19 min read

19 min read

You built equity in your home over decades. A reverse mortgage loan lets you convert that into usable cash without selling or taking on monthly payments. The loan is repaid when you sell, move out, or pass away. The product is well-established. Choosing the right lender is less straightforward. Reverse mortgage companies differ significantly in product range, fees, and service quality.

Mortgage brokers like Truss Financial Group work with borrowers across this process daily, and the difference between a good outcome and a costly one almost always comes down to who you work with, not just which product you choose. This article covers how reverse mortgages work, what they cost, and which lenders are worth your time.

A reverse mortgage loan allows older homeowners to borrow against the equity in their principal residence without making monthly payments. Instead of paying the lender each month, interest accrues on the loan balance over time. The loan becomes due when the borrower sells the home, moves out permanently, or passes away.

Reverse mortgages are non-recourse loans, meaning borrowers and their heirs cannot owe more than the appraised value of the home at the time of repayment, even if the loan balance has grown beyond that amount. This protection is backed by the federal government through the FHA insurance program on HECM loans.

The most common type is the HECM reverse mortgage, insured by the Federal Housing Administration and overseen by the Department of Housing and Urban Development. Proprietary and jumbo reverse mortgage options exist for borrowers who fall outside the HECM parameters.

|

Requirement |

Detail |

|

Age |

62+ for HECM; 55+ for some proprietary products |

|

Property type |

Principal residence only |

|

Equity requirement |

Must own outright or carry a small remaining mortgage balance |

|

Property standards |

Must meet FHA or lender condition requirements |

|

Counseling |

Mandatory HUD-approved session before HECM application |

Choosing the right reverse mortgage type comes before choosing a lender. The product determines your eligibility, cost structure, and how much money you can access.

|

Type |

Best For |

Key Feature |

|

HECM |

Most borrowers 62+ |

FHA-insured, flexible payout, usable for any purpose |

|

HECM for Purchase |

Borrowers buying a new primary home |

Finances new purchase using equity from the prior home, no monthly payments |

|

Proprietary Reverse Mortgage |

Borrowers 55+, higher-value homes |

Not government-insured, higher loan limits, and more flexibility |

|

Jumbo Reverse Mortgage |

Homes exceeding HECM loan limits |

Larger borrowing potential, issued by private lenders |

|

Single-Purpose Reverse Mortgage |

Lower-income borrowers with a specific need |

Lowest cost option, restricted use, such as property taxes or home repairs |

Most borrowers will land on a HECM or a proprietary reverse mortgage. The HECM reverse mortgage is the right fit for the majority. It is a reverse mortgage insured by the FHA through an approved lender, broadly available, and flexible on how you receive funds. A proprietary reverse mortgage makes sense if your home value is high, you are under 62, or you need a larger loan than the HECM program allows.

Single-purpose reverse mortgages are worth noting for lower-income homeowners. They are the least expensive option, but the use of the funds is restricted by the lender or issuing agency.

The right reverse mortgage company depends on your home value, your age, your state, and what you need the funds for. There is no universal answer, but there are five criteria that consistently separate the best reverse mortgage lenders from the rest.

|

Criteria |

What to Look For |

|

Product range |

Offers HECM, proprietary, and jumbo options, not a single-product shop |

|

Fee transparency |

Clearly discloses origination fees, mortgage insurance premiums, closing costs, and TALC upfront |

|

Customer satisfaction |

Strong independent ratings and low complaint volume |

|

State availability |

Licensed in your state; some products carry geographic restrictions |

|

Counseling support |

Guides borrowers through the HUD-approved housing counselor requirement, not around it |

One more factor worth considering is loan volume. A lender with consistent, high origination numbers has operational depth and product experience that a newer or smaller shop may not. That matters when questions come up mid-process. When you first speak with a loan officer, ask directly about their reverse mortgage products and how many they have closed in the past 12 months.

Truss Financial Group works with borrowers evaluating HECM, proprietary, and jumbo reverse mortgage options across a range of home values and financial situations. The focus is on matching borrowers to the right product, not the fastest close, with full fee transparency from the first conversation.

Features

Best for homeowners 62+ (or 55+ for proprietary products) who want a lender that takes the time to explain every option before making a recommendation.

CrossCountry Mortgage is among the highest-volume reverse mortgage lenders in the country by origination, which reflects broad operational experience across HECM and proprietary reverse mortgage products. A loan officer can walk borrowers through standard HECM options as well as proprietary programs for borrowers starting at age 55.

Features

Best for borrowers who want to work with a high-volume, nationally recognized lender with a full range of reverse mortgage products.

Finance of America is well-known for its proprietary reverse mortgage programs, which lower the eligible borrowing age to 55 and allow loan amounts up to $4 million for qualifying properties. Their second-lien proprietary product does not require the existing mortgage to be paid off first, which opens the door for borrowers who still carry a meaningful mortgage balance.

Features

Best for borrowers with high-value homes or those aged 55 to 61 who do not yet qualify for a HECM.

Longbridge Financial offers a proprietary product line with larger lump sums, flexible payout structures, and eligibility starting at age 55. They provide a $500 closing cost credit for active military members and veterans, along with mobile app access for account management.

