11 min read

11 min read

.png)

If you’ve ever tried to open a home equity line of credit, you already know the slowest and most annoying part of the process: the appraisal. Scheduling it, paying for it, waiting weeks, only to be told your home came in lower than expected.

The good news? In 2026, many homeowners can access a no-appraisal HELOC using modern valuation tools instead of a full in-person inspection.

.png?width=2240&height=1260&name=xxxxxx%20header%20(55).png)

This guide breaks down the best no-appraisal HELOC options, who they work best for, and how lenders decide whether an appraisal can be waived, without rehashing basic HELOC theory you’ve already heard a hundred times.

Think of a HELOC like a reusable credit card backed by your home’s value. The difference today is how that value gets determined.

A “no-appraisal HELOC” doesn’t mean the lender ignores your home’s value. It means the lender uses automated valuation models (AVMs) or limited hybrid methods instead of a traditional full appraisal.

Instead of sending an appraiser to physically inspect your property, lenders may rely on:

This can eliminate appraisal fees (often $350–$800) and reduce approval time from weeks to days.

If you want a deeper breakdown of how appraisal waivers work and when lenders allow them, see our detailed guide: Can You Get a HELOC Without an Appraisal?

This article assumes you already know it’s possible, and focuses on choosing the best option.

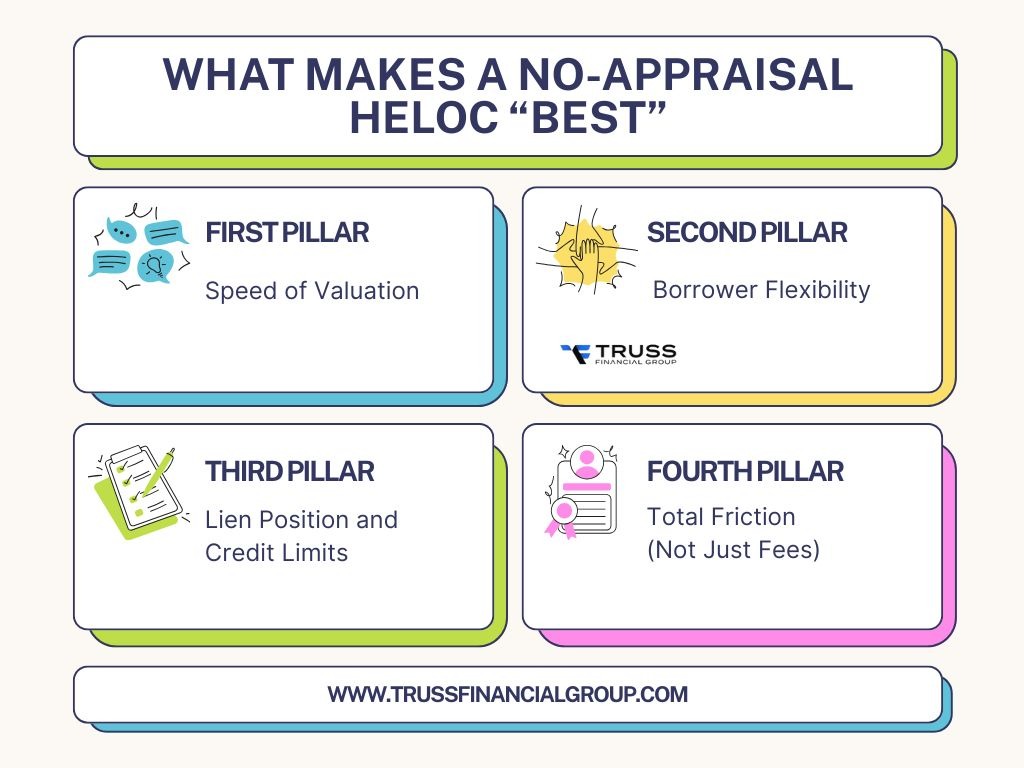

Not all no-appraisal HELOCs are created equal. The “best” option depends less on rates and more on who the loan is designed for.

Here’s what actually matters.

AVM-based HELOCs can complete property valuation in minutes or hours instead of 1–3 weeks. Faster valuation usually means faster funding.

Some lenders only waive appraisals for borrowers with pristine credit and low debt-to-income ratios. Others design programs for self-employed borrowers, seniors, or high-DTI profiles.

