14 min read

14 min read

If there’s one thing you need to know when you’re drowning in multiple debts and feeling overwhelmed with the mountain of monthly payments, you’re not alone. In fact, a recent survey carried out this year found that around 48 % of loan applicants have been denied at some point. The numbers are raging, but we are here to provide the solution to your problems.

Debt consolidation loans are a good option, since they help simplify your monthly debt payments and help save money on interest rates. So, instead of managing several different loan payments, all with different due dates and rates, you’ll just have to focus on one new monthly payment.

Yes, consolidating debt with a high debt-to-income ratio can be challenging. The good news, however, is that there are proven strategies to get you back on track, debt-free. Understanding how to calculate your debt-to-income ratio and your available loan options means you’re already halfway there.

Here’s everything you need to know to present your case in the strongest way possible.

____________________________________________________________________________

Debt consolidation loans combine multiple debts into one, simplifying repayment and potentially lowering interest costs.

High DTI (over 43%) limits access to traditional loans, but specialized lenders and strategies can still get you approved.

Balance transfer cards with 0% APR are ideal for short-term credit card debt relief.

Home equity loans or cash-out refinances are best for borrowers with property equity and high DTI.

Debt management programs negotiate directly with creditors, lowering APRs and combining payments into one manageable monthly amount.

Credit score still matters, so keep utilization low and make consistent payments to improve approval chances over time.

____________________________________________________________________________

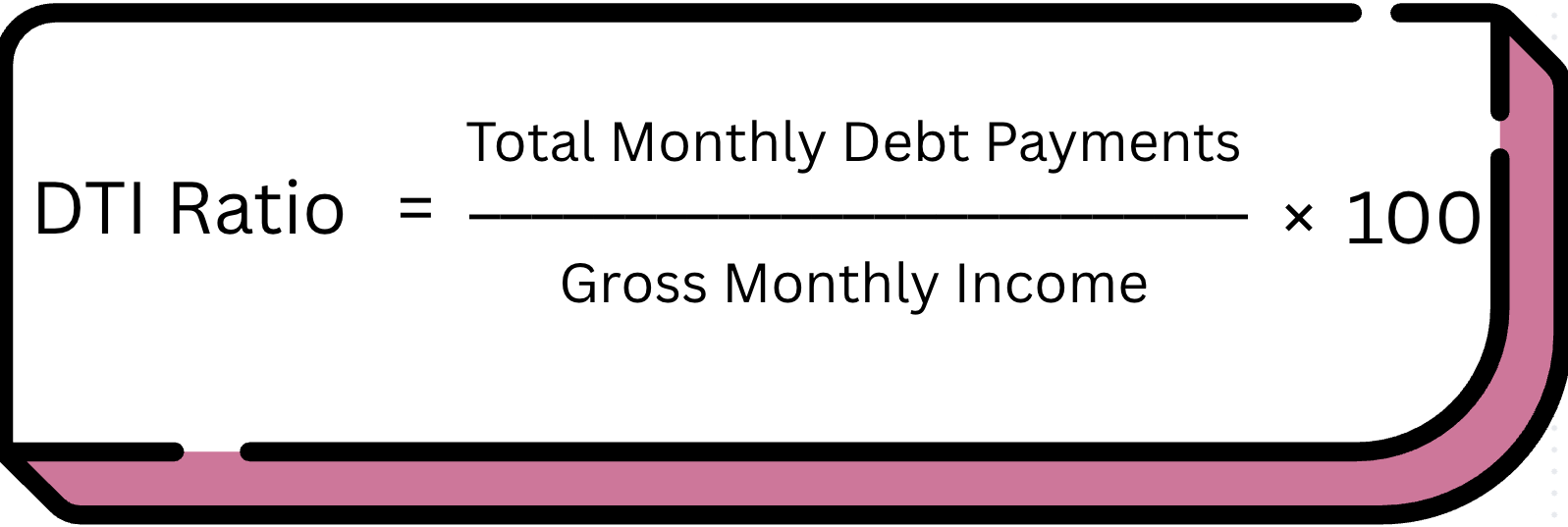

Your debt-to-income ratio is the percentage of your gross monthly income used for debt payments. This includes mortgage, car loans, credit cards, and student loans. This single figure can give lenders the complete picture of your financial health and whether you’re able to take on a new loan.

To calculate your DTI ratio:

If you have $5,000 in monthly debt payments and earn $8,000 in monthly pre-tax income, your DTI would be 62.5 %.