Features

Best for veteran borrowers and those seeking a jumbo reverse mortgage with flexible disbursement options.

Reverse mortgage costs go well beyond the interest rate. The lender with the lowest rate is not always the least expensive option over the life of the loan.

|

Fee Type |

Typical Range |

Notes |

|

Origination Fee |

Up to $6,000 (HECM) |

HUD caps at 2% of first $200K + 1% of remainder; max $6,000 |

|

Upfront MIP |

2% of appraised value |

Required at closing for all HECM loans; paid to FHA |

|

Annual MIP |

0.5% of the outstanding balance |

Added monthly and compounds over time |

|

Closing Costs |

Varies |

Includes appraisal, title insurance, and inspections |

|

Servicing Fees |

Up to $35/month |

Not all lenders charge this; confirm upfront |

|

Interest Rate |

Fixed or variable |

Variable rate offers more payout flexibility; fixed rate typically requires a lump sum |

|

TALC |

Ask every lender |

Total Annual Loan Cost is the most accurate metric for comparing true loan cost |

Most of these costs can be rolled into the loan balance rather than paid out of pocket, but doing so increases the outstanding balance and accelerates equity depletion over time. Always ask every lender for their TALC disclosure. It is the only apples-to-apples comparison metric across different fee structures and rate types.

A reverse mortgage is not the only way to access home equity in retirement. Before committing to a lender, it helps to understand where it wins and where it does not.

|

Feature |

Reverse Mortgage |

HELOC |

Home Equity Loan |

Downsizing |

|

Monthly payments |

None |

Required |

Required |

N/A |

|

Age requirement |

62+ (55+ proprietary) |

None |

None |

None |

|

Repayment timing |

At sale, move-out, or death |

During the draw/repayment period |

Fixed term |

Immediate at sale |

|

Long-term cost |

Higher (MIP + compounding interest) |

Lower if paid regularly |

Fixed and predictable |

No debt incurred |

|

Best for |

Staying at home, no payment pressure |

Short-term access with income |

Lump sum needed with repayment capacity |

Full equity release |

A home equity loan delivers a fixed lump sum with predictable monthly payments, which works well for a borrower with stable retirement income who needs a defined amount. A HELOC offers a revolving line of credit but requires monthly payments and a qualifying credit profile. For borrowers on a fixed income with no appetite for monthly obligations, the reverse mortgage from a mortgage broker like Truss Financial Group wins on cash flow, but costs significantly more over a long hold period.

Downsizing releases full equity and eliminates all mortgage debt, but involves relocation costs and lifestyle adjustment. The reverse mortgage preserves the home while accessing a portion of that equity. The trade-off is real and worth thinking through honestly before deciding.

A reverse mortgage is a powerful tool for the right borrower. It also carries risks that deserve a direct conversation.

