19 min read

19 min read

A DSCR loan without a down payment sounds like a golden ticket for real estate investors. Buy the property, let the rent support the mortgage, and keep your cash free for renovations, reserves, or the next deal.

That is the dream version. The real version needs more care.

Most legitimate DSCR purchase loans still require a down payment. The better opportunity is not finding a true 0% down DSCR loan. It is structuring the deal so you use the least amount of out-of-pocket cash while keeping the loan file clean, disclosed, and financeable.

Truss Financial Group works with investors who want that practical answer. If a standard bank says no because your tax returns, DTI, property count, or LLC structure does not fit, a DSCR loan may still work. But it has to be built around real numbers, real equity, and real rental cash flow.

A DSCR loan is a mortgage for income-producing real estate where the property's rental income helps qualify the loan. DSCR stands for debt service coverage ratio.

The basic formula is simple:

If a property brings in $3,000 in qualifying rent and the monthly payment is $2,500, the DSCR is 1.20. That means the rent covers 120% of the payment.

For investors, the biggest appeal is that a DSCR loan may not require traditional income verification. Instead of focusing on pay stubs, W-2s, personal tax returns, or standard DTI, the lender focuses on the property's ability to carry the debt.

Many investors use these phrases like they mean the same thing. They do not. This distinction matters whether you are buying your first rental, comparing DSCR loans vs conventional loans, or trying to preserve cash for the next property.

| Term | What it really means | How realistic it is |

|---|---|---|

| No down payment DSCR loan | The lender finances 100% of the purchase price | Rare and usually not realistic for a legitimate DSCR purchase loan |

| Low down payment DSCR loan | The investor brings less than the standard 20% to 25% | Possible for select strong files |

| Low out-of-pocket cash | The investor uses another legal capital source | More realistic when structured correctly |

| Seller credits | Seller helps with closing costs, not usually the down payment | Useful, but lender limits apply |

The safest goal is not 0% down. The safest goal is approved leverage. Every dollar should be documented, every lien should be disclosed, and the lender should understand the full capital stack before closing.

A DSCR loan may feel easier than a conventional investment property loan because personal income documentation is lighter. But easier documentation does not mean no borrower equity.

The Office of the Comptroller of the Currency describes DSCR as a measure that compares net operating income with debt service in commercial real estate credit analysis. The official OCC Commercial Real Estate Lending handbook explains the risk logic behind coverage ratios.

| 1. It lowers loan-to-value

A 75% LTV loan means the lender is financing 75% and the borrower has 25% equity. |

2. It improves DSCR math

A larger down payment usually means a smaller loan amount and a lower monthly payment. |

| 3. It shows borrower commitment

Meaningful equity tells the lender the investor has real cash at risk. |

4. It creates room for problems

Vacancy, repairs, taxes, insurance, and rent softness are easier to absorb with more equity. |

