-2.png?width=2000&height=1125&name=White%20Gray%20Monochrome%20Business%20Company%20Blog%20Banner%20(21)-2.png "Explore everything about Non-QM loans, guidelines, benefits, and who they’re for. Learn how they help self-employed and non-traditional borrowers qualify.")

- Non-QM loans use bank statements, asset balances, or rental cash flow instead of strict tax-return income.

- Share of U.S. rate locks tagged “Non-QM” hit 7.4 % in June 2025, up from 5 % in 2024.

- Average 30-year fixed mortgage sits near 6.67 %; most Non-QM loans are priced 0.75%–1.5% higher, still well below hard-money rates.

- 35 % of U.S. workers now earn income outside traditional payroll fueling demand for alternative underwriting.

- TFG offers 10+ Non-QM programs, direct-lender pricing, and one-on-one guidance from our loan officers.

-

The Rise of Non-QM Lending

Trace the evolution from the 2008 mortgage crisis to today’s booming Non-QM market, including regulatory shifts and market data. -

Understanding Non-QM Loans

Learn definitions, core principles, key documentation types, and underwriting mechanics that differentiate Non-QM from other products. -

Non-QM vs. Qualified Mortgage (QM)

A detailed comparison chart and narrative on why Non-QM is essential for modern borrowers. -

TFG’s Flagship Non-QM Programs

Deep dives into our DSCR Loans, bank statement loans, and Asset-Based Loans with real-world case studies. -

Complete Non-QM Menu

Expanded coverage of eight additional specialized programs, each with eligibility, terms, and borrower profiles. -

Applying for a Non-QM Mortgage

Step-by-step application process, digital checklists, timeline expectations, and best-practice tips. -

Case Studies & Borrower Profiles

Four in-depth journeys showcasing how Non-QM empowers freelancers, retirees, international investors, and post-credit-event borrowers. -

Advanced Strategies for Investors & High-Net-Worth Clients

Portfolio-level tactics like blending programs, trust structures, and tax considerations. -

Expanded FAQs

Over 14 nuanced answers addressing edge cases on PMI, rate locks, co-borrowers, property types, and more. -

Conclusion & Next Steps

Key takeaways, TFG’s unique advantages, and how to kick off your application.

1. The Rise of Non-QM Lending

1.1 Historical Context

- Income documentation: Two years of tax returns or W-2s.

- Debt-to-income cap: Maximum 43% DTI.

- Term limits: 30-year amortization only; no interest-only or balloon payments.

- Fee restrictions: Points and fees capped at 3% of the loan amount.

1.2 Why Non-QM Matters Today

1. Market share surge: Non-QM accounted for 7.4% of U.S. rate locks in June 2025 up from 5% in mid-2024.

2. Gig-economy prevalence: 35% of American workers now earn significant income outside traditional payroll channels, a 12% jump since 2018.

3. Competitive pricing: While conforming 30-year fixed mortgages hover around 6.67%, Non-QM rates typically span 6.25%–8.17%, still substantially below hard-money’s 10%+ range.

4. These figures tell a simple story: as the workforce diversifies, so too must mortgage products. Non-QM loans have emerged as essential tools for:

5. Self-employed professionals: Agency principals, consultants, and creative entrepreneurs whose tax deductions obscure true earnings.

6. Gig workers: Rideshare drivers, delivery couriers, and freelance designers who rely on platform payouts rather than employer payroll.

7. Real-estate investors: BRRRR strategists and rental operators focused on property cash flow more than personal salary.

8. Retirees & HNW clients: Individuals drawing from investment portfolios or retirement accounts, seeking liquidity without selling assets.

9. Foreign nationals: International buyers lacking U.S. tax history but holding substantial overseas assets or rental income.

Non-QM’s flexibility bridges the gap between borrower reality and traditional underwriting, ensuring qualified individuals aren’t penalized by outdated rules.

