15 min read

15 min read

Most homeowners are sitting on substantial equity but struggle to access it without refinancing their entire mortgage at higher rates. NftyDoor HELOC offers a better solution: a fully digital home equity line of credit that lets you tap $25K to $500K in days, not weeks, while keeping your existing low-rate mortgage intact.

The rate you get depends on how you access NftyDoor. Apply directly through their website, and you pay retail pricing. Work with a wholesale lending partner like Truss Financial Group, and you access the same platform at wholesale rates (upto $750K) that individual borrowers can't negotiate on their own.

This guide explains what NftyDoor is, how HELOCs work, and why wholesale partners deliver better terms than going direct.

NftyDoor is a division of Homebridge Financial Services, Inc., one of the largest privately held mortgage lenders in the United States. That backing means NftyDoor operates under the same federal and state licensing, regulatory oversight, and consumer protection frameworks as any major financial institution. The platform was specifically designed for home equity lending with a fully digital infrastructure that handles credit approval, income verification, title work, and closing entirely online.

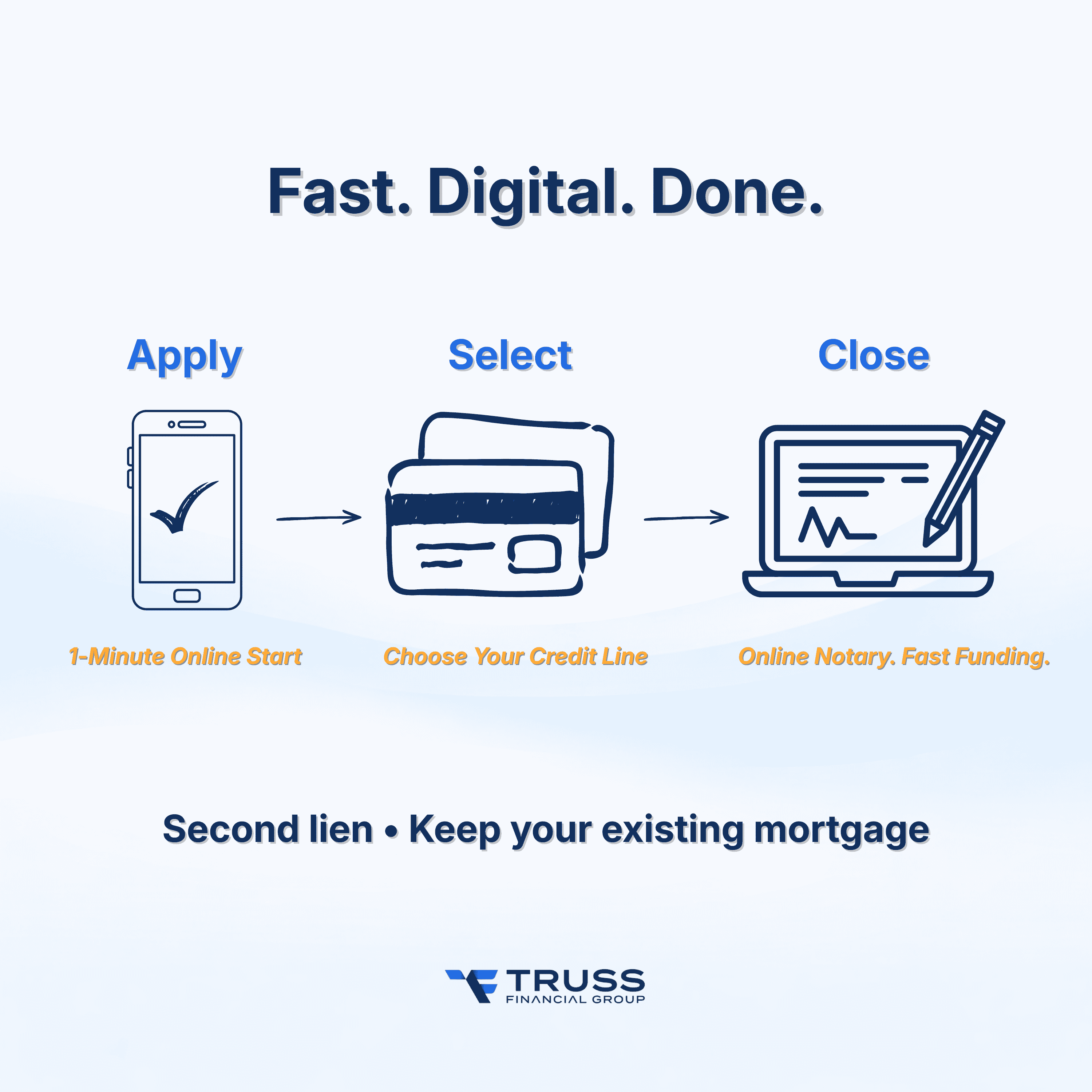

NftyDoor HELOC is a second lien product, sitting behind your existing first mortgage. This allows you to preserve your low-rate primary mortgage while accessing new funds through a revolving credit line for primary residences, second homes, or investment properties.

NftyDoor simplified what used to be a 30-to-45-day ordeal into three straightforward steps:

Complete a 1-minute online application with no paperwork required upfront. You'll receive instant pre-qualification based on a soft credit pull that won't impact your credit score. The system evaluates your home equity, income, and credit profile to determine your borrowing capacity.

Once pre-qualified, select your initial draw amount from your approved credit line. NftyDoor offers lines from $25K minimum up to $750K maximum (with Truss Financial Group), and you decide how much to access immediately versus keeping in reserve for future use during the draw period.

Schedule an online notary closing (no branch visit, no title office appointment required). For primary residences, funds are disbursed three days after closing to comply with the federal rescission period. Investment properties and second homes fund in as few as one business day since the rescission period doesn't apply.

Throughout the process, borrowers can track their loan status through NftyDoor's HELOC Loan Tracker portal. What traditionally required stacks of paperwork, multiple in-person appointments, and weeks of back-and-forth now happens almost entirely online.