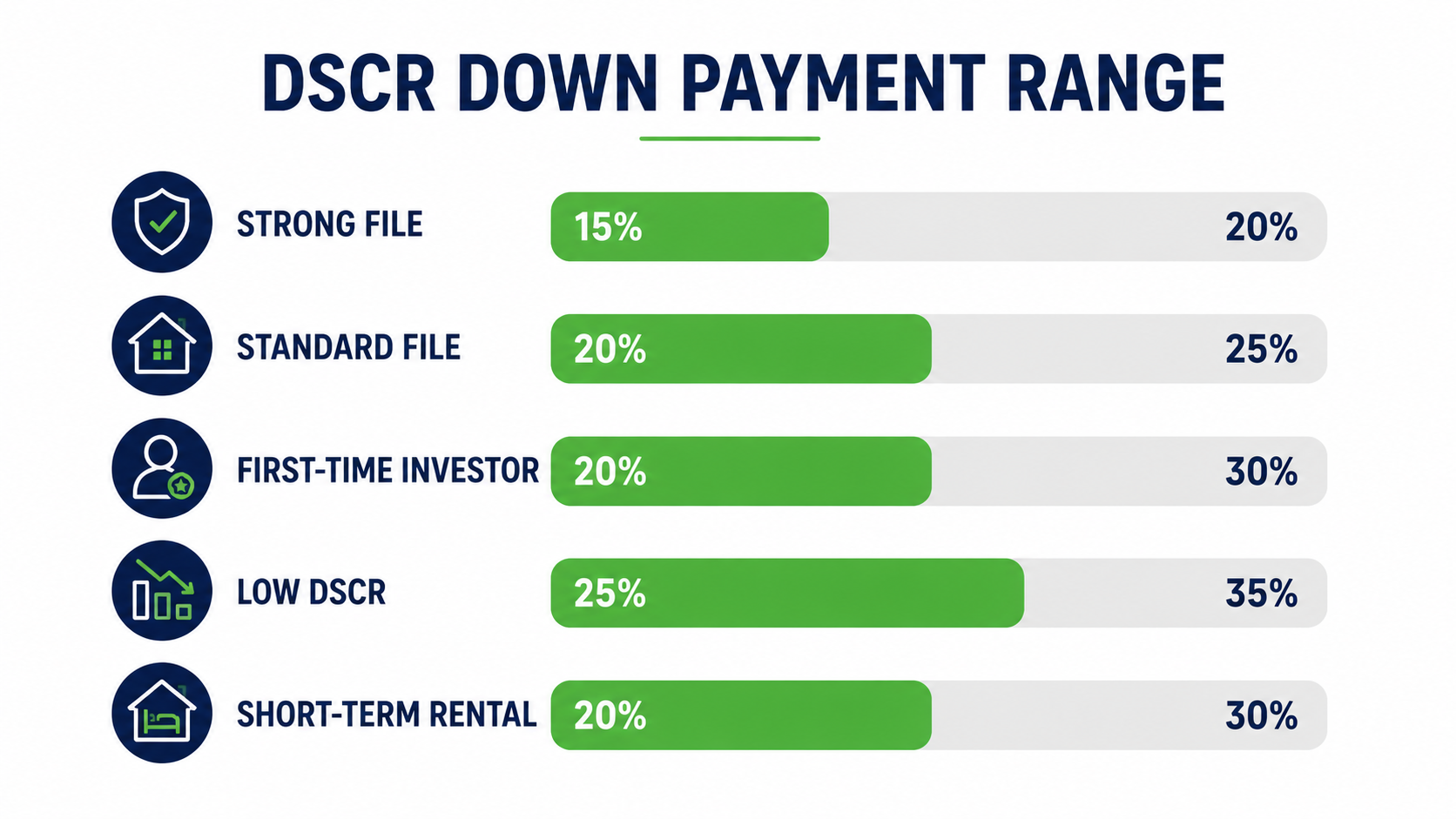

Most DSCR purchase loans in 2026 require 20% to 25% down. Some strong files may qualify around 15% to 20% down, while more complex or higher-risk files may need 25% to 35% down. Investors comparing program types can also review Truss's guide to DSCR loan types for investors.

| Investor profile | Typical down payment range | Why it changes |

|---|---|---|

| Strong file | 15% to 20% | Higher credit score, strong DSCR, simple property, solid reserves |

| Standard file | 20% to 25% | Common range for many rental property purchases |

| First-time investor | 20% to 30% | Less rental ownership history may require more equity |

| DSCR below 1.0 | 25% to 35% | Rent does not fully cover the proposed payment |

| Short-term rental | 20% to 30% | Income can be more volatile and documentation can vary |

Conventional investment property guidelines are not the same as DSCR guidelines, but they show the broader lending principle: investment properties usually receive lower LTV treatment than primary residences. Fannie Mae's current Eligibility Matrix shows how occupancy, property type, and transaction type affect LTV limits in conventional lending.

The down payment is not the full cash picture. Many investors hear "25% down" and only calculate 25% of the purchase price. That misses closing costs, prepaids, reserves, and entity-related costs.

