4.6 from 700+ reviews

4.6 from 700+ reviews

4.6 from 700+ reviews

Key Features

Understanding Home Equity and HELOCs

Using the equity in your house is a wise financial decision, whether you're planning a remodel, paying for college, or paying off debt.

What is a Home Equity Line of Credit?

A HELOC, or home equity line of credit, is a loan that uses your home as collateral, similar to a primary mortgage. Equity is the difference between how much your home is worth on the market and how much you still owe on it. A HELOC is similar to a credit card in that it enables you to borrow a certain amount of money over time. You pay interest only on what you draw down as needed, not on the entire line of credit. This makes it a good choice for things like fixing up your house, paying for college, or other costs that come up unexpectedly.

How does Home Equity Line of Credit work in California?

You build home equity as you pay down your mortgage and as the value of your home goes up. Prices of properties in California tend to increase over time, particularly in places with high demand. This means many homeowners may be able to accumulate equity rapidly, which can be used to obtain cash via a HELOC. Lenders will generally allow you to borrow 85% of the value of your home, subtracting what you owe on your mortgage. The more equity you have, the more money you can borrow.

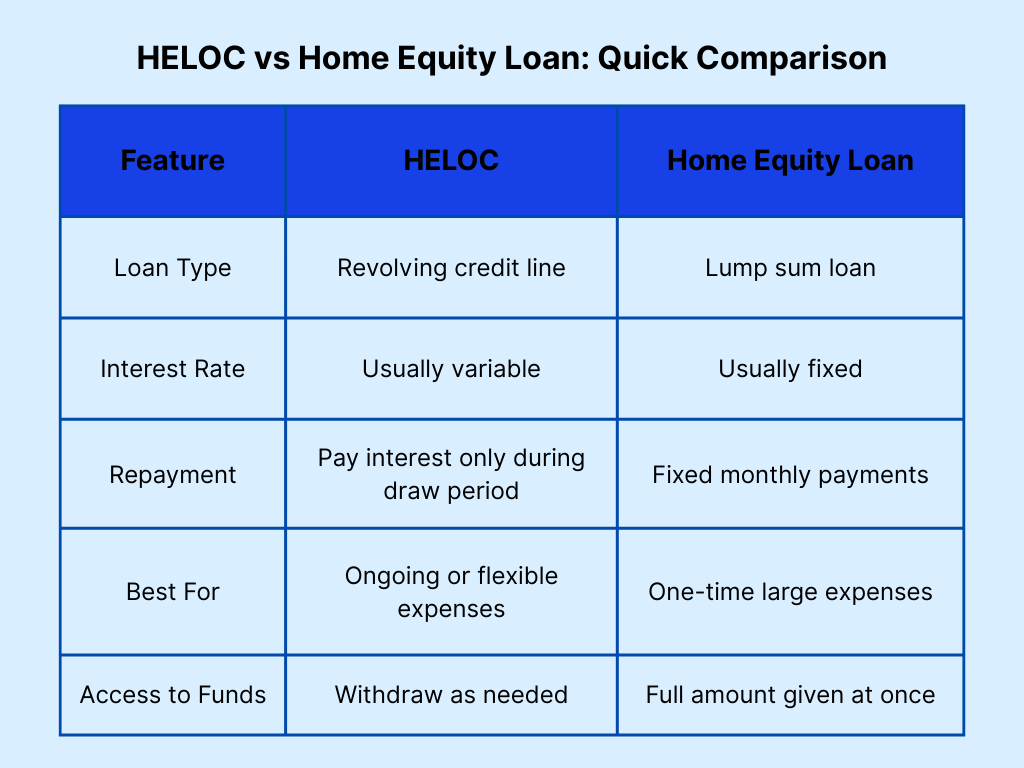

HELOC vs Home Equity Loan

A HELOC and a home equity loan both use your property as collateral, but they work in different ways. With a home equity loan, you get a single payment with a fixed interest rate and fixed payments. A HELOC, on the other hand, lets you borrow money when you need it and normally has an interest rate that changes. A HELOC is more flexible, but a home equity loan is preferable for big, one-time costs. How you want to spend the money and your financial goals will help you decide between the two.

HELOC vs Home Equity Loan: Quick Comparison

Home Equity Line of Credit Rates and Payments in California

Let’s explore HELOC rates and payments in California:

Home Equity Line of Credit rate in California

Bankrate says that the national average HELOC interest rate is 8.20% as of May 14, 2025. Depending on your credit score, home equity, and lender, rates in California usually fall between 8.25% and 9.75%. Many lenders have special rates for the first 6 to 12 months, and then the prices change based on the prime rate.

What is the HELOC rate in California?

California's HELOC rates are similar to the rest of the US, but they may be higher due to higher property values and demand. Homeowners with good credit may get rates like the national average of 8.14%, while others may get 9.5% or more. Always check rates from more than one lender and ask about rate limitations and margins.

Home Equity Loan Rates

The interest rates on home equity loans are fixed, so you can easily plan your budget. The national average rate is 8.36% as of mid-2025, while California borrowers may get offers between 7.25% and 9.00%, depending on their credit and the details of the loan. These loans are great for big, one-time costs like upgrading your home or paying off debt.

