13 min read

13 min read

.png)

If you're exploring a home equity line of credit (HELOC), one of the first questions you'll face is: how many bank statements do I actually need? The answer isn't one-size-fits-all. It depends on your income source, employment type, and the specific HELOC program you're applying for.

Traditional W-2 employees might only need 2–3 months of personal bank statements. Self-employed borrowers, on the other hand, typically need 12–24 months of business bank statements to verify income. And if you're a retiree or investor? Some programs, like Truss Financial Group's Equity Select HELOC for seniors, don't require bank statements at all, relying instead on your home's equity and credit profile.

This guide breaks down exactly what lenders look for, how many months of statements you'll need, and which alternative documentation loans might work better for your situation.

Bank statements act as a financial diary. They tell lenders the story of your income, spending habits, and financial stability. When you apply for a home equity line of credit, lenders need to verify that you can afford the monthly payments, and your bank statements provide that proof.

For traditional HELOC borrowers with W-2 income, verification is straightforward: a few months of statements plus recent pay stubs paint a clear picture. But for self-employed borrowers, freelancers, or business owners, the picture gets more complex. Your income might fluctuate month to month. You might reinvest profits back into your business, making your taxable income look lower than your actual cash flow.

That's where bank statement HELOC programs come in. Instead of relying on tax returns (which often don't reflect true business income), lenders like Truss Financial Group review 12–24 months of business deposits to calculate your average monthly income. This approach gives self-employed borrowers a fair shot at qualification, without penalizing them for strategic tax planning.

The number of bank statements required for a HELOC depends entirely on your borrower profile. Here's a quick breakdown:

|

Borrower Type |

Typical Bank Statements |

Used For |

Example Program |

|

W-2 Employee |

2–3 months personal |

Verify consistent income |

Traditional HELOC |

|

Self-Employed |

12–24 months business |

Determine the average income |

Bank Statement HELOC |

|

Investor / LLC |

6–12 months business |

Rental or property income |

|

|

Retired (55+) |

None or limited asset proof |

Equity-based qualification |

Most bank statement HELOC lenders use 12 months of business statements to calculate income. If your income fluctuates seasonally, say you're a wedding photographer earning more in summer, lenders may review 24 months to establish a stable average. This protects both you and the lender by ensuring the loan is based on realistic, sustainable income.

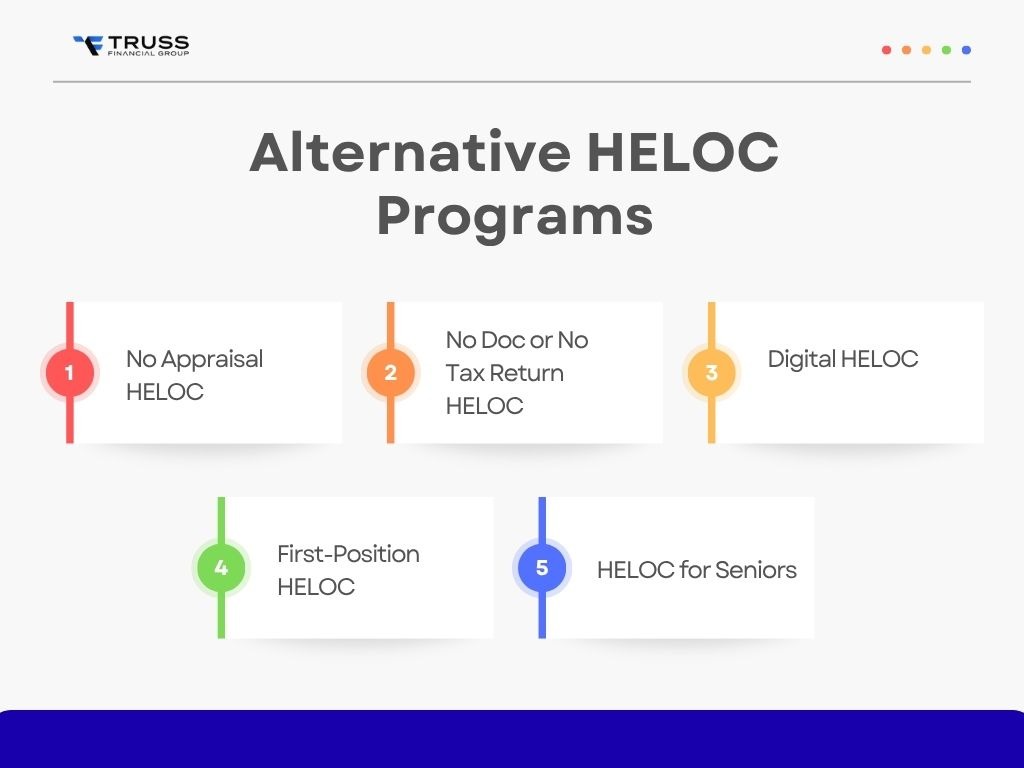

Today's HELOC programs go far beyond the traditional "show us your W-2 and tax returns" model. Let's explore the flexible home equity line options that match modern borrower needs.