Cash to Close Planning Formula

Cash to Close = Down Payment + Closing Costs + Prepaids

| Item | Example amount |

|---|---|

| Purchase price | $400,000 |

| Down payment at 25% | $100,000 |

| Estimated closing costs at 3% | $12,000 |

| Insurance and tax prepaids | $4,000 |

| 6 months reserves at $2,500 | $15,000 |

| Total funds to document | $131,000 |

The full $131,000 may not all be paid at closing. Reserves are usually documented as remaining assets. But the lender may still need to verify that the money exists.

Before making an offer, run the rent, payment, taxes, insurance, and loan amount through the Truss DSCR calculator. That gives you a cleaner starting point before you commit earnest money. If you are comparing the deal's return beyond the loan payment, the Truss guide on cap rate on rental property can help you sanity-check the investment.

A 10% down DSCR loan is uncommon. If you see one advertised, slow down and ask what the program actually is.

It may be a bridge loan, hard money loan, private-money structure, seller-financing arrangement, or marketing language for a product that is not truly a standard DSCR purchase loan. If you are comparing higher-cost short-term options, read Truss's breakdown of DSCR loans vs hard money loans.

A 15% down DSCR loan may be possible in select cases, but it is not the default planning number. The file usually needs strong credit, strong rental coverage, a simple property type, clean reserves, and sometimes investor experience.

The lowest down payment is not always the best deal. A lower down payment may come with higher rates, more points, more reserves, tighter property rules, or a prepayment penalty. Truss can compare 15%, 20%, and 25% down scenarios so you can see the real cost instead of chasing the smallest upfront number.

When a DSCR lender considers a lower down payment, the file usually needs compensating strengths. The investor is asking for higher leverage, so the lender looks for other ways to reduce risk.

| 1. Credit score

Higher credit can improve leverage and pricing, especially with clean housing history. |

2. Rental income support

The lender needs confidence that lease, market rent, or short-term rental income is realistic. |

| 3. Property type and condition

A clean 1-unit rental is usually easier than a complex, rural, mixed-use, short-term rental. |

4. Reserves after closing

Lenders may want 3 to 12 months of PITIA available after closing, depending on the file. |

Source of funds also matters. Bank statements, brokerage statements, equity proceeds, partner contributions, and approved credits should be clear before underwriting. Unexplained large deposits can slow a file down even when the property itself is strong. For a related document checklist, see Truss's guide on how to prepare a proof of funds letter for a mortgage.