Home Equity Line of Credit Rates California

In California, lenders offer competitive home equity loan rates, especially in locations where property values have gone up a lot. Rates usually range from 7.25% to 9.00% as of 2025. This depends on your credit score, the size of the loan, and the length of the term. People who own homes in counties like Los Angeles, Orange, San Diego, and Santa Clara may be able to get lower rates because their properties are worth more and they have a lot of equity.

Many local banks, credit unions, and private lenders provide home equity loans with fixed rates that last from 5 to 30 years. To stay competitive, many of them also offer flexible repayment plans and may remove some fees, like closing costs or application fees. With a fixed-rate loan, you know how much your monthly payments will be, which makes it easier to plan for big needs like home repairs, medical bills, or college tuition.

What is the monthly payment on a $50,000 home equity line of credit?

If you had a $50,000 HELOC with an 8.14% interest rate, the monthly payment will be about $339.17. Depending on how long you have to pay it back, your monthly payments might be between $418 and $450 if you pay both the principal and the interest.

What is the monthly payment on a $100,000 home equity line of credit?

If you have a $100,000 HELOC with an 8.14% interest rate, the monthly payment would be roughly $678.33. Depending on how long and how the repayment plan is set up, full amortized monthly payments could be between $835 and $900.

HELOC Requirements and Tools

Home Equity Line of Credit requirements in California

In California, you usually need at least 15% to 20% equity in your home and a credit score of 620 or higher to get a HELOC. If your credit score is 700 or above, you may be able to get better prices. Loan experts at Truss Financial Group look at your whole financial picture, including your income, the value of your house, and your debt-to-income ratio. Truss also helps homeowners who may not fit the usual requirements for a loan, which makes it easier for more Californians to get to their home equity.

How Truss Helps You Estimate HELOC Options

Truss Financial Group give you individual support to help you figure out how much you can borrow and what your monthly payments would be. Their staff will help with every step of the way, looking at your home's worth, mortgage balance, and goals to create a HELOC plan that works for you. This one-on-one method gives you more accurate results than internet tools and helps you understand what to do before you apply.

Understanding Home Equity Line of Credit Estimates

Truss can help homeowners who want a lump-sum loan instead of a line of credit understand their alternatives for fixed-rate loans secured by home equity. They'll explain payments, loan payoff time, and possible interest rates. This approach is especially helpful if you are paying off debt or working on a single project like a renovation.

Finding the Best HELOC Options

Best home equity line of credit in California

Truss Financial Group is a reliable local authority when it comes to picking the best home equity line of credit (HELOC) in California. Truss doesn't just give you a one-size-fits-all HELOC as big banks do. Instead, they take the time to learn about your financial goals and make your HELOC meet them. They are a great alternative for California homeowners since they have competitive rates, quick processing, and personal attention.

Truss makes it easy to access your home equity by letting you choose how long to draw on it, paying interest, and being clear about the terms. Truss can help you with your home improvement project, college tuition, or debt consolidation by giving you advice and a loan arrangement. They'll help you look at your alternatives and decide if a HELOC is good for you without any pressure and with expert assistance.

You are welcome to speak with a Truss lending specialist right away to receive a personalized quotation or determine your eligibility. You don't have to fill out any online forms or guess.

Frequently Asked Questions (FAQ)

What is the difference between a HELOC and a home equity loan?

A HELOC is like a credit card in that it lets you borrow money as you need it. You only pay interest on what you use. A home equity loan provides you with an upfront lump sum amount and fixed monthly payments. HELOCs often have variable rates, while home equity loans have fixed fees and payments that are easy to plan for.

Can I qualify for a HELOC with bad credit in California?

If you have weak or fair credit, you can still receive a HELOC in California. However, your interest rate may be higher and your borrowing limit may be smaller. Truss Financial Group may help homeowners with any kind of credit issue. They may be able to help you qualify by looking at your home's equity and your whole financial picture, not just your credit score.

How do I calculate my monthly HELOC payments?

Your monthly HELOC payments will depend on your interest rate, balance, and whether you are in the draw period (when you only pay interest) or the repayment period (when you pay both principal and interest). To figure out how much you'll have to pay, multiply your current balance by the interest rate and then divide by 12. If you owe $50,000 at 8.14%, for instance, the payment that simply goes toward interest would be around $339 a month.

Is a fixed-rate HELOC better than a variable one in California?

When rates go up, a fixed-rate HELOC is useful since your payments stay the same. A variable-rate HELOC can start off lower, but your payments could go up later. Many homeowners in California are choosing fixed-rate alternatives for more stability now that rates are above 8% in 2025. Truss Financial Group will help you look at both types and figure out which one is best for your budget.

Get the information you need to make confident decisions

Discover your borrowing power and plan your mortgage journey with knowledge on your side.

Get a quote- No documents required

- No commitment

- No commitment

Get a quote in 3 easy steps

Tell us what you want

Fill out our online form to help us understand your financial situation and loan needs.

We get to work for you

We review your info and look for competitive rates that match your specific goals.

You get a personalized quote

You’ll receive a customized rate quote that meets your unique profile.