Here’s how lenders actually view DTI risk, as opposed to what they’re telling you in their marketing:

|

DTI Range |

Reality Check |

Your Approval Odds |

|

0 - 36 % |

Golden star |

90 %+ with decent credit |

|

37 - 43 % |

Still acceptable, barely |

60 - 70 % approval |

|

44 - 50% |

Now you're in trouble |

20 - 30 % approval |

|

50 %+ |

Good luck with that |

Sub - 10 % with traditional lenders |

A high debt-to-income ratio doesn’t just make it harder for you to get your loan approved; it can also trap you in predatory interest rates, leaving you worse off than you started. Most traditional lenders put hard stops at 43 % DTI, regardless of what their websites claim about ‘flexible underwritings’.

A common rule of thumb lenders go by is the 28/36 rule, which recommends no more than 28% of gross monthly income on housing and 36% on total debt.

When it comes to getting approved for a debt consolidation loan, your credit score plays an important role. However, here’s what most banks won’t tell you: a bad credit score doesn’t automatically disqualify you, that is, if you know where to look.

Three big factors that determine your credit score include: credit utilization, payment history, and credit history length.

Improving your credit score doesn’t have to be as difficult as the credit industry wants you to believe. Most score improvements can come from two factors that you can control: making consistent payments and keeping your credit card balances low.

And, did we mention patience?

Most people look for debt consolidation loan options because of their credit card debt, which, quite frankly, is the most expensive debt people carry. With average interest rates hovering around 20 - 25 %, credit card debt can compound faster than you can pay it down.

By consolidating credit card debt into a single loan, you can simplify payments and even slash interest rates in half or more. Instead of juggling multiple credit card payments with different due dates, you now have one predictable monthly payment that actually makes progress on your balance.

Balance transfer credit cards offer 0 % introductory APRs, which help you save money on interest. But, there’s a catch here. They require a good credit score, one that most high-DTI borrowers don’t have.

Most credit card debt consolidation strategies include debt management programs, balance transfer credit cards, and personal loans. The key here is to match with the right strategy that will help your specific situation.

There are several consolidation loan options to choose from, each with its own advantages and requirements. Personal loans, for example, are one of the most common choices. They offer fixed interest rates as well as predictable monthly payments over terms running from 2 to 7 years.

Then there are secured loans, such as home equity loans, which have lower interest rates but require collateral. This means you could risk losing your home if you’re unable to clear the payments.

Unsecured loans, like personal loans, have higher interest rates but don't require collateral, making them safer from an asset protection standpoint. The only downside is that lenders may be a tad bit selective about who they approve.

At the end of the day, choosing the right consolidation loan option really just depends on your current financial situation, credit score, and debt obligations. Before committing to any option, make sure you’ve considered all factors such as origination fees, loan terms, and whether you can realistically afford the new monthly payment.

Working with a certified credit counselor can be really helpful when you’re navigating debt consolidation with a high DTI ratio. They can help create tailored debt management plans as well as negotiate with creditors on your behalf, such as reducing your monthly debt payments by 20 to 40 % through credit concessions.

This helps you secure better terms than you could have achieved on your own.

You also have the option of working with non-profit credit counseling agencies that provide free or low-cost services, which include debt management programs and financial education. These agencies can review your financial situation and help you understand your options while creating a realistic plan for you to follow.

Credit utilization is essentially the amount of available credit used and it’s calculated by dividing your current credit card balances by your total available credit limits across all cards.

High credit utilization can affect your credit scores negatively, which is why it’s a good rule of thumb to keep it under 30 %. However, the best scores typically come from utilization rates that are below 10 %. Maintaining a good credit score increases your chances of a loan approval significantly.

Some quick ways to improve your ratio are:

Balance transfer credit cards offer 0% introductory APRs, which can save money on interest and help you pay off credit card debt faster. These promotional periods typically last 12-21 months, which gives us a good window to clear out your debts without the added burden of compound interest.

Balance transfer credit cards require a good credit score and may charge balance transfer fees, which are usually around 3 to 5 % of the transferred amount. Despite the fees, though, the interest savings far outweigh the costs.

Since balance transfer credit cards are a great tool for consolidating credit card debt, make sure you:

A cash-out refinance involves converting home equity into cash to pay off existing debt, such as credit card debt or auto loans. This strategy can be particularly effective if you have significant equity and high-interest debt.