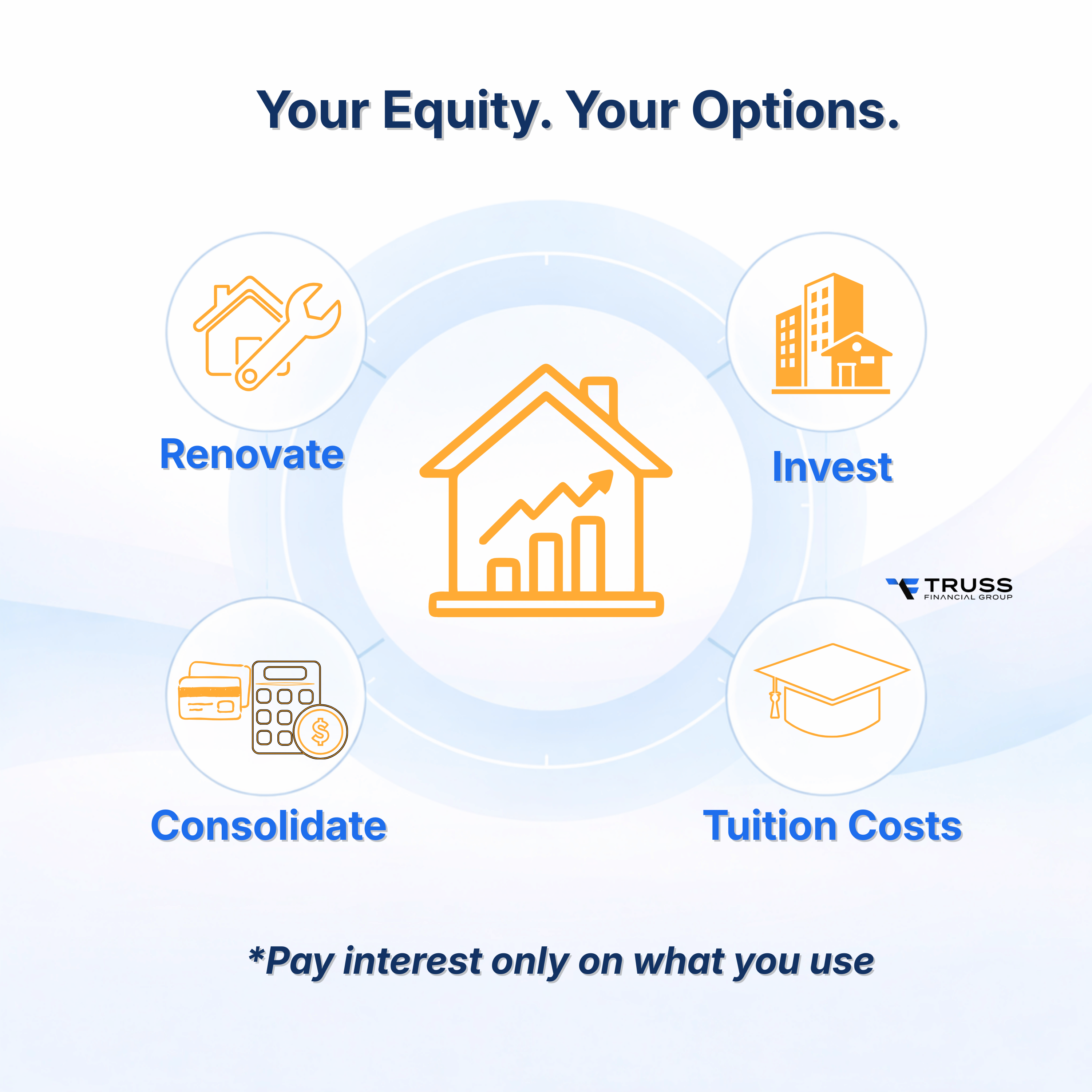

A home equity line of credit gives you flexible access to funds for virtually any purpose:

Beyond these common scenarios, borrowers use HELOCs for tuition and education costs, financing a vehicle, covering major expenses, or managing unexpected financial needs. The revolving structure means you only pay interest on what you draw, not your full credit limit.

NftyDoor HELOCs carry variable interest rates that move with the Prime Rate plus a lender's margin based on your credit profile and loan-to-value ratio. Variable rates mean your monthly payments can rise or fall with market conditions, something borrowers should plan for when budgeting.

During the draw period, interest-only payments are typical. You're only paying interest on your outstanding balance, not the full available credit line. This keeps monthly payments lower while you're actively using the funds. After the draw period ends, the repayment period begins, requiring principal and interest payments on whatever balance remains.

|

Feature |

Details |

|

Interest Rate Type |

Variable (Prime Rate + lender's margin) |

|

Draw Period Payments |

Interest-only on the outstanding balance |

|

Repayment Period Payments |

Principal + interest (fully amortized) |

|

Closing Costs |

Lower than cash-out refinance |

|

Rate Advantage |

Wholesale partners beat direct retail pricing |

Here's the critical piece: rates through wholesale lending partners typically beat NftyDoor's direct retail pricing. Same loan product, same digital platform, same closing process, just better terms because wholesale lenders bring volume and established relationships that unlock pricing individual borrowers can't access on their own.

When you apply directly through NftyDoor's website, you're accessing their retail channel, the same as walking into a bank branch and asking for their advertised rates. The pricing is fine, but it's built for individual consumers without negotiating power.

Wholesale partners deliver:

Wholesale mortgage brokers like Truss Financial Group aren't middlemen adding cost. They're the channel that removes cost by leveraging lender relationships on your behalf. This model is standard, regulated, and common across the U.S. mortgage industry. The only difference is whether you know how to ask for it.

