19 min read

19 min read

A cash-out refinance is not limited to your primary residence. If you own a rental property with usable equity, a DSCR cash-out refinance may let you replace the current loan with a new investment-property mortgage and take cash out based largely on the property's rental income.

DSCR stands for debt service coverage ratio. In plain English, it compares the rental income a property can generate with the debt payment the property needs to support. That makes it especially important for real estate investors who may not want a loan decision based only on personal W-2 income or tax-return income.

Used carefully, a DSCR cash-out refinance can help investors access equity for renovations, reserves, debt consolidation, or another rental purchase. The right answer still depends on the property's cash flow, loan-to-value ratio, market rent, reserves, and the investor's broader plan. Truss Financial Group explains the underlying loan type in its guide to DSCR loans.

A DSCR cash-out refinance lets a real estate investor refinance a rental property, pay off the existing loan, and receive cash from available equity when the property's income can support the new mortgage payment.

A DSCR cash-out refinance is an investment-property refinance that focuses on the rental property's income instead of relying primarily on the borrower's personal income. The lender reviews whether the property's income can cover the proposed mortgage payment and related housing expenses.

This is why DSCR financing is popular with investors, self-employed borrowers, and portfolio owners. A borrower may have strong rental assets but a complicated tax profile. In that case, a debt service coverage ratio mortgage can be a more practical fit than a conventional income-documentation route.

The current rental-property loan is replaced by a new loan with new terms.

Part of the available equity is returned to the borrower after payoff and closing costs.

The lender checks whether rental income supports the new payment.

The DSCR is one of the main ways lenders assess risk. A higher DSCR means the property has more income cushion after the debt payment. A lower DSCR may mean the property is close to break-even or negative cash flow, which can affect approval, pricing, cash-out amount, or reserve requirements.

The basic DSCR formula is simple, but the inputs matter. Lenders may calculate income differently depending on whether they use lease income, market rent, short-term rental data, appraisal schedules, or operating history.

DSCR formula

DSCR = Net Operating Income / Total Debt Service

Net operating income usually starts with rental income and subtracts qualifying operating expenses. Total debt service generally includes the proposed principal, interest, taxes, insurance, and any applicable association dues.

For example, a DSCR of 1.00 means the property's income is roughly equal to the debt obligation. A DSCR above 1.00 means there is some income cushion. Many lenders prefer a DSCR around 1.20 to 1.25 or higher, but minimums vary by lender, loan size, property type, occupancy, credit profile, and LTV.

If you want to understand the income side more deeply, read Truss's guide to what NOI means in real estate. For conventional rental-income context, Fannie Mae also publishes guidance on rental income, although DSCR and Non-QM programs can use different rules.

A calculator can help you estimate whether the rental property has enough income cushion before you request terms. It will not replace underwriting, but it can help you spot whether the deal is likely to be tight.

The main appeal is flexibility. Instead of selling a property or using personal income documentation, investors may be able to unlock equity from a rental that already supports itself.

Cash-out refinancing can turn built-up equity from appreciation or principal paydown into usable capital.

Funds may be used toward another rental purchase, down payment, or investor reserve strategy.

Renovations can improve tenant appeal, reduce maintenance issues, or support stronger rent potential.

If the new terms are favorable, the refinance may help stabilize payments or free liquidity for reserves.

Some investors use cash-out funds to pay down higher-interest business or property-related debt.

DSCR loans typically focus on rental-property performance rather than traditional personal income verification.

Before using equity, compare the upside with the costs. Interest rate, prepayment penalty, closing costs, loan size, and the property's post-closing DSCR all matter. Truss covers more tradeoffs in its guide to DSCR loan pros and cons.

Requirements vary by lender and program. The ranges below are common starting points, not guarantees. A stronger property, borrower profile, or lower LTV can sometimes improve available terms.

| Requirement | What lenders may review | Why it matters |

|---|---|---|

| DSCR | Often around 1.20 to 1.25+, though some programs may differ. | Shows whether rental income can support the new payment. |

| Loan-to-value | Cash-out refinance LTV is commonly lower than purchase or rate-term limits. | More equity lowers lender risk and affects cash-out availability. |

| Credit profile | Credit score, mortgage history, and major derogatory events. | Credit can affect pricing, reserves, LTV, and approval conditions. |

| Reserves | Months of reserves for the subject property or portfolio. | Reserves help cover vacancy, repairs, or payment shocks. |

| Property type | Single-family rentals, 2-4 units, condos, townhomes, and sometimes short-term rentals. | Eligible property types and rent calculations vary by program. |

| Seasoning | How long you have owned the property or held the current loan. | Some lenders require ownership seasoning before cash-out. |

DSCR refinance programs commonly consider single-family rentals, 2-4 unit residential properties, condos, townhomes, and certain short-term rental properties. Larger multifamily, mixed-use, or commercial properties may require a different loan structure.