1.3 Regulatory Overview

Key regulatory considerations:

- ATR compliance: Lenders must assess income, assets, debts, and credit history, regardless of documentation type.

- Consumer protections: Non-QM borrowers enjoy the same Truth-In-Lending Act (TILA) disclosures, escrow requirements, and state-level anti-predatory statutes as QM borrowers.

- No QM safe harbor: Lenders assume increased liability if ATR standards aren’t met. Partnering with reputable institutions like TFG, which follows stringent internal guidelines mitigates risk for both parties.

2. Understanding Non-QM Loans

2.1 Definition and Core Principles

- Income and Assets: How much money you earn and hold in reserves.

- Debt Obligations: Existing loans, credit cards, and other payment commitments.

- Credit History: FICO score, past delinquencies, and payment performance.

- Debt-to-Income Ratio (DTI): A borrower’s monthly debts divided by gross monthly income though Non-QM programs may stress DTI differently.

- Customize Documentation: Bank statements, asset statements, DSCR analysis, 1099s.

- Include Flexible Features: Interest-only periods, balloon payments, and amortization up to 40 years.

- Price for Risk: Rates typically 0.75%–1.5% above conforming, with fee structures adapted to borrower complexity.

- The goal: match underwriting rigor with borrower reality to approve loans responsibly and efficiently.

2.2 Key Documentation Types

I. Bank Statement Loans

2. Documentation: 12 or 24 months of personal or business checking/savings statements.

3. Income calculation: Lenders sum all deposits, subtract a conservative “expense factor” (typically 25–35%), then divide by the number of months.

Example: Total deposits over 12 months = $360,000. Expense factor 30% → $360,000 × 0.70 = $252,000 annual qualifying income → $21,000 monthly income.

4. Loan parameters: LTV up to 80% (purchase) or 75% (refinance); FICO minimum 620; loan amounts $150K–$3M.

II. Asset-Based Loans

III. DSCR (Debt Service Coverage Ratio) Loans

IV. 1099 & Gig-Economy Loans

2. Documentation: Last two years of 1099 forms; supplemental pay-stubs or platform statements (Uber, Lyft, Upwork).

2.3 Underwriting Mechanics

I. Cash Flow Stress Testing

- Lenders apply a rate-shock scenario (typically +2%), increasing the note rate to test repayment capacity.

- DTI (if used) recalculated under stress conditions to verify it remains within program limits.

II. Expense-Adjusted Income

For bank statements, an expense factor (25–35%) accounts for business or personal spending variability protecting against over-optimistic income figures.

III. Asset Imputation & Preservation

- Lenders choose an imputation period balancing asset longevity and income needs.

- Borrowers often maintain reserve requirements (e.g., 6–12 months of payments) in liquid accounts.

IV. DSCR Calibration

- Property cash flow validated via lease agreements and third-party management statements.

- Minimum DSCR threshold (0.75–1.15) ensures property performance can weather vacancies and expense fluctuations.

V. Credit & Reserve Requirements

- FICO score minimums vary by program (580–700).

- Reserve requirements typically range from 3–12 months of combined mortgage payments.

VI. Automated Analytics

TFG employs proprietary underwriting algorithms to standardize stress tests, flag anomalies, and expedite decision-making targeting conditional approvals in 5 business days or less.

By meticulously calibrating these underwriting steps, Non-QM lenders like TFG maintain responsible lending practices, protect against borrower overextension, and deliver sustainable homeownership and investment outcomes.

