16 min read

16 min read

-1.png)

You earn well. Your bank account reflects it. But when you sit down with a conventional mortgage lender and hand over your tax returns, the number on the page can tell a very different story, shaped by legitimate deductions rather than what you actually bring home.

For self-employed individuals, small business owners, real estate investors, and freelancers, this is one of the most frustrating moments in the mortgage process. The decline does not always come from bad credit or an inability to repay. Often, it comes from a documentation gap: a mismatch between how you earn and how conventional lenders are required to verify income.

Stated income loans were created around that problem. They still exist today, but the product looks very different from what borrowers may remember before 2008.

Yes, but not in the old no-verification sense. Today's stated income loans are usually Non-QM mortgage programs that verify income through bank statements, rental income, or assets instead of W-2s and tax returns.

Mortgage brokers like Truss Financial Group help borrowers navigate this gap. This guide breaks down what stated income loans actually mean in today's market, who may qualify, what lenders look for, and which alternative income verification programs may be the most practical path forward for borrowers who do not fit the conventional mold.

-1.png?width=1200&height=628&name=Blog%20covers%20(4)-1.png)

A stated income loan is a mortgage that allows a borrower to qualify without relying on the traditional income documents used for conventional loans, such as W-2s, pay stubs, and full tax returns. Instead, lenders use alternative methods to evaluate the borrower's ability to repay.

In their original form, stated income mortgage loans required very little documentation. A borrower could state income on the application, and the lender might accept that figure with limited verification. That is where the older idea of a no-doc loan came from.

That old version of the product is not how responsible stated income lending works today. Modern stated income loans are usually Non-QM loans, which means they fall outside the standard Qualified Mortgage box but still require lenders to verify the borrower's ability to repay through alternative documentation. The name stayed, but the mechanics changed.

Before 2008, some lenders accepted stated income with little to no verification. That loose approach allowed borrowers to qualify for mortgages they could not realistically afford. When defaults rose, regulators tightened the rules around mortgage underwriting.

The official ability-to-repay rule appears in Regulation Z, 12 CFR 1026.43. For borrowers, the practical takeaway is simple: today's stated income loan is not a documentation-free shortcut. It is a different way to document income when traditional paperwork does not reflect the full picture.

The modern stated income loan can still look like a standard mortgage in many ways: fixed or adjustable rate, title review, appraisal, underwriting, and closing. The main difference is how income is documented.

Instead of W-2s and tax returns, lenders may analyze 12 to 24 months of personal or business bank statements to calculate average monthly income from actual deposits. Truss has a separate guide on how many months of bank statements may be needed for a mortgage.

For real estate investors, projected rental income on the subject property may be used in some DSCR programs. For asset-rich borrowers with limited current income, asset depletion calculations may convert verified assets into a qualifying monthly income figure.

