16 min read

16 min read

Do you know your DTI and, more importantly, do you know which Fannie Mae threshold it has to clear before a lender will approve your loan?

Most borrowers do not find out until after the denial. They know their credit score, their down payment, and their income. What they do not know is that Fannie Mae does not set one DTI limit. It sets three, and which one applies to their loan depends on details most borrowers are never told upfront. By the time the number matters, the loan application is already under review.

Lenders like Truss Financial Group put this resource together for borrowers who are done guessing. What follows is a clear breakdown of where Fannie Mae draws the line, what actually triggers a denial, and when a HELOC is the financing structure that brings the number back under the threshold.

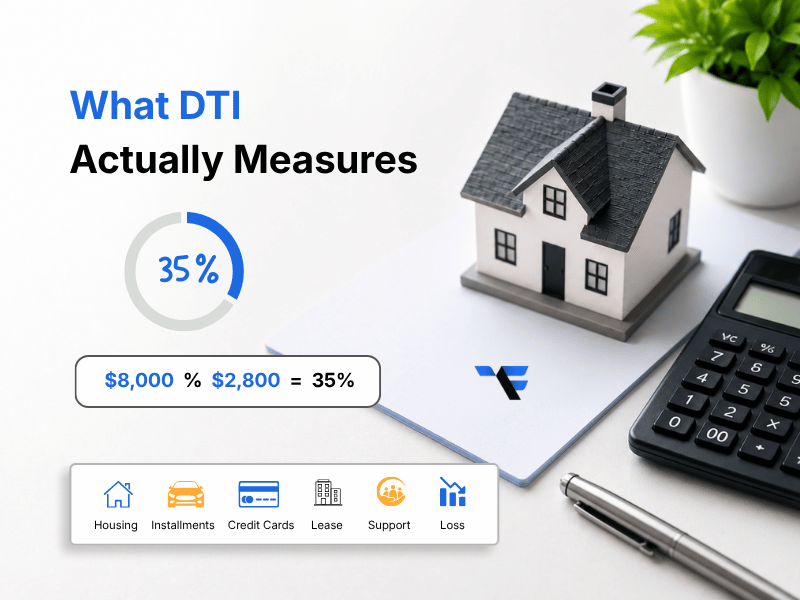

Your debt-to-income ratio compares your total monthly debt obligations to your gross monthly income, which is your income before taxes and deductions. The result, expressed as a percentage, tells a lender how much of what you earn is already committed to existing debt payments each month.

If your gross monthly income is $8,000 and your total monthly debt payments add up to $2,800, your DTI is 35%. That number sits under most conventional thresholds. Bring it to $3,600, and you are at 45%, a line where mortgage approval depends heavily on your loan type and how it is underwritten.

When lenders evaluate a loan application, the monthly obligation figure they work with is more specific than most borrowers realize. Under Fannie Mae's guidelines, your total monthly obligations include:

One detail that trips many borrowers up: installment debt with ten months or fewer remaining can still be counted if the lender determines it materially affects your ability to meet your outstanding debt obligations. That call belongs to the lender, not the borrower.

The reason lenders weigh the DTI ratio so heavily is that it answers a question a credit score alone cannot: of the income you bring in each month, how much is already spoken for?

Most borrowers assume there is one DTI limit for conventional loans. There is not. Fannie Mae sets different maximum DTI ratios depending on how the loan is underwritten, and the gap between those thresholds is where a significant share of fixable denials live.

|

Underwriting Path |

Standard Maximum DTI |

Maximum with Compensating Factors |

|

Manually Underwritten |

36% |

45% (with qualifying credit score and reserves) |

|

Desktop Underwriter (DU) |

50% |

50% |

For manually underwritten loans, Fannie Mae's standard ceiling is 36% of stable monthly income. That ceiling can extend to 45% if the borrower meets the credit score and reserve requirements outlined in Fannie Mae's Eligibility Matrix, but meeting those requirements is not automatic, and not every borrower qualifies.