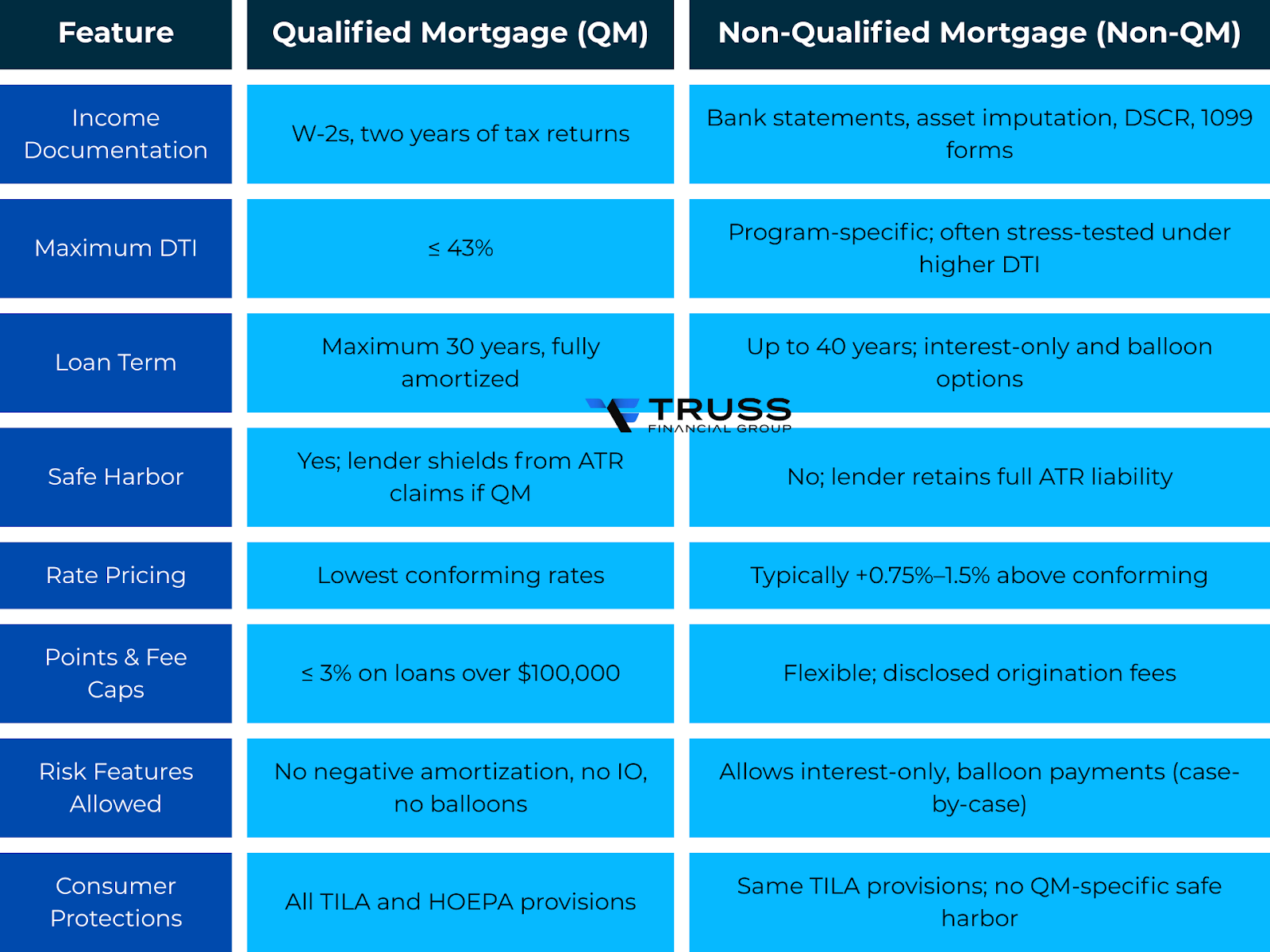

3. Non-QM vs. Qualified Mortgage (QM)

3.1 Income Documentation

1. Bank statements (12–24 months) to demonstrate cash flow.

2. Imputed asset income by dividing liquid assets over an agreed timeline.

3. DSCR analysis for rental properties, qualifying on property income alone.

1099 and gig platform statements capturing contractor revenue.

