4.6 from 700+ reviews

4.6 from 700+ reviews

4.6 from 700+ reviews

Key Takeaways

![]() Texas mortgage rates remain competitive in 2025, with median home prices around $350,000 and annual appreciation of 4-6% creating strong investment potential.

Texas mortgage rates remain competitive in 2025, with median home prices around $350,000 and annual appreciation of 4-6% creating strong investment potential.

![]() Truss Financial Group offers specialized mortgage solutions for diverse situations including self-employment, military service, and first-time homebuyers across all Texas regions.

Truss Financial Group offers specialized mortgage solutions for diverse situations including self-employment, military service, and first-time homebuyers across all Texas regions.

![]() No state income tax and strong homestead protections make Texas homeownership particularly advantageous compared to other states.

No state income tax and strong homestead protections make Texas homeownership particularly advantageous compared to other states.

![]() Down payment assistance programs are available for qualified Texas homebuyers, with options requiring as little as 3% down for conventional loans.

Down payment assistance programs are available for qualified Texas homebuyers, with options requiring as little as 3% down for conventional loans.

![]() Property taxes significantly impact monthly payments in Texas, typically adding about 30% to your principal and interest payment.

Property taxes significantly impact monthly payments in Texas, typically adding about 30% to your principal and interest payment.

______________________________________________________________________

Expert Texas Mortgage Solutions Since 2006

- Rising interest rates that require strategic financing

- Competitive markets in cities like Austin and Dallas

- Property tax considerations that affect your total monthly payment

- Special programs for first-time buyers and veterans

What are the Areas We Serve in Texas

Major Metropolitan Areas

Growing Suburban Communities

- North Texas: Frisco, Plano, McKinney, and Allen

- Houston Area: The Woodlands, Sugar Land, Pearland, and Katy

- Austin Region: Round Rock, Cedar Park, Georgetown, and Leander

- San Antonio Area: New Braunfels, Boerne, and Schertz

Rural Texas Locations

- USDA Rural Development Loans: Zero-down options for qualifying rural properties

- Farm and Ranch Loans: For properties with agricultural components

- Large Acreage Financing: Options for properties with significant land

- Remote Property Considerations: Solutions for homes in less-populated counties

What are Our Texas Mortgage Programs?

We offer a variety of mortgage solutions tailored to the unique needs of Texas homebuyers. Whether you're a first-time buyer, self-employed professional, or military veteran, we have options to fit your situation.

Mortgage Options for Every Texas Homebuyer

Whether you're a first-time buyer, self-employed professional, real estate investor, or retiree, we have options designed specifically for your situation.

Conventional Loans - Popular for good-credit borrowers with down payments starting at 3%. These conventional loans offer competitive rates and fewer restrictions than government-backed options. Ideal for Texas homebuyers with stable income and strong credit profiles looking for long-term financing.

FHA Loans - Perfect for first-time buyers with down payments as low as 3.5%. FHA loans work well for buyers with credit scores as low as 580 who need more flexible qualifying guidelines. These government-backed mortgages provide an accessible path to homeownership for many Texas families.

Bank Statement Loans - Designed for self-employed Texans. Instead of complex tax returns, we use your bank deposits to qualify you. Ideal for business owners, freelancers, and gig workers with variable income. These specialized loans recognize your true earning capacity beyond what appears on tax returns.

Stated Income Loans - Modern alternatives to traditional income verification for qualified Texas borrowers. These loans allow certain borrowers to qualify based on declared income with alternative verification methods. Ideal for commission-based professionals, seasonal workers, and others with complex income structures. Today's stated income options include stronger verification safeguards than pre-2008 versions while still providing flexibility.

DSCR Loans - For Texas real estate investors. These loans qualify based on the property's rental income potential rather than your personal income. Buy investment properties without the traditional income documentation hassle. DSCR loans require the property's income to cover the mortgage payment with a ratio of 1.0 or higher.

Asset Depletion Loans - For retirees and high-net-worth individuals. We calculate your loan eligibility based on your assets rather than monthly income. These programs convert your investment portfolios, retirement accounts, and liquid assets into theoretical income for qualification purposes.