First-position HELOCs and lower loan-to-value requests are more likely to qualify for appraisal waivers. Most lenders cap borrowing at around 85% of the home’s current market value minus existing mortgage balance.

“No appraisal” loses its meaning if the lender replaces it with excessive income verification, documentation requests, or slow manual underwriting.

This is where most comparison articles fail. The best no-appraisal HELOC depends on who you are, not who has the biggest marketing budget.

Self-employed homeowners often get stuck twice, once on income verification and again on property valuation.

Some lenders allow:

This structure works well for business owners, freelancers, consultants, and 1099 earners who have strong equity but inconsistent taxable income.

Programs like No Tax Return HELOCs and Bank Statement Mortgages are often paired with digital valuation methods to streamline approvals.

Seniors frequently have:

A Senior HELOC may allow appraisal waivers when equity is strong and credit history is stable, even if income is limited. In some cases, lenders focus more on available equity and credit profile than traditional debt-to-income ratios.

This makes HELOCs a useful alternative to personal loans or asset liquidation for retirees managing ongoing expenses or unexpected costs.

Real estate investors and high-DTI borrowers are often excluded by traditional banks, even with strong assets.

Some lenders structure HELOCs similarly to DSCR HELOAN programs, where the focus shifts away from personal income and toward asset performance or equity position.

When loan amounts are conservative and equity is strong, AVM-based valuations can still be used, especially for single-family homes in active markets.

If speed matters, digital underwriting is the differentiator.

Digital HELOCs combine:

This approach reduces approval timelines dramatically compared to traditional credit unions and large banks.

Lenders like Truss Financial Group specialize in these alternative-friendly structures, offering digital HELOC programs that serve seniors, self-employed borrowers, and high-DTI homeowners without relying on old-school appraisal bottlenecks.

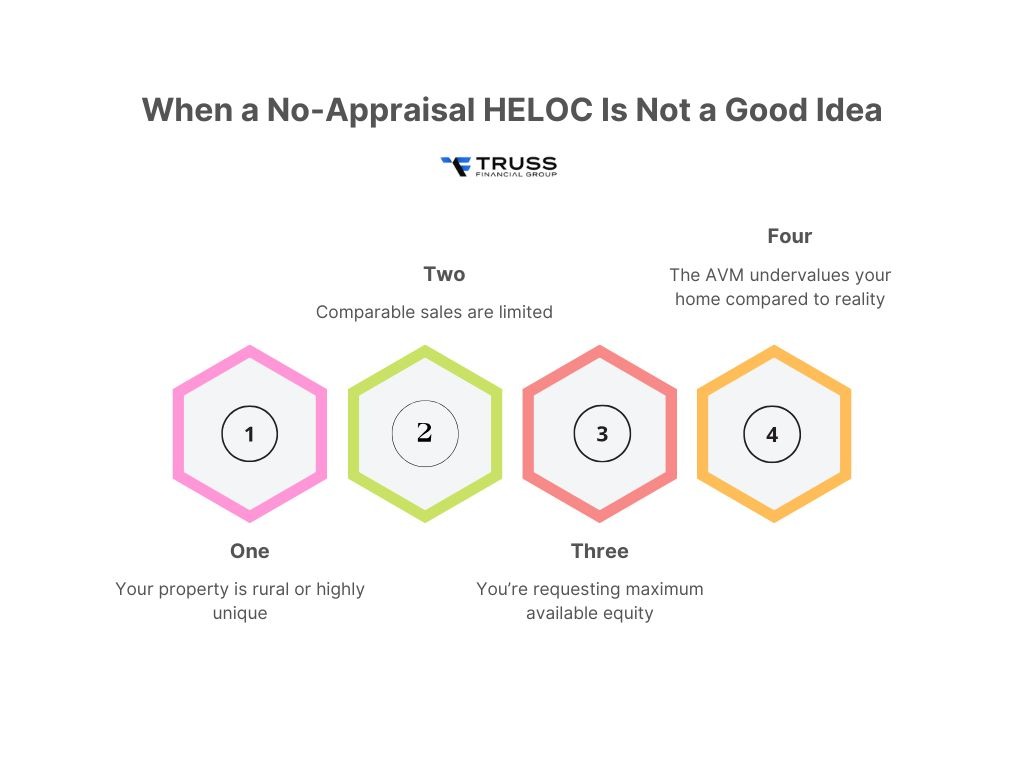

No-appraisal doesn’t mean no-risk. In some cases, a full appraisal is actually the better option.