Why it matters: A graphic designer deducting software subscriptions and home office expenses may report “net” income too low for QM approval, yet bank-statement loans reveal actual deposit patterns that support higher borrowing capacity.

3.2 Debt-to-Income Ratio (DTI)

3.3 Loan Terms & Risk Features

3.4 Pricing & Fees

3.5 Safe Harbor & Liability

3.6 Consumer Protections

Summary:

While QM loans provide simplicity and legal protections for conventional borrowers, Non-QM mortgages accommodate today’s diverse income landscapes: expanding eligibility, offering flexible features, and maintaining long-term amortization. By understanding these differences, borrowers can select the product that aligns with their income profile, financial goals, and risk tolerance.

4. TFG’s Flagship Non-QM Programs

Truss Financial Group (TFG) offers three cornerstone Non-QM solutions designed to address the most common non-traditional borrower profiles. Each program balances underwriting rigor with documentation flexibility, ensuring responsible lending and streamlined closings.

4.1 DSCR Loans (Debt Service Coverage Ratio)

Key Features

1. Qualification Metric: Debt Service Coverage Ratio (DSCR) = Net Operating Income ÷ Annual Debt Service. Minimum DSCR thresholds typically range from 0.75 (for seasoned investors) to 1.15 (for more conservative underwriting).

2. Loan-to-Value (LTV): Up to 85% on purchases; 75% on refinances.

3. Rates: Start near agency-jumbo + 1.00% (approximately 7.00%–7.25% as of mid-2025).

4. Terms: 30-year amortization, with optional 10-year Interest-Only periods to maximize cash flow during lease-up or renovations.

5. No Personal Income Verification: Eliminates W-2s, tax returns, and personal DTI calculations.

Underwriting Mechanics

1. Income Documentation

- Lease agreements or rent rolls demonstrating current rental rates.

- Operating expense statements (property taxes, insurance, maintenance).

2. NOI Calculation

- Gross scheduled rent minus vacancy assumptions (typically 5–10%) and operating expenses equals Net Operating Income (NOI).

3. DSCR Computation

- Annualized NOI divided by annual debt service at the fully indexed rate must meet or exceed the program’s minimum DSCR.

4. Stress Testing

- Underwriters often apply a 2% rate “shock” to ensure viability if rates rise.

5. Ideal Borrower Profile

- Seasoned Investors expanding multi-property portfolios.

- Fix-and-Flip Operators converting short-term projects into long-term rentals.

- Portfolio Landlords seeking acquisition or refinance liquidity without disrupting personal finances

6. Case Study Snapshot

- Investor: Sarah, a BRRRR specialist with 6 single-family rentals.

- Loan Need: $1.2M purchase of a four-plex generating $8,500/month gross rent.

Underwriting:

- Vacancy allowance 8% → Effective gross income $93,840.

- Expenses $25,000 → NOI $68,840.

- Annual debt service at 7.25% on $1.2M = $98,100 → DSCR = 0.70 (approved with a 0.75 program through conservative expense adjustment).

Outcome: Closed in 18 business days, Interest-Only option to maximize early cash flow.

4.2 Bank Statement Loans

Overview

Key Features

- Documentation: 12 or 24 months of personal or business checking account statements.

- Expense Factor: Underwriters apply a standard “expense ratio” (25%–35%) to gross deposits to account for legitimate spending.

- Loan Amounts: $150K–$3M, with 80% LTV for purchases and 75% LTV for refinances.

- Minimum FICO: 620.

- Term Options: Up to 30 years fully amortized; interest-only available on select cases.

Underwriting Mechanics

1. Deposit Analysis

All credits to the account(s) are summed over the chosen period.

Transfers between accounts, loan proceeds, and non-recurring large deposits may be excluded or adjusted.

2. Expense Adjustment

Total deposits × (1 – expense factor) = annual qualifying income.

Divide by 12 or 24 to determine monthly qualifying income.

3. Backup Documentation

Profit and Loss (P&L) statements or business license may be requested to corroborate the nature of deposits.