Waiting weeks for an appraiser to visit your home? Not anymore. A no appraisal HELOC uses an automated valuation model (AVM), which is like a sophisticated algorithm that analyzes recent sales, property records, and market trends to estimate your home's value.

This approach is ideal for homeowners with:

By eliminating the traditional appraisal, you can cut 2–3 weeks off your closing timeline. No scheduling hassles, no waiting for reports, just faster access to your home's equity.

If you're self-employed, you know the frustration: your tax returns show minimal income because you've maximized deductions, but your bank account tells a different story. A no-doc or no-tax return HELOC solves this disconnect.

Here's how it works:

Loan-to-value ratios (LTV) typically cap around 75% for these programs, reflecting the alternative documentation approach. But for borrowers with strong cash flow and healthy bank balances, this trade-off is worth the simplicity.

Imagine applying for a HELOC entirely from your phone, no paper statements, no faxing documents, no visiting a branch. That's the promise of a digital HELOC.

Digital HELOC exemplifies this modern approach:

The digital process doesn't sacrifice accuracy; it enhances it. Real-time bank connections provide lenders with up-to-the-minute financial data, reducing fraud risk while accelerating approvals.

Most people think of HELOCs as second liens, lines of credit that sit behind your primary mortgage. But a first-position HELOC flips this model.

Instead of having a traditional mortgage plus a HELOC, your HELOC becomes your primary loan. This structure offers unique advantages:

First-position HELOCs work especially well for:

Retirement changes your financial picture. You might have significant home equity but limited monthly income. Traditional lenders see "no W-2" and immediately decline, but that's shortsighted.

Truss Equity Select, designed exclusively for homeowners 55 and older, takes a different approach:

It’s like a financial safety net that grows with your home's value. You maintain full ownership, control when and how you access funds, and preserve your estate for heirs.

When underwriters review your bank statements for a bank statement loan, they're looking for more than just big numbers. Here's what matters:

Bank statements tell part of your story, but lenders consider several factors when determining HELOC approval:

Smart preparation accelerates your HELOC approval and prevents last-minute scrambling. Follow these steps:

Yes. Programs like Truss Digital HELOC and Bank Statement HELOC use income deposits from bank statements instead of tax forms, making them ideal for self-employed borrowers with complex tax strategies.

Typically, 12–24 months for self-employed borrowers using a bank statement HELOC, or just 2–3 months for traditional W-2 employees. The exact requirement depends on your lender and income stability.

Not always. Some lenders offer no-appraisal HELOCs using automated valuation models (AVMs) that estimate your home's value through data analysis rather than physical inspections.

Truss HELOCs go up to $750,000, depending on your home's equity, credit score, and loan-to-value ratio. Some specialized programs for high-value properties may offer even higher limits.

Yes, The Truss Equity Select HELOC for homeowners 55+ offers equity-based qualification with flexible draws and non-recourse protection, minimizing traditional income documentation requirements.

Whether you're a self-employed borrower tired of being penalized for smart tax planning, a retiree sitting on substantial equity, or a traditional employee seeking the fastest path to approval, Truss Financial Group offers HELOC solutions designed for your specific situation.

From no-appraisal options that close in days to bank statement programs that honor your true earning power, our flexible home equity line products put you in control.

Connect with lending specialists who understand non-traditional income. Or explore conventional refinance options if a DSCR cash-out refinance better suits your goals.

Your home's equity is waiting. Get a quote today!

Take your pick of loans

Experience a clear, stress-free loan process with personalized service and expert guidance.

Get a quote.png?width=352&name=xxxxxx%20header%20(55).png)

11 min

19 min

-1.png?width=352&name=Blog%20covers%20(7)-1.png)

10 min

Discover your borrowing power and plan your mortgage journey with knowledge on your side.

Get a quoteGet a quote in 3 easy steps

Tell us what you want

Fill out our online form to help us understand your financial situation and loan needs.

We get to work for you

We review your info and look for competitive rates that match your specific goals.

You get a personalized quote

You’ll receive a customized rate quote that meets your unique profile.