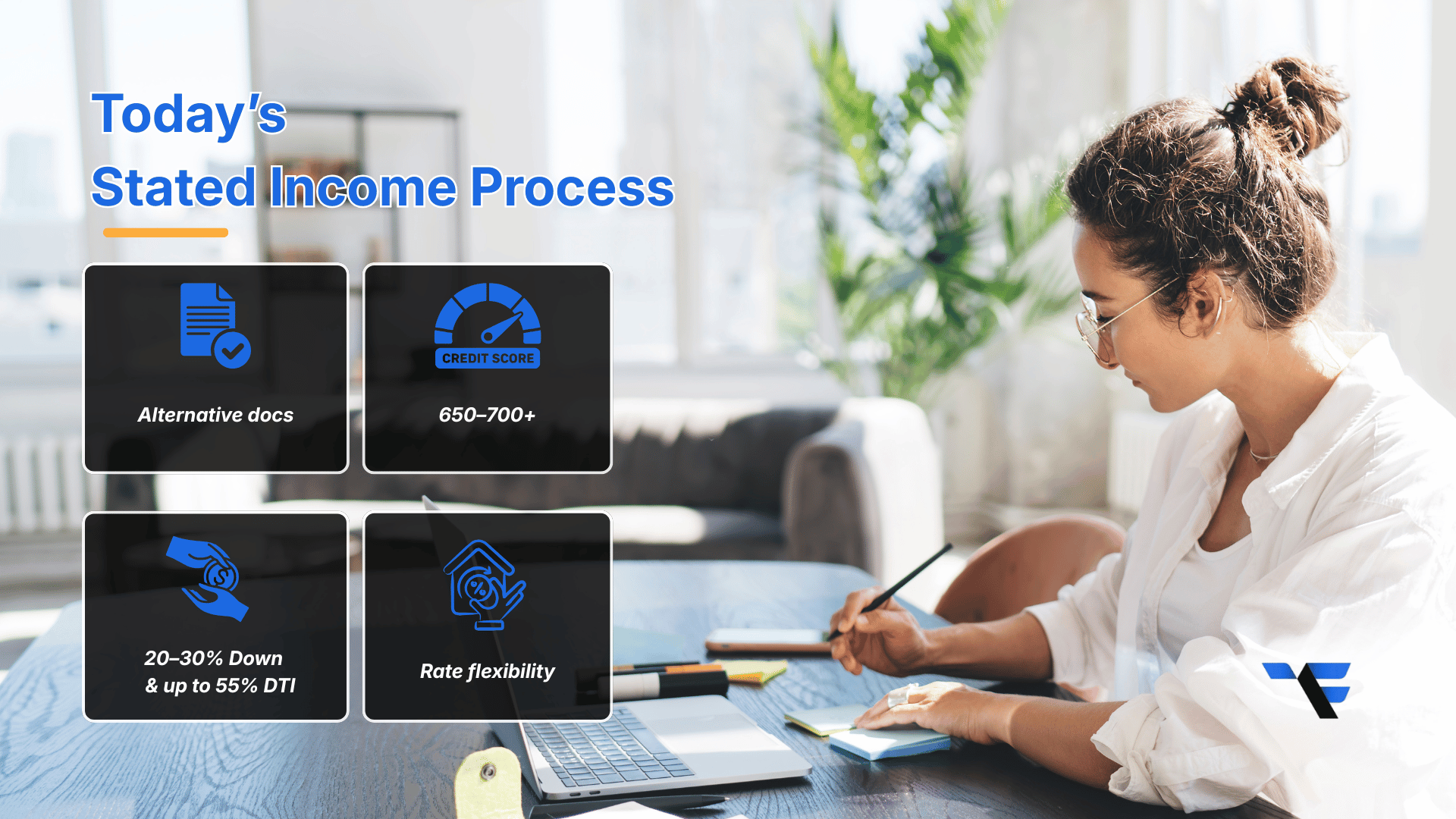

Because the lender is allowing documentation flexibility, the credit score becomes an important signal of repayment reliability. Many stated income and Non-QM programs prefer stronger credit, and a higher score can affect both approval odds and pricing.

Down payment requirements are usually higher than conventional loans because the lender is taking on added underwriting complexity. Debt-to-income ratio may still matter, though some Non-QM lenders review DTI against bank statement income rather than tax-return income.

Stated income mortgage rates are typically higher than conventional rates. That difference is the lender's risk premium for underwriting without traditional income documentation. The process is documentation-flexible, not documentation-free.