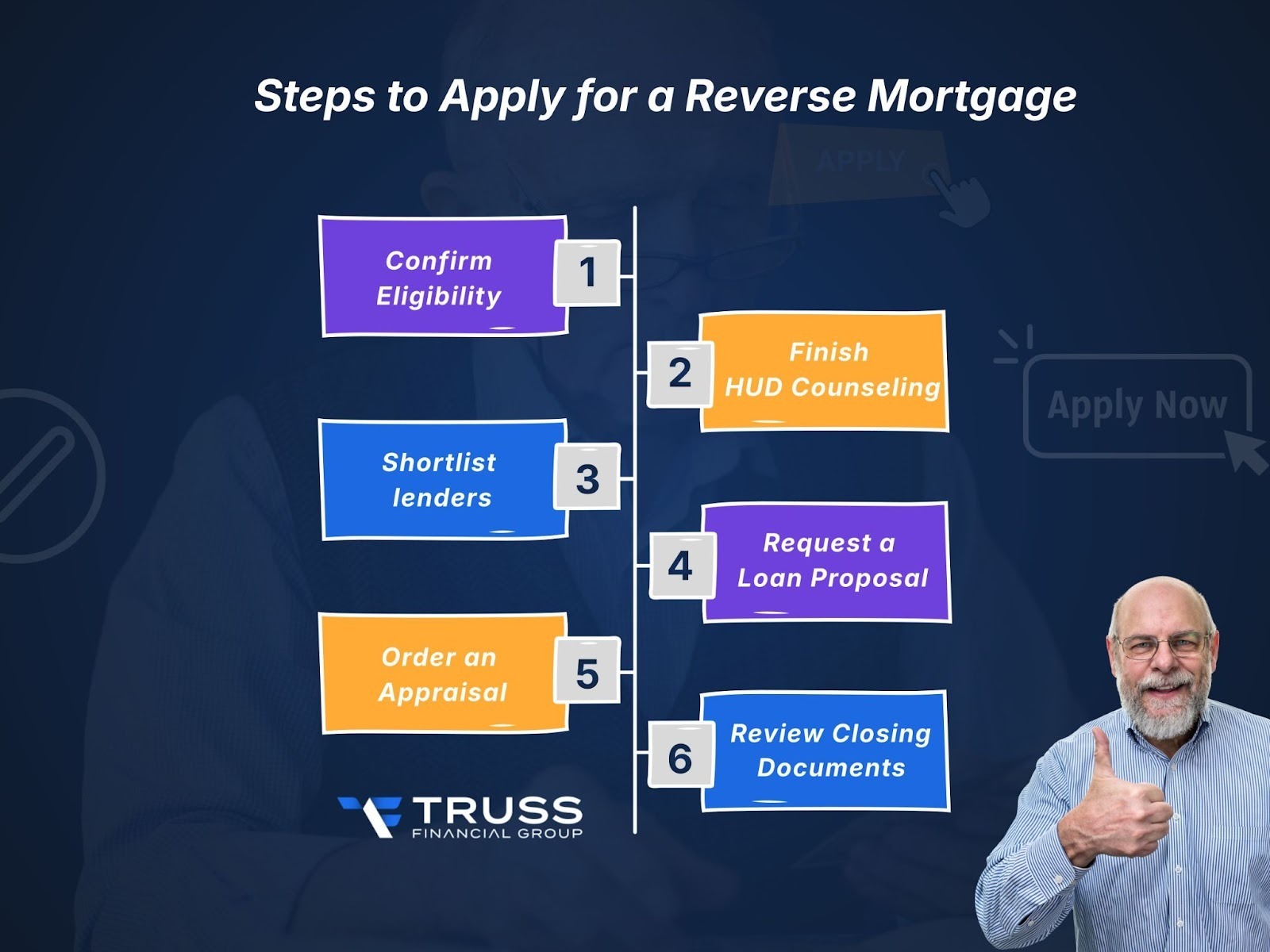

HECM applicants are required by federal law to complete a reverse mortgage counseling session with a HUD-approved housing counselor before submitting an application. This is not optional, and it is genuinely useful. The counselor has no stake in the transaction and is there to make sure you understand the full cost, your loan obligations, the impact on your estate, and any alternatives worth considering.

The counseling fee is typically around $125, can be paid from loan proceeds, and cannot be denied based on inability to pay. Borrowers who have outstanding federal debt, such as unpaid taxes or defaulted student loans, should raise this with their counselor early, as it can affect HECM eligibility.

Product range, fee transparency, customer service quality, and state availability are the factors that actually matter. A lender that offers only one product or buries fees until late in the process is not the right partner for a decision of this size. Ask any loan officer upfront for a full breakdown of reverse mortgage products and their associated TALC figures.

A HECM reverse mortgage is insured by the FHA through an approved lender, available to borrowers 62+, and capped at HUD loan limits. A proprietary reverse mortgage is issued by private lenders, often available to borrowers as young as 55, and can accommodate higher home values and larger loan amounts. Proprietary products are not backed by the federal government and may carry higher interest rates.

The main costs are the origination fee (capped at $6,000 for HECMs), upfront mortgage insurance premium (2% of appraised value), annual MIP (0.5% of the outstanding balance), closing costs, and, in some cases, a monthly servicing fee. Always ask for the TALC. It reflects the true total cost across all fee types.

Yes, in most cases. The existing mortgage balance must typically be paid off at closing, often using money from the reverse mortgage proceeds itself. Some proprietary products allow a reverse mortgage to be structured as a second lien, which does not require the first mortgage to be paid off.

If the youngest borrower moves out of the principal residence for more than 12 consecutive months, the loan generally becomes due. Planning for this scenario before closing is important, particularly for borrowers without a spouse or co-borrower remaining in the home.

When the loan matures, your heirs must repay the outstanding loan balance, typically by selling the home or surrendering the property to the lender. Because reverse mortgages are non-recourse, heirs cannot owe more than the home's sales price at the time of repayment.

TALC is the projected annual average cost of a reverse mortgage, incorporating all fees, interest, and insurance costs into a single comparable figure. It is the most reliable way to compare two reverse mortgage offers that have different rate structures or fee profiles.

A reverse mortgage is the right tool for a specific borrower. One with significant equity, a plan to stay in their home, and a need for cash flow flexibility without monthly payment obligations. The product is sound. What determines the outcome is who structures it.

The best reverse mortgage companies are transparent on fees, offer a full product menu, and guide borrowers honestly through the counseling process. They do not rush the decision. They ask the right questions before recommending a product.

That is the approach specialized lenders like Truss Financial Group bring to every reverse mortgage conversation. Matching borrowers to the right structure based on their home value, their age, their cash flow needs, and their estate goals, and getting it right before anything goes to closing. If you are ready to explore your options, the first step is a conversation.

Take your pick of loans

Experience a clear, stress-free loan process with personalized service and expert guidance.

Get a quote

8 min

15 min

6 min

Discover your borrowing power and plan your mortgage journey with knowledge on your side.

Get a quoteGet a quote in 3 easy steps

Tell us what you want

Fill out our online form to help us understand your financial situation and loan needs.

We get to work for you

We review your info and look for competitive rates that match your specific goals.

You get a personalized quote

You’ll receive a customized rate quote that meets your unique profile.