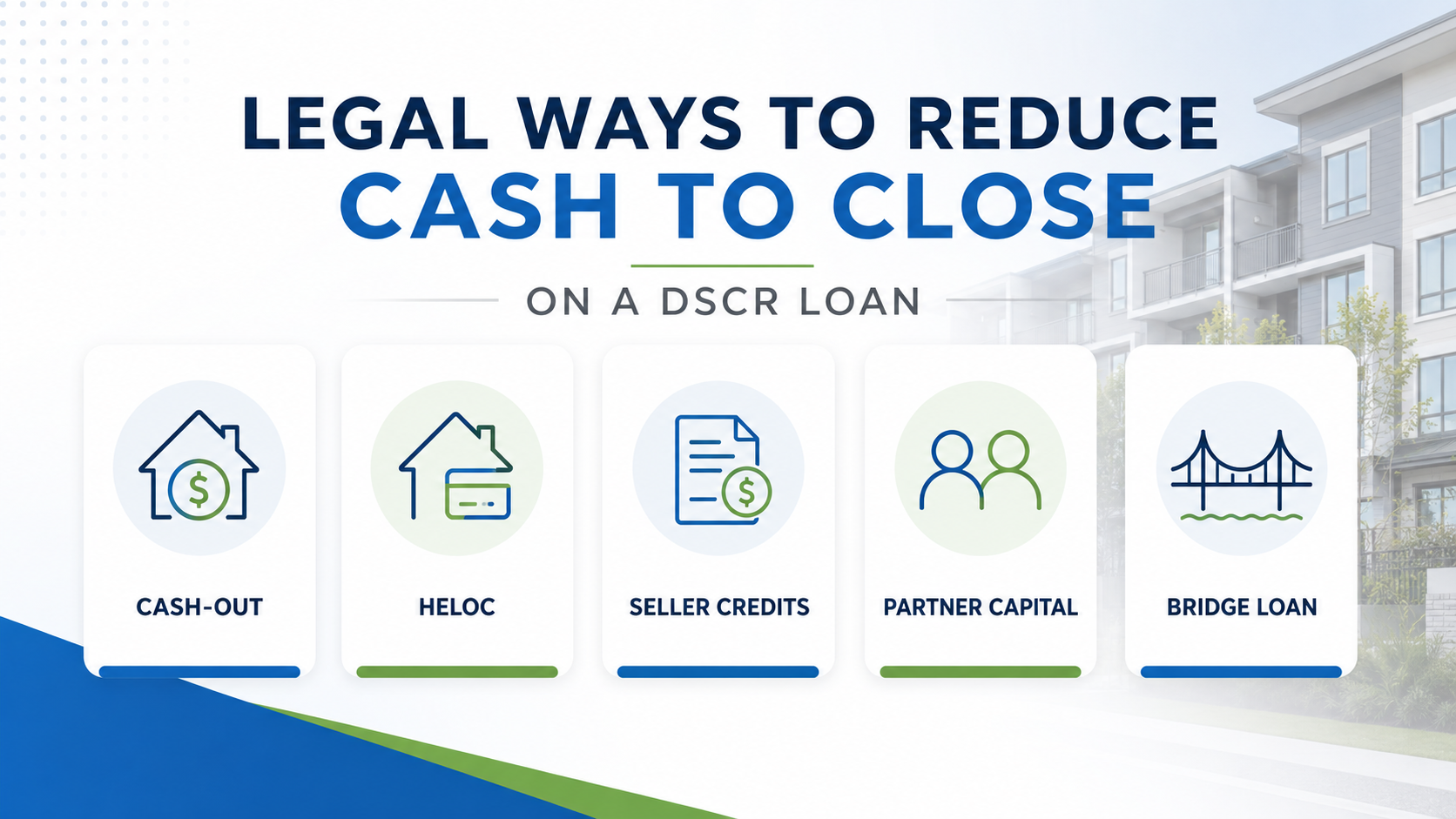

The realistic goal is not a fake 0% down DSCR loan. The realistic goal is a legal, documented structure that reduces how much new cash you bring to the closing table.

If you already own a rental property with equity, a DSCR cash-out refinance may help you pull capital from that property and use it toward the next purchase.

If you have equity in an investment property, an investor HELOC may help you access capital without refinancing the first mortgage. Truss offers a DSCR HELOC for real estate investors, which may help qualified borrowers use rental property performance rather than personal tax returns as the center of the file.

Seller credits usually cannot replace the required down payment. They may reduce closing costs if the DSCR lender allows them. The credit must be written into the contract, disclosed to the lender, and approved before closing.

Partner capital can help when the deal is strong but your available cash is limited. The lender may need to review ownership percentages, operating agreements, capital contributions, and signing authority.

If a property needs renovation, lease-up, or stabilization, a bridge loan or fix-and-flip loan may be a better first step. After repairs and rental stabilization, the investor may refinance into a DSCR loan.

A DSCR below 1.0 means the rental income does not fully cover the proposed payment.

| Monthly rent | Monthly PITIA | DSCR |

|---|---|---|

| $2,000 | $2,500 | 0.80 |

| $2,500 | $2,500 | 1.00 |

| $3,000 | $2,500 | 1.20 |

At 0.80, the property is short. At 1.00, rent matches the payment. At 1.20, the property has a 20% cushion.