Jumbo Loans - For high-value Texas properties that exceed conforming loan limits. These loans feature competitive rates with specialized options for luxury homes. Our jumbo programs offer financing up to $5 million with flexible terms for Texas' premium real estate markets. We provide jumbo options for primary residences, second homes, and investment properties with customized solutions for complex financial situations.

Home Equity Lines of Credit (HELOCs) - Flexible financing that lets Texas homeowners tap into their equity as needed. HELOCs work like a credit card secured by your home, allowing you to borrow, repay, and borrow again during the draw period. Perfect for home improvements, debt consolidation, education expenses, or creating a financial safety net. Texas HELOCs follow specific state regulations including 80% combined loan-to-value limits and mandatory waiting periods.

Reverse Mortgages - Designed for Texas homeowners aged 62 and older. Reverse mortgages allow you to convert home equity into tax-free cash without monthly mortgage payments. These FHA-insured loans provide retirement funding while allowing you to remain in your home. We also offer proprietary jumbo reverse mortgages for high-value properties exceeding FHA limits.

Fix and Flip Loans - Specialized short-term financing for Texas real estate investors purchasing distressed properties for renovation and resale. These loans fund both acquisition and renovation costs with loan terms typically ranging from 6-24 months. Our fix and flip programs feature streamlined approval processes, flexible property condition requirements, and competitive rates based on experience level.

VA Loans - Exclusive financing for veterans, active duty service members, and eligible surviving spouses. VA loans offer 100% financing with no mortgage insurance and competitive rates. Texas has one of the nation's largest veteran populations, and we proudly serve those who've served our country with specialized VA loan expertise.

|

Loan Type |

Minimum Down Payment |

Minimum Credit Score |

Best For |

Special Features |

|

Conventional |

3-5% |

620+ |

Borrowers with good credit |

Lower PMI, cancelable after 20% equity |

|

FHA |

3.5% |

580+ |

First-time buyers, lower credit scores |

More flexible credit requirements |

|

VA |

0% |

Typically 620+ |

Veterans, active military |

No PMI, competitive rates |

|

USDA |

0% |

640+ |

Rural and some suburban areas |

Income limits apply |

|

Bank Statement |

10-15% |

620+ |

Self-employed borrowers |

Uses bank deposits instead of tax returns |

|

DSCR |

20-25% |

640+ |

Real estate investors |

Based on property's rental income |

|

Jumbo |

10-20% |

680+ |

Luxury properties |

Exceeds conforming loan limits |

Texas-Specific Mortgage Advantages: Why you should invest?

Texas Veteran Home Loan Programs

What are Texas Home Buying Requirements?

1. Credit Score Requirements for Texas Mortgages

2. Texas Down Payment Options and Assistance Programs

- Texas Homebuyer Program - Offers up to 5% of your loan amount as down payment assistance for qualified buyers.

- My First Texas Home - Provides competitive fixed-rate mortgage loans and down payment assistance to first-time buyers and veterans.

- Texas Mortgage Credit Certificate - Offers a tax credit up to $2,000 annually while you own and live in your home.

- Local Programs - Many Texas cities and counties offer their own assistance programs for residents, including Dallas, Houston, Austin, and San Antonio.

3. Current Mortgage Interest Rates in Texas

- Credit score - Higher scores receive better rates

- Loan-to-value ratio - Larger down payments typically secure lower rates

- Loan type - Government-backed loans may offer lower rates for qualified borrowers

- Property type - Primary residences usually receive better rates than investment properties

- Loan term - 15-year mortgages generally have lower rates than 30-year terms

- Points - You can pay points upfront to lower your interest rate

Texas Income Verification Process

- Recent pay stubs (typically covering 30 days)

- W-2 forms from the past 2 years

- Federal tax returns for the past 2 years

- Verification of employment from your employer

- Tax returns from the past 2 years with all schedules

- Year-to-date profit and loss statement

- Business tax returns if you own 25% or more of a business

- Bank Statement Loans - 12-24 months of personal or business bank statements instead of tax returns

- Award letters for Social Security, disability, or pension income

- Divorce decree for alimony or child support

- Lease agreements for rental income

- Documentation of investment income

Property Types Eligible for Financing in Texas

Understanding Texas Property Taxes and Homeownership Costs

- Own and occupy the home as your primary residence

- Submit an application to your county appraisal district

- Apply by April 30th following your purchase (though late applications are accepted up to one year after the deadline)

How Property Taxes Impact Your Monthly Payment?