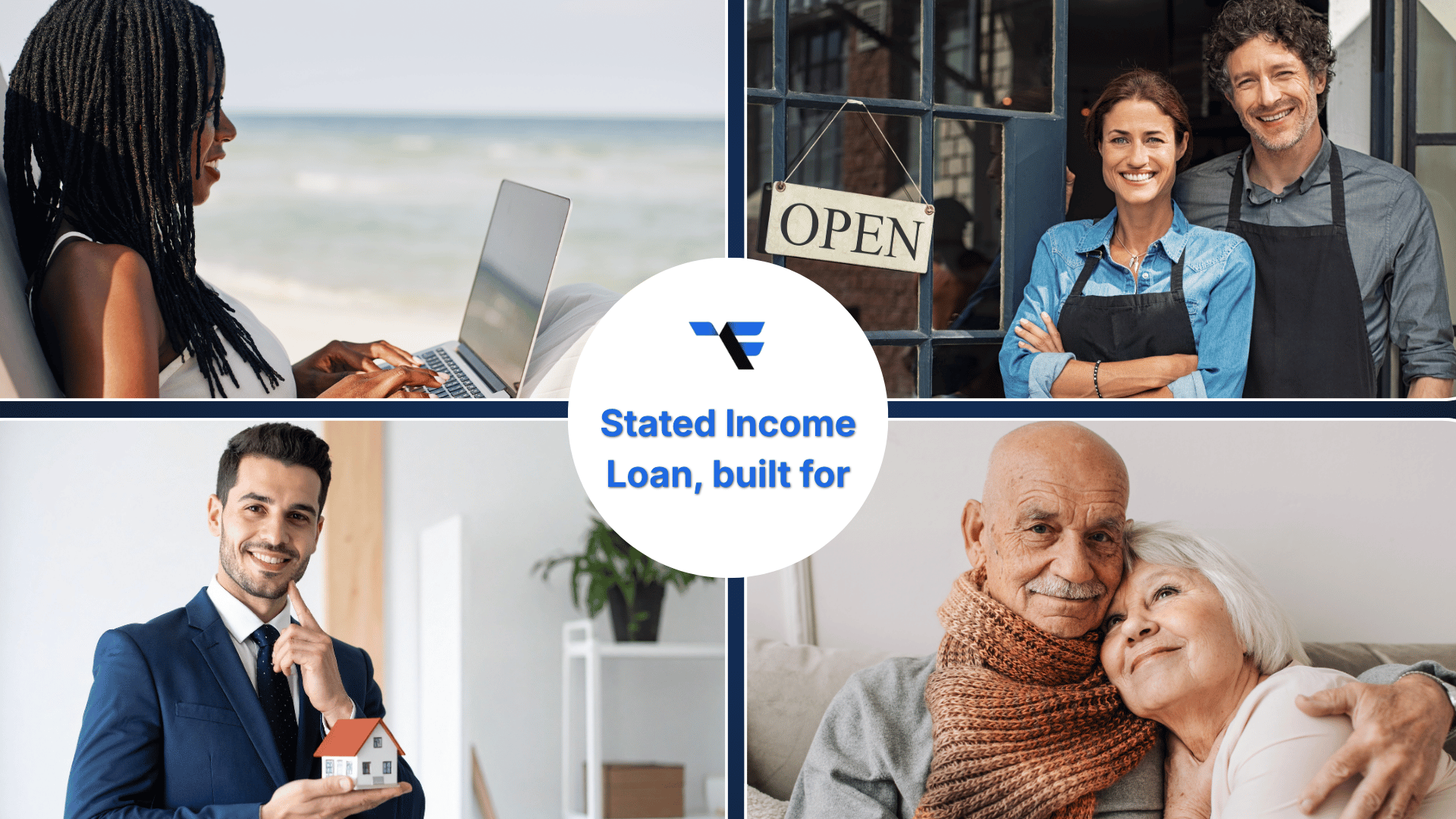

The borrowers who benefit most from stated income and alternative income verification loan programs share one thing in common: their tax returns may not show their actual cash flow or ability to repay.

A freelancer or consultant may earn strong gross income while also taking legitimate business deductions. Conventional lenders often qualify self-employed borrowers from taxable income, which can make the borrower look weaker on paper than they are in reality.

Business expenses, depreciation, and pass-through deductions can reduce taxable income while the business's cash flow remains strong. A bank statement loan may provide a cleaner way to evaluate that income.

Real estate investors often report rental income through IRS Schedule E, which can be difficult for some conventional underwriting models to interpret cleanly. DSCR programs may focus more directly on the property's rental cash flow.