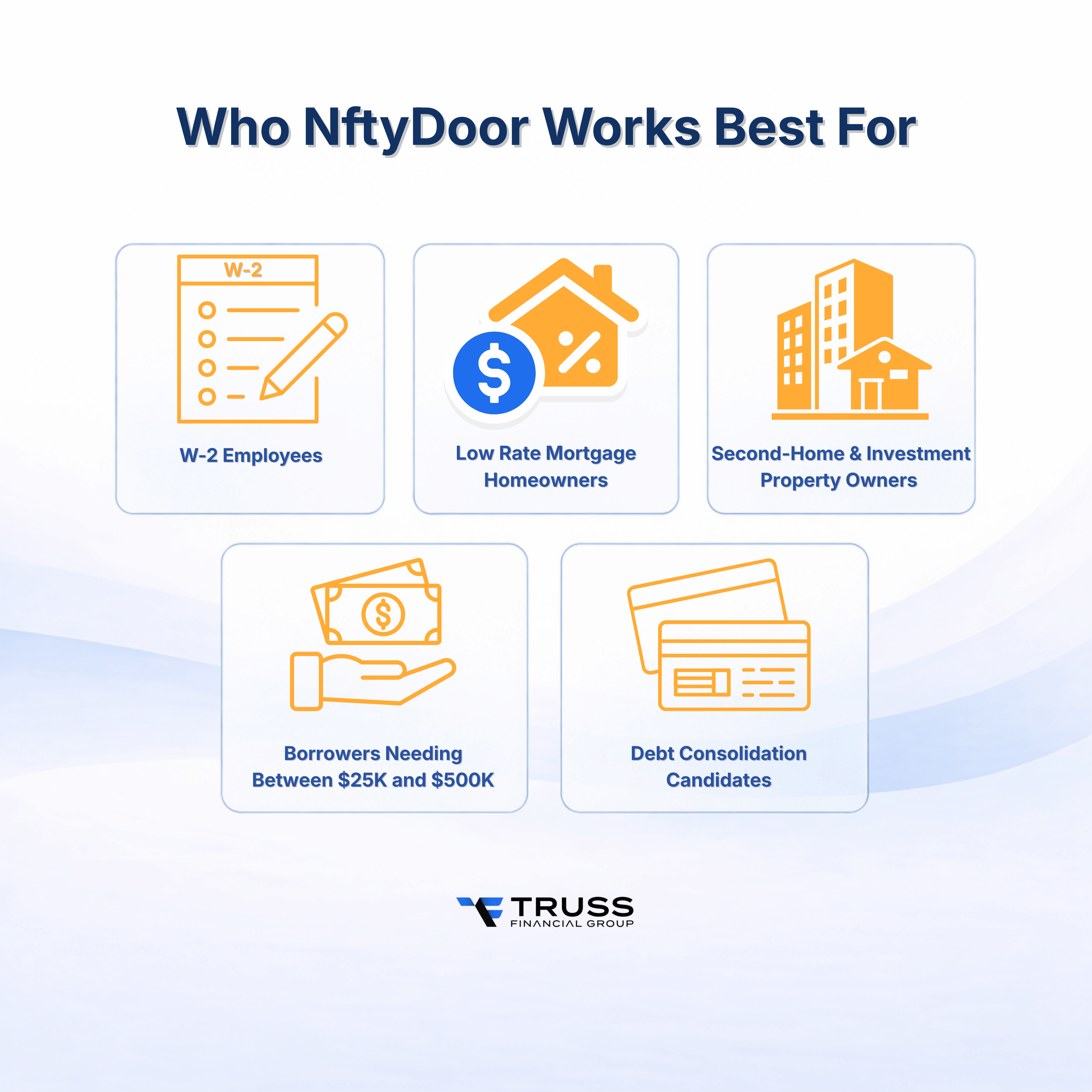

NftyDoor's automated underwriting excels with clean, straightforward borrower profiles:

For straightforward scenarios like these, NftyDoor's automation delivers exactly what modern borrowers want: speed, transparency, and minimal friction. But not every borrower fits that mold.

NftyDoor's automated platform is built for efficiency, not complexity. When your financial profile requires human expertise, wholesale lending partners fill the gap.

The role of wholesale partners isn't to replace NftyDoor's platform but to extend its reach. For borrowers who fit NftyDoor's automated criteria, wholesale lenders submit your loan at better pricing. For borrowers who don't fit the automated mold, they find the right product and structure the file to maximize approval odds.

NftyDoor isn't just faster. It's a fundamentally different borrower experience built for the modern homeowner who values speed and transparency. But speed doesn't mean less rigor. NftyDoor still verifies income, title, employment, credit history, and home value. The difference is how they verify, not whether they verify.

|

Feature |

NftyDoor |

Traditional Bank |

|

Application Process |

1-minute digital app |

Lengthy paper application |

|

Timeline to Close |

Under 1 week is typical |

30-45 days typical |

|

Paperwork Required |

No upfront paperwork |

Extensive documentation |

|

Closing Location |

Online notary |

In-person closing |

|

Funding Speed |

1-3 days post-closing |

Additional days after closing |

|

Rate Type |

Variable rate |

Variable or fixed rate |

|

Borrower Experience |

Fully digital |

Branch-dependent |

Traditional banks require in-person appointments, physical document submission, and manual underwriting that stretches timelines to 30 or 45 days. Credit unions often move even slower despite offering competitive rates. NftyDoor's digital infrastructure eliminates these bottlenecks without sacrificing the due diligence that protects both lender and borrower.