- Principal - Portion of payment reducing your loan balance

- Interest - Cost of borrowing the money

- Taxes - Property taxes collected monthly

- Insurance - Homeowners insurance (and possibly PMI)

- Principal and Interest: ~$1,770/month

- Property Taxes (~1.8%): ~$525/month

- Insurance: ~$175/month

Total Monthly Payment: ~$2,470

- Tax rates vary widely—even between neighboring communities

- Newer developments often have higher tax rates to fund infrastructure

- Some areas have multiple overlapping taxing authorities

- Homes in tax-heavy districts can have lower purchase prices but higher monthly costs

Insurance Requirements for Texas Homeowners

- Mortgage companies require sufficient coverage to protect their investment

- Typically demands replacement cost coverage (not actual cash value)

- May require specific endorsements based on property location

- For loans with less than 20% down, private mortgage insurance (PMI) adds another monthly cost

- Multiple-deductible policies are common, with separate deductibles for hail, wind, or named storms

- Some areas require specific certifications for windstorm coverage

- Many insurers offer discounts for impact-resistant roofing, security systems, and newer homes

- Shopping among multiple carriers is essential, as rates can vary by thousands for identical coverage

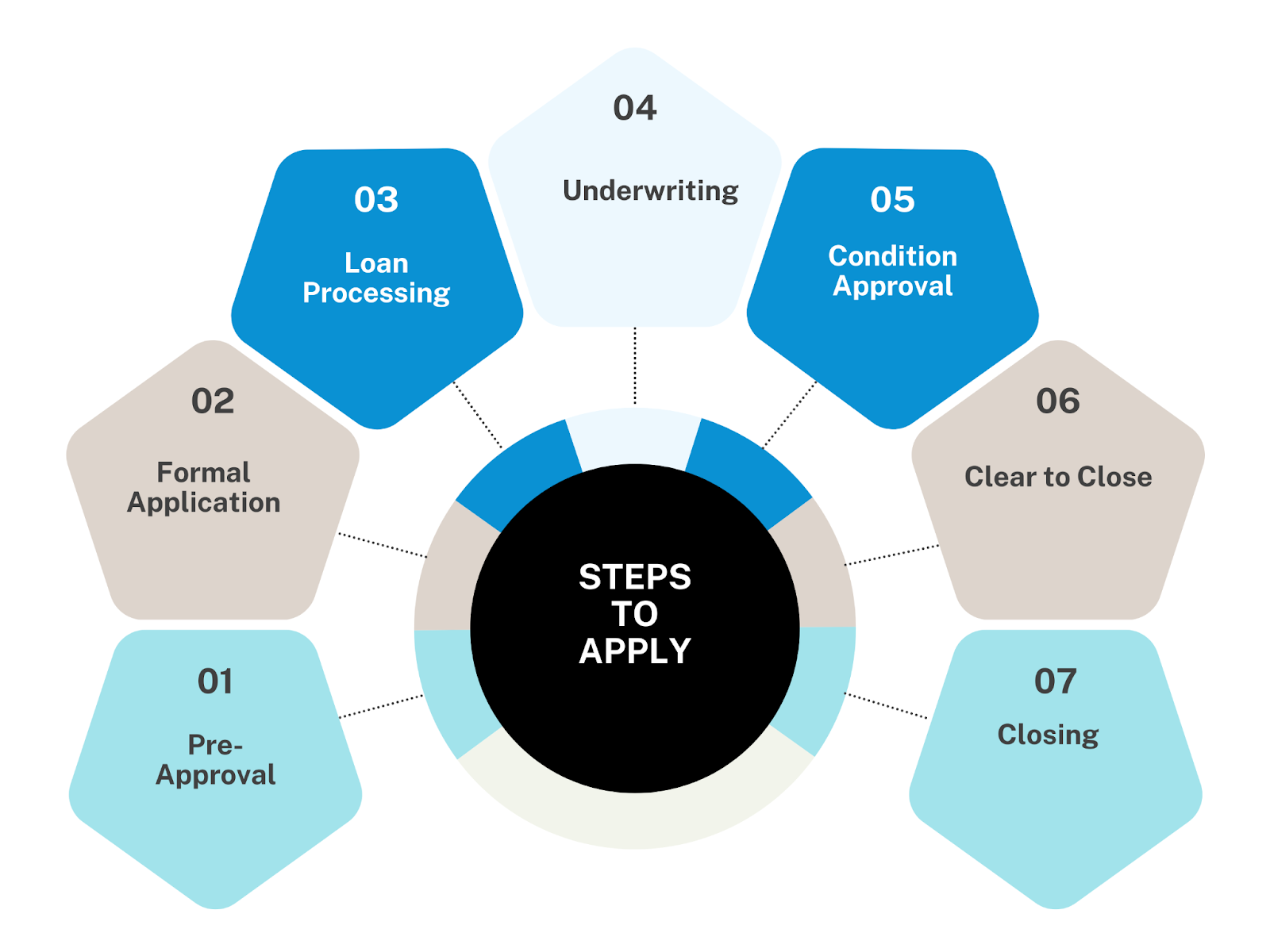

What is the Texas Mortgage Application Process?

Step-by-Step Application Guide for Texas Borrowers

- Pre-Qualification/Pre-Approval: Start your home buying journey on solid footing by getting pre-approved. This initial step helps determine your price range and demonstrates to sellers that you're serious. We review your financial situation and credit history to provide a pre-approval letter typically valid for 60-90 days.

- Formal Application: Once you've found your perfect Texas property and have an accepted offer, it's time to complete your full mortgage application. We'll guide you through completing the Uniform Residential Loan Application, collect your documentation, and discuss your loan options.

- Loan Processing: Our processing team verifies all your information and prepares your file for underwriting. This includes ordering the appraisal, title search, and verifying employment, income, and assets. For Texas properties, we'll also coordinate property tax verifications and HOA documentation if applicable.

- Underwriting: Our underwriters thoroughly review your application against the specific requirements of your chosen loan program. They may request additional documentation or clarification on certain items. Texas-specific underwriting considerations include reviewing property tax obligations and flood zone determinations for coastal and low-lying areas.

- Conditional Approval: Most loans receive a "conditional approval" that requires addressing specific items before final approval. Our team works proactively to clear these conditions quickly, often including things like explanation letters, additional asset documentation, or property-related information.