4. Stress Testing & DTI

Qualifying income is tested against monthly obligations at the note rate + 2% (if DTI applies).

5. Ideal Borrower Profile

Consultants & Agencies whose published net income is suppressed by operating costs.

Real-World Entrepreneurs with seasonal or project-based cash flow.

Trailblazers & Creatives earning via platforms like Etsy, Amazon FBA, or YouTube.

6. Case Study Snapshot

Borrower: Raj, a freelance UX designer.

Documentation: 24 months of business account statements showing average monthly credits of $25,000.

Calculation: $25,000 × 75% = $18,750 monthly qualifying income.

Outcome: $800K purchase, 30-year fixed at 7.1%, closed in 20 days no tax returns required.

4.3 Asset-Based Loans

Overview

Asset-Based Loans allow individuals with significant investment portfolios stocks, bonds, mutual funds, CDs, and cash reserves to convert these holdings into qualifying income. Rather than liquidating or using margin, borrowers simply divide their asset balances over an imputation period to demonstrate sustainable cash flow.

Key Features

Eligible Assets: Stocks, bonds, CDs, mutual funds, money market accounts.

Imputation Period: Typically 84–120 months, chosen based on asset type and borrower goals.

Loan-to-Value: Up to 80% for purchase or refinance; cash-out options available.

Minimum FICO: 700.

Term Options: 30-year fixed; interest-only available for experienced borrowers.

Underwriting Mechanics

1. Asset Verification

2. Imputed Income Calculation

Example: $840,000 ÷ 84 months = $10,000/month.

3. Reserve Requirements

Borrowers generally maintain 6–12 months of mortgage payments in reserve accounts.

4. Tax Considerations

Portfolio performance and tax-liability analysis may influence imputation rates.

5. Ideal Borrower Profile

Retirees & Pre-Retirees drawing from investment accounts but preferring to avoid asset liquidation.

High-Net-Worth Professionals seeking new primary residences or second homes without triggering taxable events.

Executives relocating globally, leveraging stock compensation to qualify.

6. Case Study Snapshot

Client: Elena, recently retired, with $1.2M in liquid assets.

Imputation: 84-month period → $14,285 monthly qualifying income.

Loan: $900K vacation home, 30-year fixed at 6.9%, closed in 17 days, no need to liquidate stock positions.

5. Complete Non-QM Loan Menu

Below are eight additional Non-QM programs from TFG’s suite. Each is described in detail eligibility, documentation, terms, and ideal borrower profiles to help you select the right fit.

5.1 Bank Statement Home Equity Loans

Overview

Eligibility & Documentation

Terms & Pricing

Ideal Borrowers

5.2 1099 Income Loans

Overview

Eligibility & Documentation

Terms & Pricing

Ideal Borrowers

5.3 Jumbo Loans with 10% Down

Overview

Eligibility & Documentation

Terms & Pricing

Ideal Borrowers

- High-income professionals priced out of conforming limits.

- Buyers in coastal or urban markets with high home values.

- Those carrying student debt whose DTI needs flexibility.

5.4 Foreign National Loans (ITIN)

Overview

Eligibility & Documentation

Terms & Pricing

Ideal Borrowers

- International executives relocating to the U.S.

- Global investors seeking rental property cash flow.

- Students or families purchasing while awaiting permanent status.

5.5 Interest-Only Home Loans

Overview

Eligibility & Documentation

Reserves: 6–12 months of full payments (IO + eventual amortization).

Credit: Minimum FICO 640.

Terms & Pricing

Amortization: 30-year (10-year IO + 20-year amortization) or 40-year (10-year IO + 30-year amortization).

Rates: +0.25%–0.75% above comparable fully amortized terms.

Ideal Borrowers

- Rehab investors awaiting lease-up.

- Buyers expecting significant income growth.

- Borrowers with seasonal revenue (e.g., tourism properties).

