Mortgage Options

Bank statement loans are just one type of non-QM (non-qualified mortgage). Non-QM loans are designed for people who don’t meet the standard rules for regular mortgages.

Here are a few other types:

- Asset-based loans: Use your savings, stocks, or other assets to qualify instead of income.

- No-ratio loans: Don’t require lenders to check your income or debt at all.

- DSCR loans: Used by real estate investors, based on how much income the rental property makes.

- 1099 loans: Great for contractors or gig workers who get paid with 1099 forms.

If a bank statement loan isn’t the best fit, there may be another non-QM option that works for your situation.

Ready to See If You Qualify for a Bank Statement Loan in Florida?

You don’t have to figure this out on your own. At Truss Financial Group, we help self-employed buyers across Florida get approved without the usual income paperwork. If you’ve been told “no” by a bank because you don’t have W-2s or perfect tax returns, we may have a solution that fits you.

Talk to a loan expert today, and we’ll take a look at your bank statements, credit score, and goals. Your dream home or refinance might be closer than you think.

FAQ: Bank Statement Loans in Florida

How do I apply for a bank statement loan in Florida?

Start by talking to a lender that offers bank statement loans, like Truss Financial Group. They’ll ask about your income, business type, and home loan goals. You’ll then provide your bank statements (usually 3 to 12 months), along with basic documents like ID and credit info. If everything checks out, you’ll be pre-approved and can move forward with your loan.

How many months of bank statements are required?

Most lenders ask for 12 to 24 months of bank statements, but some may accept as few as 3 or 6 months. It depends on your income and the lender’s rules. The goal is to show steady deposits that prove you earn enough to cover your mortgage.

Is it difficult to get approved for a bank statement mortgage?

It’s often easier than getting a regular loan if you're self-employed. You don’t need W-2s or tax returns, just solid bank records. As long as your statements show strong income and your credit is in good shape, approval is very possible. A lender will guide you through each step.

How can I get the best interest rate on a bank statement loan?

To get the lowest rate, keep your credit score high, make steady deposits, and avoid overdrafts. A larger down payment can also help lower your rate. It's also smart to compare offers from different lenders to find the best deal.

Get the information you need to make confident decisions

Discover your borrowing power and plan your mortgage journey with knowledge on your side.

Get a quote- No documents required

- No commitment

- No commitment

Get a quote in 3 easy steps

Tell us what you want

Fill out our online form to help us understand your financial situation and loan needs.

We get to work for you

We review your info and look for competitive rates that match your specific goals.

You get a personalized quote

You’ll receive a customized rate quote that meets your unique profile.