Many lenders decline low-DSCR files or require a larger down payment. But a low DSCR does not always kill the deal. Truss can review options such as DSCR loans below 1.0, no-ratio loan structures, stronger reserves, asset depletion, or a different investor loan path. Short-term rental investors should also review how DSCR loans for Airbnb properties can be documented differently from long-term rentals.

| 1. Hidden seller financing

A seller second mortgage that is not disclosed to the first-lien lender can create serious underwriting and legal issues. |

2. Undisclosed credits after closing

Any side agreement where money changes hands after closing should be reviewed before the loan closes. |

| 3. Inflated purchase price

Raising the contract price to manufacture equity or create fake room for credits can create appraisal and fraud issues. |

4. Edited bank statements

Never change balances, remove pages, crop transactions, or edit financial records. Explain confusing documents instead. |

The FBI warns consumers about false statements and misrepresentation in mortgage transactions. Their public resource on mortgage fraud is worth reviewing before anyone suggests a side agreement, hidden lien, or altered document.

Truss Financial Group works with real estate investors who often do not fit a standard bank path. That includes self-employed investors, LLC borrowers, short-term rental operators, portfolio landlords, first-time investors, and high-equity borrowers with complicated tax returns.

Instead of chasing a risky 0% down claim, Truss looks at the actual deal. Does the rent support the payment? Is the lowest down payment actually the best deal? Can existing equity fund the next purchase? Does the property need a short-term loan first? Is another Non-QM option cleaner?

For investors comparing products, Truss also has deeper guides on DSCR loan interest rates, bank statement mortgages vs DSCR loans, and DSCR and Non-QM mortgage options when Fannie Mae does not fit.

Before applying for a DSCR loan, prepare the purchase price, target loan amount, estimated monthly rent, taxes, insurance, HOA dues, credit score estimate, proof of down payment funds, reserve funds, entity documents, and exit strategy.

A clean file closes faster. A vague file gets conditions.

In most cases, no. A legitimate DSCR purchase loan usually requires a down payment because the property is an investment asset and the lender needs an equity cushion.

The common DSCR loan down payment range in 2026 is 20% to 25% for many rental property purchases. Strong files may qualify with less, while low-DSCR or complex files may need more.

A 10% down DSCR loan is uncommon. If a program advertises 10% down, review the rate, points, reserve requirement, property limits, and whether a second lien is involved.

Some investors use home equity or rental property equity as a down payment source. The HELOC or equity loan must be documented and acceptable to the lender.

Investors may reduce out-of-pocket cash by using existing equity, a DSCR cash-out refinance, an investor HELOC, seller credits for closing costs, partner capital, bridge financing, or a fix-and-flip-to-DSCR strategy.

DSCR loans can be a strong option for investors who want faster underwriting and less personal income documentation. The tradeoff is simple: most DSCR purchase loans still need real borrower equity. Plan for 20% to 25% down, then work backward to reduce cash to close legally.

If you are offered a DSCR loan with no down payment, slow down and review the structure carefully. Hidden seller financing, edited bank statements, inflated purchase prices, or undisclosed credits can create serious underwriting and legal risk.

For a cleaner path, you can contact our experts at Truss Financial Group to compare DSCR, investor HELOC, bridge, fix-and-flip, no-ratio, and cash-out refinance options before the deal reaches underwriting. To learn more about DSCR loans, explore Truss's full debt service coverage ratio mortgage guide.

Take your pick of loans

Experience a clear, stress-free loan process with personalized service and expert guidance.

Get a quote

15 min

-3.jpg?width=352&name=Blog%20covers%20(5)-3.jpg)

9 min

.png?width=352&name=Blog%20Cover%20(1).png)

7 min

Discover your borrowing power and plan your mortgage journey with knowledge on your side.

Get a quoteGet a quote in 3 easy steps

Tell us what you want

Fill out our online form to help us understand your financial situation and loan needs.

We get to work for you

We review your info and look for competitive rates that match your specific goals.

You get a personalized quote

You’ll receive a customized rate quote that meets your unique profile.