5.6 Recent Credit Event Loans

Overview

Eligibility & Documentation

Terms & Pricing

Rates: +1.25%–1.75% above conforming.

Amortization: 30 years; IO possible.

Ideal Borrowers

- Individuals rebuilding credit and homeownership goals.

- Those seeking to refinance into better terms post-seasoning.

- Strategic buyers capitalizing on credit event recovery.

5.7 Commercial Small-Balance Multifamily Loans

Overview

Eligibility & Documentation

DSCR: Minimum 1.15; non-recourse available above $1M upon request.

Borrower: Single-entity LLC or individual, with proof of management experience.

Reserves: 6–9 months of debt service.

Terms & Pricing

Rates: +0.75%–1.25% above multifamily conforming benchmarks.

Amortization: 25–30 years; IO optional.

Fees: Standard origination; appraisal fee based on property size.

Ideal Borrowers

- Small syndicators testing multi-family market.

Portfolio landlords expanding beyond single-family.

Emerging developers converting properties into rentals.

5.8 Temporary Buy-Down Mortgages

Overview

Temporary rate buy-downs (2-1 or 3-2-1) reduce the mortgage rate by 2–3% in year one, tapering up annually until the note rate is reached seller-funded or builder-funded for new construction.

Eligibility & Documentation

Documentation: Standard Non-QM income verification (bank statements, assets, DSCR, 1099s).

Reserves: 6 months of full payments at note rate.

Terms & Pricing

LTV: Up to 80%–85%.

Rates: Comparable fully indexed note rate + buydown offset.

Ideal Borrowers

- First-time buyers seeking temporary affordability.

- Builders and sellers enhancing marketability.

- Buyers in lock-tight markets needing initial payment relief.

6. Applying for a Non-QM Mortgage

6.1 Discovery Call & Pre-Qualification

Initial Consultation

Soft Credit Pull

Timeline: Instantaneous results available during the call.

Pre-Qualification Letter

6.2 Digital Application & Disclosures

Online Application

Automated Disclosures

Document Checklist

6.3 Underwriting & Appraisal

Underwriting Review

Process: Underwriters verify documentation, run stress tests, and calibrate program-specific criteria (DSCR calculations, expense factors, asset imputation).

Conditional Approval: You receive a “Clear to Appraise” once underwriting confirms your file is in shape.

Appraisal Ordering

Field Work: A certified appraiser inspects the property, typically within 7–10 days of referral.

Appraisal Review

Possible Outcomes:

6.4 Clear-to-Close & Final Documentation

Clear-to-Close Issued

Final Closing Disclosure (CD)

Closing Logistics

Wire Instructions: Final wiring documents and homeowner’s insurance declarations are coordinated electronically.

6.5 Funding & Post-Closing

Wire Transfer

Recordation

County Office: The deed and mortgage are recorded, typically within 1–2 business days post-funding.

Ongoing Support

Account Access: Our portal gives you 24/7 access to your loan’s status and payment schedule.

Customer Service: Your Senior Loan Officer remains available for questions on payment, escrow, or future refinancing.

Total Timeline Estimate:

Application to Conditional Approval: ~5 business days

Appraisal & Review: ~8–12 business days

Clear-to-Close to Funding: 3–4 business days

Overall: As few as 21 business days

7. Advanced Strategies for Investors & High-Net-Worth Clients

7.1 Portfolio Diversification via DSCR Lending

Concept

- Conserve Personal Capital for renovations, acquisitions, or contingencies.

- Leverage Multiple Cash Flows across disconnected properties, spreading risk geographically and by property type.

- Scale Rapidly without personal income verification delays.

Implementation

Example

An investor acquires three single-family rentals using DSCR loans:

7.2 Blending Asset & Income Programs

Concept

- Asset-Based Loans for the lion’s share of qualifying income.

- Bank Statement or 1099 Loans to supplement imputed income with active cash flow.