If the property is already financed, Truss's guide to refinancing a rental property can help you compare whether a DSCR option, conventional refinance, or another investor loan path makes more sense.

The right lender should understand investor files, rental-income analysis, entity vesting, property type, reserves, and DSCR calculations. Small differences in requirements can change how much cash is available and whether the deal still cash flows after closing.

This phrase can be confusing because a DSCR loan and a cash-out refinance are not opposites. A DSCR loan describes the way the rental property is underwritten. A cash-out refinance describes the transaction: replacing an existing loan with a larger one and taking cash from available equity.

A DSCR cash-out refinance combines both ideas. The property is evaluated through DSCR, and the refinance is structured to return cash to the investor after the existing debt and closing costs are handled.

If you are comparing DSCR with conventional financing, read Truss's breakdown of DSCR loans vs. conventional loans. Conventional financing may offer different pricing, but it usually requires a more traditional personal-income review.

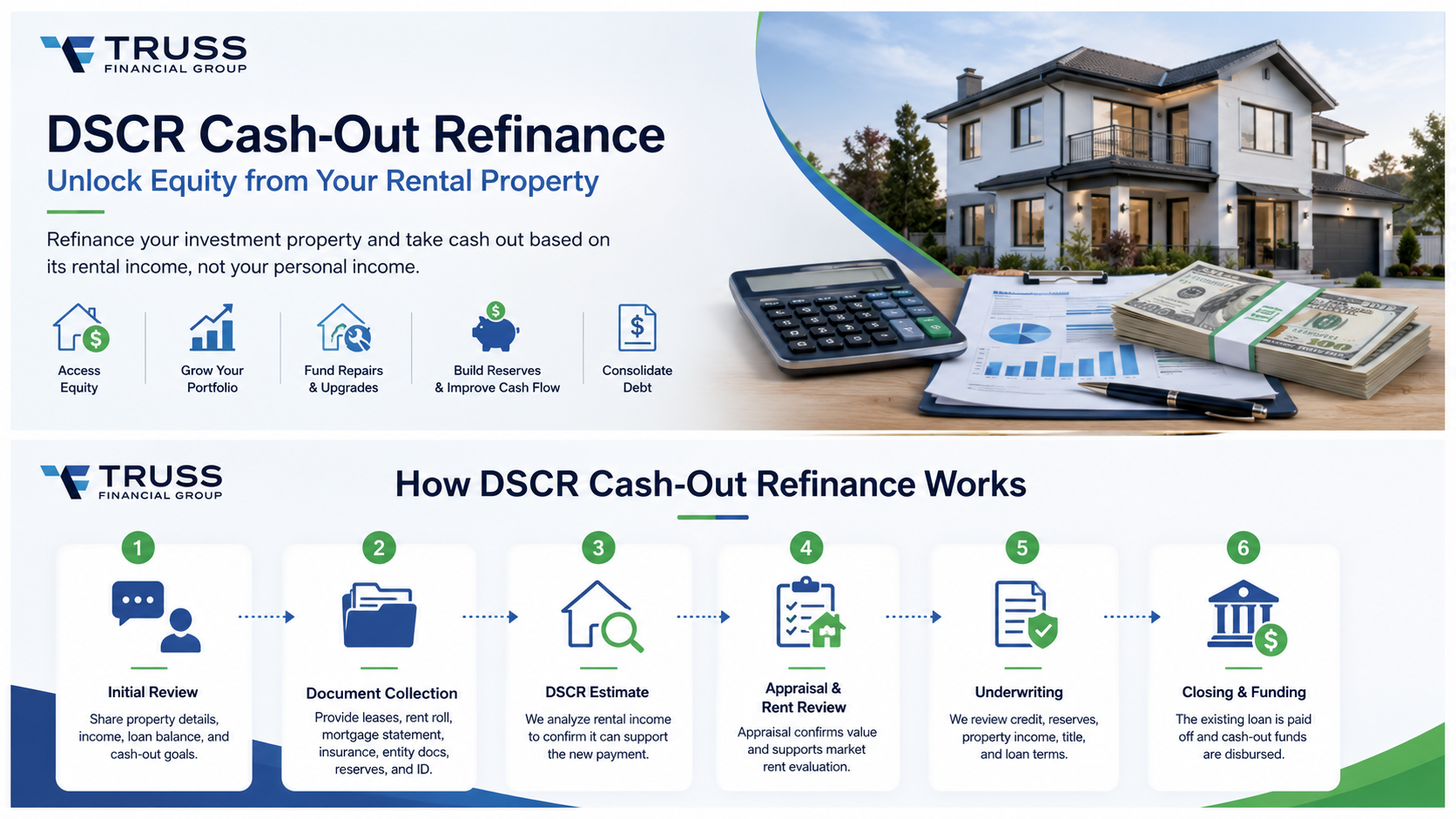

The process usually takes a few weeks, depending on the lender, appraisal timing, title, documentation, and the complexity of the property. The steps below show what investors typically prepare for.

Share the property address, estimated value, rental income, current loan balance, and target cash-out amount.

Gather lease agreements, rent roll, mortgage statement, insurance, entity documents, reserves, and identification.

The lender estimates whether the rental income can support the proposed new payment.

An appraisal helps confirm property value and may include market-rent support.

The lender reviews credit, reserves, title, property income, loan terms, and program guidelines.

After final approval, the old loan is paid off and eligible cash-out funds are disbursed.

Keep rental income records organized. For federal tax reporting context, the IRS provides information about Schedule E for supplemental income and loss, and Publication 527 covers residential rental property income and expenses. These pages are not a substitute for loan underwriting rules, but they are useful references for how rental activity is commonly documented.

Cash-out funds should have a clear purpose. Pulling equity without a plan can weaken cash flow and increase leverage. Investors commonly use funds for:

For a more complete investor financing view, compare this strategy with Truss's guide to DSCR loan types for investors.

A DSCR cash-out refinance can be useful, but it is still debt secured by an investment property. The goal is not simply to maximize cash out. The goal is to keep the property and portfolio resilient after the new loan closes.

