10 min read

10 min read

.jpg)

A house is more than just a place to live; it's an investment that gets better over time. Your home's value goes up as you pay off your mortgage, and the home equity you build can be used to get funds. A home equity line of credit (HELOC) is a common way to reach that value.

You can borrow money against the equity in your home with a HELOC and use it for different purposes that include tuition fees, debt consolidation or any major expense that comes up. Before you think about getting a home equity line of credit, you should know what lenders want in terms of equity.

When assessing if you qualify for a HELOC, lenders consider a lot of different factors. Your credit history, how much home equity you have, how steady your income is, how much debt you already have, and how much your home is worth in the market right currently are all very important. Homeowners can get a good idea of whether they meet the basic HELOC qualifications and how much they might be able to borrow if they know these things.

Home equity is the difference between the value of one’s home and what mortgage debt one still has. When you take a loan to buy a house, you only own part of it at first. The lender keeps a major part until the loan is paid off. The home equity grows as you pay down the mortgage and the home becomes more valuable.

A HELOC lets people borrow money against the value of their homes. A home equity line of credit is not the same as a regular loan because it doesn't give you a set amount of funds all at once. Instead, it works like a revolving credit account. During the draw period of a HELOC, you can withdraw funds whenever you need, with cumulative amounts not exceeding the credit limit. During this time, borrowers can pay off their debt and then withdraw funds or just repay the interest, draw additional funds and repay together in the repayment period.

Another important part of a HELOC is how interest works. Most lenders offer a variable interest rate based on benchmarks like the WSJ prime rate. This means that the interest rates on HELOCs can go up or down depending on market fluctuations. This built-in variability is good for borrowers as they always have money on hand, but it means they need to plan their finances very carefully. A HELOC is a way for many homeowners to draw funds without having to sell their home or go through the whole process of refinancing their mortgage. This gives them some freedom with their money.

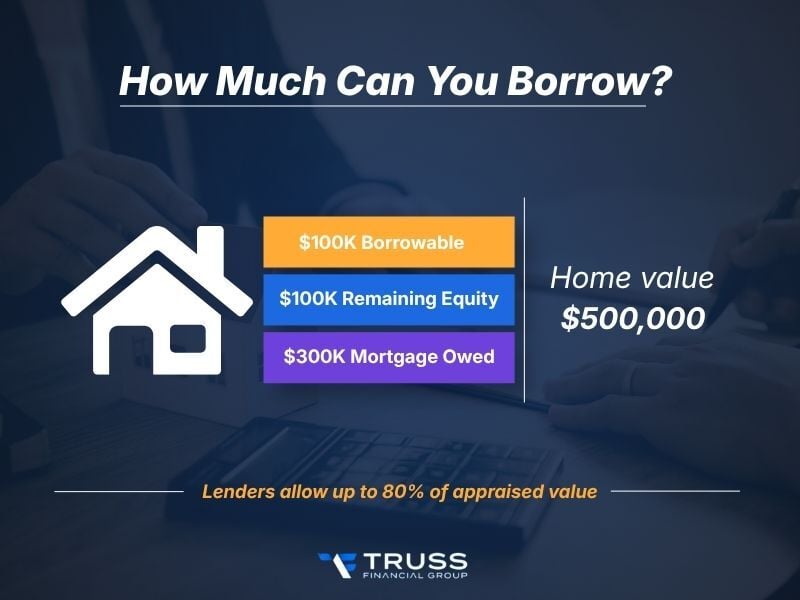

You need to have enough equity to get a HELOC. Most lenders want you to keep at least 15% to 20% of the value of your home after you take out a HELOC loan. Most lenders let homeowners borrow about 80% to 85% of the appraised value of their home. This extra funds keeps the lender from losing money if the value of the property goes down or the borrower doesn't pay back the loan.

If a house’ current market value is $500,000 and the owner owes $300,000 on their existing mortgage, they have $200,000 in equity. If the lender lets you borrow up to 80% of the value of the property, you can only borrow $400,000. A HELOC can give a homeowner up to $100,000 if they don't have a current mortgage balance right now.

If you have good credit, a steady income, and not much debt, some lenders will give a combined loan-to-value of up to 90%. But the lender's own rules and the borrower's overall financial situation have a big effect on these approvals. Some states, for example, allow cash-out loans up to 80% of the home's appraised value.

When a lender decides whether or not to give a home equity line, they evaluate two important financial indicators: the loan-to-value ratio and the combined loan-to-value ratio.