Getting wholesale access to NftyDoor takes three steps:

Step 1: Contact a wholesale lender. A loan officer reviews your financial profile and determines whether NftyDoor is the right fit or if another HELOC product better serves your needs. Not every borrower belongs on NftyDoor's platform, and experienced brokers will tell you that upfront.

Step 2: Your wholesale partner submits your application to NftyDoor at wholesale pricing. You get the same 1-minute application, instant pre-qualification, and digital closing experience, just with better rate terms than you'd receive going direct.

Step 3: NftyDoor's process takes over. Their platform handles underwriting, title work, and closing coordination. You schedule your online notary appointment, and funds hit your account according to the timeline for your property type.

Wholesale relationships are already established. There's no extra complexity for you as the borrower. You simply get better pricing because your loan is submitted through the wholesale channel instead of the retail window. It's that straightforward.

If you're looking for faster HELOC closing timelines or need to compare second lien HELOC options, working with an experienced mortgage broker gives you access to the full range of products available based on your specific situation.

NftyDoor is a fully digital HELOC platform and division of Homebridge Financial Services that offers home equity lines of credit $25K to $500K ($750K with mortgage brokers) with a 1-minute application and fast funding timelines.

NftyDoor uses a three-step process: apply online in one minute, choose your initial draw amount, and close with an online notary. Funds are disbursed within 1-3 days, depending on your property type.

Yes. NftyDoor is a division of Homebridge Financial Services, Inc., a nationally licensed mortgage lender operating under full federal and state regulatory oversight.

Investment properties and second homes can often be funded in as few as three to five business days from the start of the application, as they are exempt from the federal three-day rescission period required for primary residences. Primary residences typically close within a week; however, per federal law, funds are disbursed on the fourth business day after the rescission period ends (which lasts three business days following the signing of loan documents).

Credit score requirements vary by lender and borrower profile, but most HELOC programs require a minimum credit score of around 640-680 for competitive pricing.

NftyDoor offers credit lines from $25K minimum to $500K maximum based on your available home equity and qualification factors. With mortgage brokers, you can access up to $750K.

Yes. NftyDoor provides HELOCs for primary residences, second homes, and investment properties, with faster funding timelines for non-primary residences.

Direct rates are retail pricing available to individual consumers. Wholesale rates are lower rates and fees available through lending partners due to volume relationships and professional origination.

Wholesale lending partners get you better pricing than going direct through established relationships with NftyDoor. For complex borrower profiles (self-employed, investors, high-limit needs), they also provide loan structuring expertise that improves approval odds.

It depends on your situation. If you have a low-rate first mortgage you want to keep, a HELOC preserves that rate while giving you access to new funds. A cash-out refinance replaces your entire mortgage, which only makes sense if current rates are competitive with your existing rate.

NftyDoor changed the HELOC experience with speed, digital convenience, and backing from a nationally licensed lender. For straightforward borrower profiles, the platform delivers exactly what modern homeowners need.

But pricing depends entirely on how you access it. Apply directly, and you pay retail rates. Work with wholesale lending partners, and you get better terms: same platform, lower pricing.

For self-employed borrowers, investors, or high-limit scenarios above $500K, experienced mortgage professionals structure loans correctly before submission, often making the difference between approval and denial.

If you're exploring cash-out refinance options or comparing second lien HELOC alternatives, loan officers at Truss Financial Group can walk you through the decision that aligns with your financial goals.

Take your pick of loans

Experience a clear, stress-free loan process with personalized service and expert guidance.

Get a quote

15 min

.png?width=352&name=xxxxxx%20header%20(13).png)

17 min

2 min

Discover your borrowing power and plan your mortgage journey with knowledge on your side.

Get a quoteGet a quote in 3 easy steps

Tell us what you want

Fill out our online form to help us understand your financial situation and loan needs.

We get to work for you

We review your info and look for competitive rates that match your specific goals.

You get a personalized quote

You’ll receive a customized rate quote that meets your unique profile.