- DSCR Loans on investment properties to keep consumer debt separate from business holdings.

Implementation

Example

7.3 Trust & Tax Structure Optimization

Concept

Implementation

Documentation:

Underwriting Adjustments:

Example

Summary of Section 7

- Rapidly scale rental portfolios with DSCR loans.

- Leverage multiple income sources by blending asset, bank statement, and DSCR programs.

- Maintain sophisticated ownership structures (trusts, LLCs) without forfeiting financing flexibility.

What happens if I refinance in the future?

Many Non-QM borrowers refinance into lower-cost QM loans when they accumulate traditional documentation or improve credit. TFG can handle future rate/term refinances seamlessly through our digital portal.

Do these loans report to credit bureaus?

All TFG Non-QM mortgages report payment history to major credit bureaus, helping borrowers build or rebuild credit.

Can I add a co-borrower or co-signer?

Yes. Co-borrowers must also meet program credit and documentation requirements. Non-occupant co-borrowers can help a primary occupant qualify by boosting income or reserves.

Is interest deductibility impacted?

Non-QM mortgages follow the same IRS rules: interest paid on mortgages up to $750,000 (for single filers) is generally tax-deductible. Consult your tax advisor for personalized guidance.

How do I handle taxes and insurance escrow?

Non-QM mortgages can include an escrow account for property taxes and homeowner’s insurance, just like QM. Escrow waivers are rare but possible for high-net-worth borrowers.

Can I pay off my loan early?

Most Non-QM loans permit prepayment without penalty. Always confirm in your loan documents; some jumbo or specialized products may include early-payment fees.

Are rate locks available?

Yes. Once you e-sign disclosures and lock your rate, you typically have a 45–60 day window. Extended locks are available for an additional fee.

What reserves are required?

Reserve requirements vary by program, typically 3–12 months of combined mortgage payments held in liquid accounts. Higher-risk scenarios (IO, trusts, low DSCR) trend toward 9–12 months.

Can I use a Non-QM loan on a second home or investment property?

Yes. Many programs support primary, second-home, and investment loans. DSCR products specifically target investment properties, while Bank Statement and Asset-Based loans can finance second homes.

How do I qualify after bankruptcy or foreclosure?

Certain Non-QM programs allow day-one eligibility post-bankruptcy discharge, short sale, or foreclosure with up to 75% LTV. Rates improve and LTV increases (to 80–85%) after 24 months of seasoning.

Is a Non-QM loan the same as a hard-money loan?

No. Hard-money loans are short-term, asset-only, high-rate/fee products typically from private lenders. Non-QM mortgages are fully underwritten, amortized over 30–40 years, report to credit bureaus, and adhere to ATR standards.

Is PMI required for Non-QM loans?

Private Mortgage Insurance is rare. Many Non-QM products bake risk into the rate and require higher reserves instead. Some 90% LTV programs offer lender-paid mortgage insurance as an alternative to borrower-paid PMI.

Are Non-QM mortgages more expensive than conforming loans?

Yes, typically pricing includes a 0.75%–1.5% rate premium over conforming rates to account for alternative documentation risk. However, even at these levels (6.25%–8.17% as of mid-2025), Non-QM remains far cheaper than hard-money (10%+) or private money lenders.

What documentation is accepted for Non-QM loans?

When applying for a loan, work with a senior loan officer to identify your primary income type, whether you're self-employed, asset-based, or earning rental income. This helps match you with the right loan structure.

Clarify your borrower goals: Are you purchasing or refinancing? Do you need cash out, or are you focused on long-term investment growth? Your purpose shapes the best-fit loan product.

Assess your risk tolerance. Are you comfortable paying a premium for interest-only options? Do you have strong reserves? These factors affect flexibility and cost.

Finally, define your timeline and holding strategy. A short-term flip requires a different approach than a long-term hold.

Aligning your profile with the right loan program improves approval chances, lowers costs, and supports your real estate goals.