The loan-to-value ratio is a simple way to show how much of the home's value the mortgage balance is covering. To get the loan-to-value ratio, divide the amount of the mortgage by the value of the property as a whole. If the house is worth $500,000 and the mortgage is $300,000, the loan-to-value ratio is 60%. But when lenders look at a HELOC, they look at the combined loan-to-value ratio. This includes both the new equity line and the current mortgage. The CLTV tells lenders how much debt the property has in total.

The combined loan-to-value ratio should be 80% or lower for most lenders. As long as homeowners stay below this limit, they can keep some of their equity even if they use a HELOC. These ratios can help homeowners figure out how much they can borrow with a HELOC before they start the application process.

Lenders determine the current appraised value of the property before they give a HELOC. This valuation is important because it tells how much equity you have, which in turn tells how much money they are willing to lend you. Usually, lenders hire a licensed appraiser to do a professional appraisal to determine the current market value. Some lenders use automated valuation models to figure out how much a house is worth. These tech-based estimates use information about the property and recent sales to come up with a value. The final value is important for figuring out borrowing power available through a HELOC.

When deciding whether or not to approve a HELOC, lenders look at more than just equity. One of the most important things is the borrower's credit history. A strong credit history shows that you are good with finances, which makes lending less risky. People with good credit scores often get better annual percentage rates and terms for better repayment terms.

The debt-to-income ratio shows how much a borrower's total monthly debt payments are compared to their gross monthly income. This is how lenders find out if a borrower can afford to make new HELOC payments on top of what they already owe.

Most lenders want to see proof of a steady income to make sure the borrower can make payments during both the draw period and the repayment period. Lenders assess the borrower's other debts, such as personal loans and existing loans, as well as their overall credit history. Borrowers with several mortgage debts and unstable income can find it harder to get approvals for equity line of credit. Many HELOCs have variable interest rates. When rates go up, so do the monthly payments, so lenders carefully look at a borrower's finances.

Homeowners who don't quite have enough equity for a HELOC can still do things to make it more likely that they will qualify in the future. One easy way to build equity is to pay off the mortgage balance. Every payment lowers the principal, which means you have more equity in your home.

You can build equity by making smart changes to your home. When the current market value goes up, so does your equity.

The growth of the real estate market can help homeowners. Property values usually go up over time. This can happen when the economy and the infrastructure is improving, or there is an increase in the demand for housing. Paying off your debts can help you get a HELOC. If you have lesser debt, your debt-to-income ratio goes down. If a borrower has a good credit history, they are more likely to get a home equity line of credit.

Even if you have some equity built up, there are times when you might not be able to get a HELOC. A lot of people have trouble because they don't have enough equity. If the lender's rules say your combined loan-to-value ratio is too high, they might not approve your application.

A bad credit history can be a hurdle. Most lenders don't lend funds to applicants with missed payments, or have used up most of the credit, or have a low credit score. A high debt-to-income ratio could be an issue. If a borrower's monthly debt payments take up a big part of their income, lenders may see more borrowing as a risk. Having an unstable income or not always having a job can make it harder to get approved. Lenders want to be sure that borrowers will always have enough money to make their monthly payments for the entire loan term.

If a chosen property has a few debts already, each with a different place in the lien positions, lenders may not want to give more credit that is backed by that same asset. By knowing about these possible problems, borrowers can improve their finances before applying for a home equity line of credit.

A HELOC is a great way to access funds quickly if you own a home equity. Lenders usually require borrowers to have at least 15–20% equity in their property and will look at the loan-to-value ratio. Lenders check for credit score, how stable your income is, and how much debt you have compared to your income.

The HELOC program from Truss Financial Group helps homeowners figure out what they need, guide on the pros and cons of different financing options. HELOC helps borrowers who need funds by understanding their finances so they can make smart decisions about HELOCs and other home equity options.

Take your pick of loans

Experience a clear, stress-free loan process with personalized service and expert guidance.

Get a quote%20(1).png?width=352&name=Blog%20covers%20(2)%20(1).png)

17 min

-1.png?width=352&name=Blog%20covers%20(7)-1.png)

10 min

19 min

Discover your borrowing power and plan your mortgage journey with knowledge on your side.

Get a quoteGet a quote in 3 easy steps

Tell us what you want

Fill out our online form to help us understand your financial situation and loan needs.

We get to work for you

We review your info and look for competitive rates that match your specific goals.

You get a personalized quote

You’ll receive a customized rate quote that meets your unique profile.