- Clear to Close: Once all conditions are satisfied, your loan receives the "clear to close" status. We'll coordinate with the title company to schedule your closing appointment and prepare your final closing disclosure, which must be delivered at least three business days before closing per federal regulations.

- Closing: At the closing appointment, you'll sign your loan documents, pay your closing costs, and receive the keys to your new Texas home. Texas is typically a "table funding" state, meaning funds are often available the same day as closing.

What Documents Are Required for Texas Mortgages?

- Valid government-issued photo ID

- Social Security number

- For non-citizens: Green card or visa documentation

- Most recent 30 days of pay stubs

- W-2 forms from the past two years

- Federal tax returns with all schedules (past two years)

- For self-employed: Business tax returns, profit/loss statements, and business license

- Two months of bank statements (all pages, all accounts)

- Recent statements for retirement accounts, investments, or other assets

- Documentation for the source of your down payment

- Gift letters if using gift funds (common for first-time buyers)

- Signed purchase agreement

- Contact information for the title company

- Home insurance quote

- HOA information if applicable

- For new construction: Builder contract and specifications

- Texas Residential Property Disclosure (provided by seller)

- Texas homestead exemption documentation (if applicable)

- Flood zone certification (especially important in coastal and Houston areas)

- Wind/hail insurance information (required in many Texas regions)

- VA Loans: Certificate of Eligibility, DD-214

- FHA Loans: FHA Case Number

- Bank Statement Loans: 12-24 months of business/personal bank statements

- DSCR Loans: Property rental income documentation

Texas Closing Process and Timeline

- Application review and document collection

- Appraisal ordered (typically takes 7-10 days in Texas markets)

- Title work ordered

- Initial underwriting review begins

- Appraisal received and reviewed

- Underwriter issues conditional approval

- Additional documentation requests addressed

- Title work examined

- All conditions cleared with underwriting

- Final approval issued

- Closing Disclosure prepared and delivered (3 business days before closing)

- Final loan documents prepared

- Closings typically occur at title company offices, not attorney offices

- Texas is a community property state, often requiring both spouses to sign documents even if only one is on the loan

- Texas has unique home equity loan restrictions protecting homeowners

- The Texas Homestead Law provides special protections requiring specific closing documentation

Why Choose Truss Financial Group for Your Texas Mortgage?