Instead of letting credit card companies collect 18 - 25% interest while your home equity sits idle, you're borrowing against your house at mortgage rates to eliminate those high-interest balances. Cashing out refinance allows you to consolidate debt into a single loan with lower interest rates.

The math here is quite compelling.

While credit cards might be charging you 22% annually, mortgage rates typically hover around 6 - 8%, which is a massive difference that can save you thousands.

Of course, this strategy isn't for everyone.

You'll need decent credit and substantial equity in your home; most lenders want you to keep at least a 20 % ownership stake after the refinance. The application process tends to be more forgiving than personal loans since your house serves as collateral.

It’s important to understand that you’re putting your home on the line here. This strategy could go two ways.

When you’re ready to apply for a debt consolidation loan, gather all your financial documents. This includes:

Having everything organized upfront can speed up the application process and improve your chances of approval.

Next, compare loan options from different lenders. What you’re looking for here is:

It’s tempting to focus on just the monthly payment, but you need to look at the total cost over the life of the loan.

Before signing, make sure you’ve thoroughly read through and understood the loan terms and conditions. You also want to pay special attention to variable vs. fixed rates, prepayment penalties, and what happens if you miss payments.

Whether or not you’re eligible for a loan depends entirely on your credit score, debt-to-income ratio, and income stability. Most lenders are interested in whether you have a sufficient income to handle the new monthly payment on top of your other obligations.

Most lenders have different eligibility criteria, so make sure you’ve done your homework on comparing loan options from multiple sources. What one lender rejects, another might approve!

At the end of the day, improving your credit score and reducing your debt-to-income ratio can really increase your chances of loan approval. Even small improvements can make a huge difference in both approval odds and the interest rates you're offered.

The best way to go about this is by being honest about your financial condition. Lenders are bound to verify your information anyway, might as well build trust while you’re at it.

Managing a loan repayment and avoiding default can be made easier if you create a budget for yourself and stick to it. After all, your consolidation loan is only as good as your commitment to changing the spending habits that got you into debt in the first place.

Here’s how you can stay on track:

Maintaining financial stability isn’t your finish line; it’s your starting step. It requires ongoing effort and attention to your financial condition, with zero tolerance for backsliding.

If you’re looking for real, lasting results, make sure you do this:

Yes, though your options may be limited and interest rates higher.

Home equity loans, cash-out refinancing, and balance transfer credit cards typically offer the best rates and highest approval odds for high DTI borrowers.

If your DTI is too high, you may face loan rejections and higher interest rates. You have plenty of alternative options, though, such as debt management programs or working with specialized lenders who focus on high DTI borrowers.

Yes, home equity loans often allow higher DTI ratios (up to 50-55%) because your home serves as collateral, reducing the lender's risk.

Absolutely. You'll need to be strategic about which lenders you approach and may need to consider secured loan options or work with specialized lenders, but you can qualify.

A 7% DTI is excellent and should qualify you for the best available interest rates and loan terms from virtually any lender.

The maximum DTI varies by lender and loan type. Most traditional personal loans cap at 36 to 43 % DTI, while secured loans may allow up to 50 to 55%. Debt management programs, on the other hand, have no DTI limits.

A 50 % DTI is high, but it doesn’t automatically disqualify you. Traditional unsecured loans probably won’t work out for you. Instead, look for secured loan options, balance transfer credit cards, or debt management programs.

Finding a debt consolidation loan with a high debt-to-income ratio requires strategy, persistence, and a refusal to settle for generic advice. Initial rejections are part of the process and not the end of the road.

The borrowers who actually win this game know their numbers.

Truss Financial Group specializes in those hard-to-place cases. If you have a high DTI, your credit score isn’t perfect, and the big banks have turned you down, good. It’s time to get strategic and we can help.

The support exists, now it’s your move. Get in touch with us today.

Take your pick of loans

Experience a clear, stress-free loan process with personalized service and expert guidance.

Get a quote

15 min

4 min

-1.png?width=352&name=Blog%20covers%20(2)-1.png)

19 min

Discover your borrowing power and plan your mortgage journey with knowledge on your side.

Get a quoteGet a quote in 3 easy steps

Tell us what you want

Fill out our online form to help us understand your financial situation and loan needs.

We get to work for you

We review your info and look for competitive rates that match your specific goals.

You get a personalized quote

You’ll receive a customized rate quote that meets your unique profile.