This is where a simple investor rule helps: if the new debt weakens your DSCR too much, the cash-out amount may not be worth it. The property should still make sense after the refinance, not only on the day the funds arrive.

DSCR cash-out is not the only way to raise capital against a rental property. The better fit depends on your timeline, documentation, property type, credit profile, and tolerance for cost.

May fit if personal income and tax returns support conventional underwriting.

May move faster, but often comes with higher costs and shorter terms.

May provide flexible access to equity when available for the property type and borrower profile.

If speed and flexibility are more important than long-term loan cost, compare DSCR loans vs. hard money loans before choosing a path.

A DSCR cash-out refinance replaces an existing rental-property loan with a new loan and lets the investor access available equity when the property's rental income can support the proposed debt payment.

Many lenders prefer a DSCR around 1.20 to 1.25 or higher, but requirements vary by lender, property type, credit profile, reserves, and loan-to-value ratio.

A stronger DSCR can support better terms or more cash-out flexibility, while a lower DSCR may limit loan size, increase required reserves, or make approval harder.

DSCR loans typically focus on the rental property's income rather than traditional personal income verification, though lenders still review credit, assets, reserves, property details, and other risk factors.

Investors commonly use funds for another property purchase, renovations, reserves, debt consolidation, or portfolio liquidity, depending on lender rules and their investment plan.

Alternatives may include a traditional rental-property refinance, hard money loan, private money loan, investor HELOC, or waiting until the property has stronger equity or cash flow.

Investor financing review

A DSCR cash-out refinance can be powerful when the rental income, equity, reserves, and investment purpose all line up. Truss Financial Group can help investors compare DSCR refinance options, estimate the property's coverage ratio, and review whether cash-out proceeds make sense for the next step in the portfolio.

Check DSCR

Estimate whether the property supports the new payment.

Compare proceeds

Review LTV, costs, reserves, and cash-out availability.

Plan the use

Match the refinance to a clear investment goal.

Take your pick of loans

Experience a clear, stress-free loan process with personalized service and expert guidance.

Get a quote

21 min

19 min

13 min

Discover your borrowing power and plan your mortgage journey with knowledge on your side.

Get a quoteGet a quote in 3 easy steps

Tell us what you want

Fill out our online form to help us understand your financial situation and loan needs.

We get to work for you

We review your info and look for competitive rates that match your specific goals.

You get a personalized quote

You’ll receive a customized rate quote that meets your unique profile.