Personalized Texas Lending Solutions

- Self-Employed Professionals - Our bank statement loan programs are perfectly suited for Texas entrepreneurs, freelancers, and business owners who may show limited income on tax returns but have strong, steady cash flow.

- Real Estate Investors - Our DSCR loans are designed for Texas property investors, using the property's rental income potential rather than your personal income to qualify.

- Military Members and Veterans - Beyond standard VA loans, we help Texas service members access state-specific veteran housing benefits that many lenders aren't familiar with.

- Medical Professionals - Our specialized physician loans help Texas doctors, dentists, and other healthcare professionals overcome student debt hurdles and qualify for homes that match their future earning potential.

- Foreign Nationals - For international buyers investing in Texas real estate, our foreign national programs offer solutions when traditional financing isn't available.

- Credit Challenges -

We look beyond credit scores to help Texas homebuyers with past credit issues, offering rehabilitation loans and portfolio products that consider your full financial picture.

What sets us apart is our consultative approach. Rather than simply taking applications, we start with understanding your goals, timeline, and financial situation. Then we custom-tailor a mortgage solution that aligns with your specific needs—whether you're buying your first home in Houston, investing in Dallas rental properties, or building your dream home in the Hill Country.

Our mortgage advisors are readily available by phone, email, text, or in-person at our Texas offices. We're committed to clear communication throughout the process, with direct access to decision-makers who can solve problems quickly.

Texas Mortgage FAQs

Is Now a Good Time to Buy a Home in Texas?

How Do Texas Mortgage Rates Compare Nationally?

Texas mortgage rates typically track within 0.125% of national averages. The competitive Texas lending market – with numerous banks, credit unions and mortgage companies – often creates slightly better rate options than you'll find in less competitive states.

Texas rates benefit from the state's stable property values, which lenders view as lower risk. Urban areas like Houston, Dallas, and Austin generally see the most competitive rates, while some rural areas may run slightly higher.

Your personal rate will depend far more on your credit score, down payment, and loan type than on Texas-specific factors.

What Makes Texas Home Loans Different?

Texas has distinctive mortgage features you won't find in most states:

- Strong homestead protections that limit home equity borrowing to 80% of your home's value

- Community property laws that typically require both spouses to sign mortgage documents

- State-regulated title insurance rates that are identical across all title companies

- No prepayment penalties allowed on most home loans

- Higher property taxes balanced by no state income tax (affecting debt-to-income calculations)

- Unique Texas Veterans Land Board loan programs with below-market rates

- Special closing procedures using title companies rather than attorneys

- 12-month waiting periods between cash-out refinances

These Texas-specific differences can impact everything from your closing costs to refinancing options.

Can I Buy a House in Texas with No Down Payment?

Yes – several legitimate zero-down options exist for Texas homebuyers:

-

VA loans for veterans and active military (no down payment, no monthly mortgage insurance)

-

USDA loans for properties in designated rural areas (many Texas suburbs qualify)

-

Texas Veterans Land Board loans for Texas veterans (often with minimal to no down payment)

-

Down payment assistance programs through programs like My First Texas Home (providing up to 5% of your loan amount)

-

City-specific assistance in Houston, Dallas, Austin, and San Antonio

While zero-down financing makes homeownership more accessible, remember that putting money down reduces your monthly payment and builds immediate equity.

Start Your Texas Homeownership Journey

Taking the first step toward your Texas home purchase is easier than you think. Our mortgage team can guide you through the entire process with expert, personalized service.

Get started today:

-

Call: 888-878-7715

-

Email: hello@trussfinancialgroup.com

-

Visit: www.trussfinancialgroup.com

Get the information you need to make confident decisions

Discover your borrowing power and plan your mortgage journey with knowledge on your side.

Get a quote- No documents required

- No commitment

- No commitment

Get a quote in 3 easy steps

Tell us what you want

Fill out our online form to help us understand your financial situation and loan needs.

We get to work for you

We review your info and look for competitive rates that match your specific goals.

You get a personalized quote

You’ll receive a customized rate quote that meets your unique profile.