Loans run through Fannie Mae's automated underwriting system, Desktop Underwriter, carry a higher ceiling of 50%. Two things worth knowing about that number:

Cash-out refinance transactions carry additional DTI considerations. Fannie Mae may apply a lower maximum DTI for cash-out loans run through DU than for standard purchase transactions, a detail that catches many borrowers off guard when they are trying to access equity while carrying existing debt obligations.

If new debt is discovered or disclosed during the mortgage process and causes a recalculated DTI to exceed 45% on a manually underwritten loan or 50% on a DU casefile, the loan is no longer eligible for delivery to Fannie Mae. The re-underwriting trigger is real, and it is why conventional lenders scrutinize the credit report and outstanding debt throughout the origination process, not just at the point of initial application.

A DTI denial does not mean a borrower is financially irresponsible. It usually means one of three things happened.

A denial is not a verdict. It is a signal that the conventional qualification framework may not be the right fit for the borrower's financial situation, and that the next step is identifying exactly which threshold applied and whether it can be addressed.

If a HELOC has no required monthly payment, it may not create a recurring monthly debt obligation for DTI purposes. Once the line is drawn and a required payment exists, that payment must be included in your monthly obligations going forward.

This is not a blanket rule. It depends on whether a payment is actually required, and borrowers should not assume an open home equity loan or line of credit is invisible to a lender without confirming the terms.

A HELOC lowers your debt-to-income ratio only when it is used to consolidate existing debt, and the required actual monthly payment on the HELOC is lower than the combined monthly debt payments it replaces.

If the HELOC payment is equal to or higher than what it eliminates, your DTI does not improve. The math has to produce a net reduction in monthly obligations for the strategy to work.

The consolidation case that makes the most sense looks like this: a borrower carrying several high-interest installment loans, credit card debt, or other revolving credit balances uses a HELOC draw to pay off those outstanding balances. The individual monthly payments disappear.

The HELOC's required payment takes its place. If that single payment is meaningfully lower than the sum of what it replaced, the total monthly obligation figure drops, and so does the DTI.

Before applying, model the post-consolidation DTI, not just the pre-draw picture. The question the lender will ask is what your monthly obligations look like after the HELOC is in place, and the answer to that question determines whether the strategy clears the applicable Fannie Mae threshold.

HELOC lenders set their own requirements for DTI, home equity, credit score, and lien position. Borrowers near any DTI ceiling should run their specific numbers before applying rather than assuming a particular threshold applies to their situation.

Both products let a borrower access home equity. How they interact with DTI is meaningfully different.

| Features |

HELOC |

Cash-Out Refinance |

|

DTI impact |

Only when a required payment exists |

Immediately and permanently |

|

Lien position |

Second lien, existing mortgage stays |

Replaces the existing mortgage entirely |

|

Fannie Mae DTI ceiling |

Set by HELOC lender |

May be lower than the standard purchase ceiling |

|

Closing costs |

Typically lower |

Rolled in or paid upfront, adds to the loan amount |

|

Timing control |

Borrower controls when the draw and payment begin |

DTI impact locked in at closing |

For a borrower already near the DTI ceiling, a cash-out refinance can push them over it. A HELOC used for targeted debt consolidation, structured correctly, may bring them under it. The right product is not the one with the better interest rate. It is the one that produces a lower post-transaction DTI given the borrower's current monthly debt obligations.

Run the DTI math on both before choosing. The rate comparison comes second.

For some borrowers, the consolidation math does not close the gap. The DTI problem is structural, either because the income documentation available does not reflect actual cash flow or because the outstanding debt load is too large to be resolved through a single consolidation product. This is where non-QM loan programs become relevant.

Investors with high rental income but high personal DTI ratios may find that DSCR loans fit their situation more cleanly. DSCR loans qualify based on the rental income generated by the subject property rather than the borrower's personal DTI, using a debt service coverage ratio to assess whether the property's income covers its obligations.