You may not qualify for an appraisal waiver if:

Automated models can sometimes be conservative. If your home has custom upgrades or unusual features, a full appraisal may unlock a higher credit limit.

Before committing, it helps to understand alternatives.

A HELOC offers flexible access and variable rates, while a home equity loan provides a lump sum with fixed payments. Appraisal requirements vary for both.

Personal loans don’t require appraisals but often carry higher interest rates and shorter loan terms.

Cash-out refinancing replaces your existing mortgage and almost always requires a full appraisal making it slower and more expensive in many cases.

While every lender differs, borrowers most likely to receive appraisal waivers typically have:

Preparing documents early and understanding your equity position can significantly speed up the process.

A no-appraisal HELOC can be a powerful financial tool, but only when the structure fits your situation.

The “best” option isn’t about chasing the lowest advertised rate. It’s about:

Lenders like Truss Financial Group focus on modern underwriting, digital valuation, and alternative borrower profiles, making them a practical choice for homeowners who don’t fit inside a traditional bank box.

If you’re exploring a Digital HELOC, Senior HELOC, or No Tax Return HELOC, understanding these distinctions upfront can save you time, money, and unnecessary frustration.

Who has the best HELOC right now?

Who has the best HELOC right now?There isn’t a single best HELOC for every borrower. The right option depends on how much equity you have, how your income is documented, and how flexible the lender is with appraisals and underwriting. Borrowers who prioritize no-appraisal options, no-documentation programs, and faster digital approvals often work with alternative lenders rather than traditional banks.

In fact, an independent comparison by LendEDU listed Truss Financial Group among the top no-documentation lenders, highlighting its focus on non-QM, senior-friendly, and digital HELOC structures. The best HELOC is ultimately the one that aligns with your equity position, borrowing needs, and long-term financial goals, not just headline rates or marketing claims.

Yes, it is possible in some cases. Certain lenders approve HELOCs without a traditional in-person appraisal by using automated valuation models (AVMs) or hybrid valuation methods instead. These tools estimate a home’s current market value using recent sales data, comparable properties, and market trends.

However, not all borrowers or properties qualify. Approval depends on factors such as available equity, credit profile, loan amount, and property type.

You may be able to avoid a full appraisal by meeting conditions that lower risk for the lender, including:

Even when an appraisal is waived, lenders still verify property value using market data and internal valuation models.

Not always. While many traditional banks and credit unions require a full appraisal, some lenders waive it when automated or hybrid valuation methods provide sufficient accuracy.

Appraisal requirements vary by lender and are influenced by loan-to-value ratio, property characteristics, and borrower risk profile.

No. Some HELOCs are approved without a full appraisal, particularly when the lender can confidently determine the property’s value through AVMs or recent comparable sales. Others, especially higher loan amounts or unique properties may still require a full appraisal.

Yes, Lenders like Truss Financial Group offer home equity loans using automated or hybrid valuations instead of a full appraisal. However, appraisal waivers are more common with HELOCs than with lump-sum home equity loans. Eligibility depends on equity, credit strength, and property type.

Common disqualifiers include:

Each lender sets its own qualification standards.

The “65% rule” refers to a conservative guideline used by some lenders, where the total loan balance (existing mortgage + HELOC) cannot exceed 65% of the home’s current market value.

This rule isn’t universal, but lower loan-to-value ratios often increase the chances of approval, especially for no-appraisal or fast-track HELOCs.

You may be disqualified from a HELOC if you have:

Some alternative lenders, such as Truss Financial Group, offer more flexible underwriting for seniors, self-employed borrowers, and high-DTI profiles, but minimum standards still apply.

Take your pick of loans

Experience a clear, stress-free loan process with personalized service and expert guidance.

Get a quote.png?width=352&name=xxxxxx%20header%20(44).png)

18 min

3 min

15 min

Discover your borrowing power and plan your mortgage journey with knowledge on your side.

Get a quoteGet a quote in 3 easy steps

Tell us what you want

Fill out our online form to help us understand your financial situation and loan needs.

We get to work for you

We review your info and look for competitive rates that match your specific goals.

You get a personalized quote

You’ll receive a customized rate quote that meets your unique profile.