Retirees and high-net-worth borrowers may have significant investment accounts but limited W-2 income. Their financial strength may live in their balance sheet, not in a monthly paycheck.

Seasonal workers, contractors, and commission-based professionals may have strong annual income but uneven monthly deposits. Alternative documentation can help underwriters look at the full income pattern.

Qualifying for a stated income loan is not easier than qualifying for a conventional mortgage. The standards are different, not lower. Borrowers who understand that distinction are usually better prepared for underwriting.

| Requirement | What it signals | Typical review point |

|---|---|---|

| Credit score | Repayment reliability carries extra weight due to documentation flexibility. | Often 650-700+, depending on program. |

| Bank statements | Actual cash flow, deposit consistency, and income pattern. | Commonly 12-24 months. |

| Down payment | Borrower equity and lender risk mitigation. | Often higher than conventional loans. |

| Cash reserves | Ability to cover payments after closing. | Varies by lender and loan size. |

| Proof of self-employment | Legitimacy and continuity of the income source. | Business license, CPA letter, or business history documentation. |

| Debt-to-income ratio | Capacity to carry the new mortgage payment. | Reviewed by program; Non-QM rules vary. |

When lenders review bank statements, they are not simply confirming deposits exist. They are looking at average monthly deposits, deposit consistency, average daily balance, and whether the pattern supports the income figure used for qualification. Separating personal and business accounts before applying can make this review much cleaner.

Stated income is often used as an umbrella term. The specific product that fits a borrower depends on how they earn, document, and hold income. Truss Financial Group structures stated income loan options across several alternative documentation paths.

Best for self-employed borrowers and business owners whose deposits show stronger income than tax returns. Learn more about bank statement loans.

Best for retirees and asset-rich borrowers who may qualify from verified liquid assets. Learn more about asset depletion loans.

Best for real estate investors when the property's rental income supports the debt. Learn more about DSCR loans.

The right product is not the one with the lowest qualification bar. It is the one built around how the borrower actually generates income. Matching the loan program to the income type is often the difference between a clean approval path and a structure that does not hold up through underwriting.

Stated income mortgage rates are usually higher than conventional mortgage rates. That is built into how Non-QM lending works. When a lender accepts alternative documentation instead of tax returns, the added underwriting complexity is reflected in the rate.

For a borrower who cleanly qualifies for a conventional mortgage, the rate comparison may favor conventional financing. But for a borrower whose tax return tells the wrong story, the rate premium may be the cost of accessing financing that the conventional market does not offer.

Yes, but not in the original no-verification form. Today, stated income usually refers to Non-QM loans that verify income through bank statements, assets, or rental income instead of W-2s and tax returns.

Common candidates include self-employed borrowers, freelancers, business owners, real estate investors, retirees with assets, and borrowers with variable income that does not show cleanly on tax returns.

Most programs require bank statements, identification, proof of business or self-employment, asset documentation when relevant, and proof of down payment funds. Exact requirements depend on the loan program.

Stated income is the broader category. A bank statement loan is one specific method that uses deposit history to calculate qualifying income. In today's market, many borrowers use the terms interchangeably.

Yes. Many investors use DSCR loans, where qualification is based on the rental property's income relative to its debt service rather than the borrower's personal income.

Truss can compare how your income is best documented, whether through bank statements, rental income, or assets, and help match the loan structure to your borrower profile instead of forcing you into a conventional box.

If your tax returns do not reflect your real earning power, Truss Financial Group can help you compare bank statement, asset depletion, DSCR, and other Non-QM options around how you actually earn and document income.

Take your pick of loans

Experience a clear, stress-free loan process with personalized service and expert guidance.

Get a quote

18 min

11 min

14 min

Discover your borrowing power and plan your mortgage journey with knowledge on your side.

Get a quoteGet a quote in 3 easy steps

Tell us what you want

Fill out our online form to help us understand your financial situation and loan needs.

We get to work for you

We review your info and look for competitive rates that match your specific goals.

You get a personalized quote

You’ll receive a customized rate quote that meets your unique profile.