This is a different underwriting structure than Fannie Mae conventional loans, and it may help borrowers whose investment property income is real but whose personal debt-to-income ratio does not meet conventional guidelines.

Self-employed borrowers and those with variable income whose tax returns understate qualifying income have a path through bank statement loans, which use 12 to 24 months of bank statements to calculate income based on actual deposits rather than taxable income.

For borrowers whose actual cash flow and income stability are strong but whose paper DTI is inflated by low documented income, this structure addresses the problem at its source.

These non-QM loan programs use different underwriting frameworks than Fannie Mae conventional loans. They have their own qualification criteria and are not without standards. But for the right borrower, they remove the DTI barrier that conventional guidelines create rather than working around it.

This is the conversation mortgage brokers like Truss Financial Group have with borrowers who have exhausted the conventional path, identifying which underwriting structure fits the income they actually have, not the income a tax return reflects.

Fannie Mae sets different maximums depending on how the loan is underwritten. For manually underwritten loans, the standard ceiling is 36%, expandable to 45% if the borrower meets specific credit score and reserve requirements in the Eligibility Matrix. For loans run through Desktop Underwriter, the maximum allowable DTI is 50%. Which ceiling applies depends on the loan type and lender process, and not every borrower has access to the DU ceiling.

Because the 50% ceiling applies only to loans run through Desktop Underwriter. A manually underwritten loan has a ceiling of 36%, or 45% with compensating factors. A borrower at 42% DTI can be denied on a manually underwritten loan, while a borrower at 48% gets approved on a DU casefile. Loan type determines the ceiling, and most borrowers are not told which process was used.

Only under a specific condition: the required actual monthly payment on the HELOC must be lower than the combined monthly obligations it replaces. If the HELOC payment equals or exceeds what it eliminates, DTI does not improve. Model the post-consolidation number before applying.

If the HELOC has no required monthly payment, it may not create a recurring monthly debt obligation for DTI purposes. Once a required payment exists, after drawing on the line, that payment must be included in the monthly obligations. The terms of the specific home equity loan or line of credit determine this, not a general rule.

For investors, a DSCR loan may qualify based on rental income rather than personal DTI. For self-employed borrowers or those with variable income, a bank statement loan may use actual deposit history to calculate qualifying income rather than tax returns. Both use different underwriting structures than Fannie Mae conventional loans and may fit borrowers whose financial situation does not meet conventional guidelines.

It depends on which debts, how quickly the outstanding balance can be paid down, and how close the borrower is to the applicable threshold. Paying off a high-interest installment loan directly reduces monthly obligations without creating a new payment, but takes time. A HELOC consolidation can restructure multiple obligations into one lower required payment immediately, if the math supports it. The right approach depends on the borrower's specific debt structure and timeline.

Fannie Mae's DTI limits are not arbitrary, and they are not the same for every borrower. They shift with the underwriting path, the loan type, and the full financial situation, and the gap between those thresholds is where most fixable denials live.

A borrower who knows which ceiling applies, models their post-consolidation DTI honestly, and understands which loan program fits their income structure is in a different position than one waiting for conditions to improve on their own. The market does not fix a DTI problem. The right financing structure does.

Specialized lenders like Truss Financial Group work with buyers, homeowners, and investors to find that structure, whether it starts with a HELOC, a DSCR loan, or a bank statement product built for the way they actually earn. If DTI is holding your loan approval back, that conversation starts here.

Take your pick of loans

Experience a clear, stress-free loan process with personalized service and expert guidance.

Get a quote

19 min

-2.png?width=352&name=Blog%20covers%20(8)-2.png)

13 min

.png?width=352&name=xxxxxx%20header%20(23).png)

19 min

Discover your borrowing power and plan your mortgage journey with knowledge on your side.

Get a quoteGet a quote in 3 easy steps

Tell us what you want

Fill out our online form to help us understand your financial situation and loan needs.

We get to work for you

We review your info and look for competitive rates that match your specific goals.

You get a personalized quote

You’ll receive a customized rate quote that meets your unique profile.