4.6 from 700+ reviews

4.6 from 700+ reviews

4.6 from 700+ reviews

Key Features

![]() FHA loans in California offer low down payment options (as low as 3.5%) and flexible credit requirements, making them ideal for first-time homebuyers.

FHA loans in California offer low down payment options (as low as 3.5%) and flexible credit requirements, making them ideal for first-time homebuyers.

![]() The 2025 FHA loan limit in high-cost California counties like Los Angeles and San Francisco reaches up to $1,149,825 for single-family homes.

The 2025 FHA loan limit in high-cost California counties like Los Angeles and San Francisco reaches up to $1,149,825 for single-family homes.

![]() Buyers can apply for FHA loans in California online with minimal paperwork and faster pre-approvals through approved lenders.

Buyers can apply for FHA loans in California online with minimal paperwork and faster pre-approvals through approved lenders.

![]() FHA loans require mortgage insurance premiums (MIP), including a 1.75% upfront fee and a 0.55% annual fee paid monthly.

FHA loans require mortgage insurance premiums (MIP), including a 1.75% upfront fee and a 0.55% annual fee paid monthly.

![]() Unlike conventional loans, FHA loans in California are more accessible to buyers with credit scores as low as 580 and higher debt-to-income ratios.

Unlike conventional loans, FHA loans in California are more accessible to buyers with credit scores as low as 580 and higher debt-to-income ratios.

What Are FHA Loans?

FHA loans are government-backed mortgages insured by the Federal Housing Administration, a part of the U.S. Department of Housing and Urban Development (HUD). These loans are designed to help people, especially first-time homebuyers, qualify for a mortgage, even if they have lower credit scores or limited savings.

The FHA protects the lender by insuring the loan in case the borrower defaults. This insurance makes lenders more willing to offer loans with lower down payments and flexible credit requirements.

One of the main benefits of an FHA loan is that it allows buyers to put down as little as 3.5% of the home's purchase price. FHA loans also tend to have more lenient guidelines compared to conventional loans, which can be helpful for borrowers who might not qualify elsewhere.

This makes FHA loans especially helpful in competitive California markets where affordability is often a challenge.

Key Features of FHA Loans

- Low Down Payment: FHA loans require as little as 3.5% down, making it easier for buyers with limited savings to purchase a home.

- Flexible Credit Requirements: Borrowers with lower credit scores may still qualify. FHA loans are more forgiving of past credit issues than many conventional loans.

- Government Backing: The FHA insures the loan, not the lender. This government guarantee encourages lenders to approve buyers who might otherwise be denied.

- Fixed or Adjustable Rates: FHA loans are available with either fixed interest rates, which stay the same over time, or adjustable rates, which may change after a few years. This gives borrowers options to fit their financial needs.

FHA Loans in California Timeline

- Pre-approval: Start by getting pre-approved through Truss Financial Group to understand your budget and strengthen your offer.

- Home Search: Find a home in California that meets FHA guidelines, with help from a qualified real estate agent.

- Loan Application: Submit your official FHA loan application through Truss, including all required financial documents.

- Appraisal: An FHA-approved appraiser will assess the home’s value and safety standards.

- Underwriting: Our underwriting team reviews your application to ensure it meets FHA and California loan limits.

- Closing: Once approved, you’ll sign final documents, pay closing costs, and get the keys to your California home.

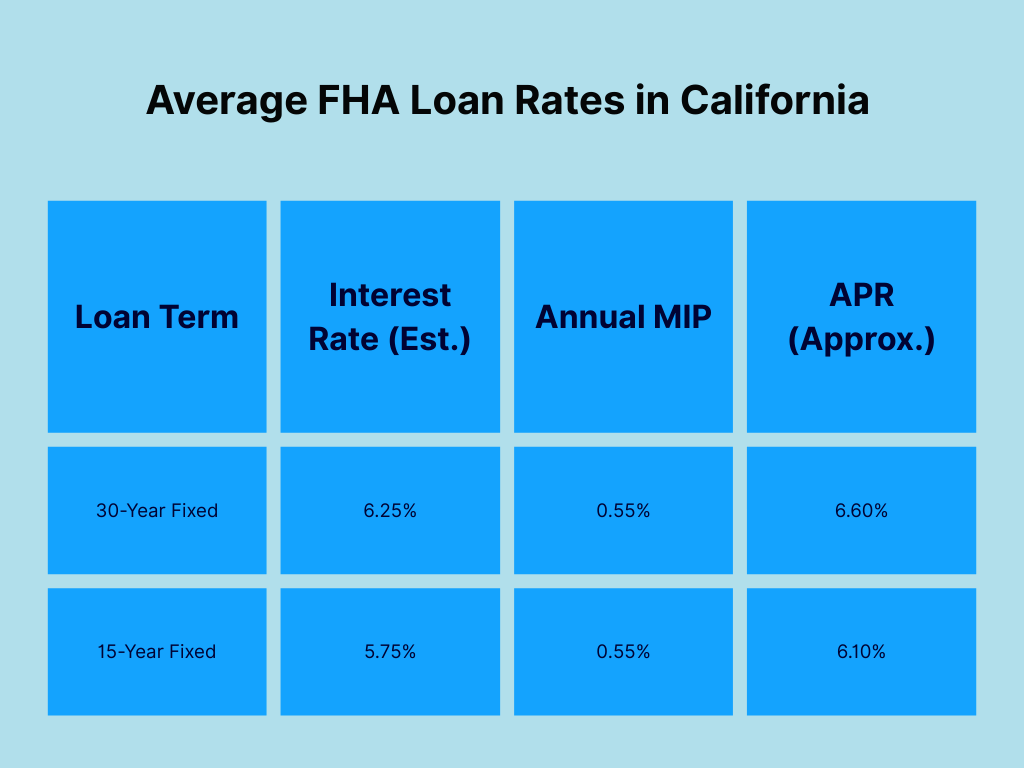

FHA Loan Interest Rates in California

How Rates Are Determined

FHA loan interest rates are influenced by several factors, including

- Current market rates (based on the 10-year Treasury yield)

- Your credit score (higher scores often get better rates)

- Loan amount and term (e.g., 15-year vs. 30-year)

- Down payment (larger down payments may reduce the rate)

- Debt-to-income ratio (DTI)

Lenders also factor in FHA mortgage insurance premiums (MIP), which are required for all FHA loans and can affect the total cost of the loan.

Average FHA Loans in California Rates

Rates can change daily, but here’s a general snapshot for early 2025:

Rates are estimates and vary by lender, borrower profile, and location. Truss Financial Group offers competitive FHA rates tailored to California borrowers.

Tips to Get the Best FHA Rate in California

- Improve Your Credit Score: Even a small jump in your score can lower your rate.

- Shop Around: Compare offers from multiple lenders, including Truss Financial Group, to find the most favorable terms.

- Lower Your DTI Ratio: Pay down debt to improve your financial profile.

- Lock in Your Rate: Once you find a good rate, ask your lender to lock it in to avoid market changes.

How Do FHA Loans Work in California?

FHA loans work the same way nationwide, but in California’s unique housing market, there are some important differences, especially in high-cost areas like Los Angeles, San Diego, San Francisco, and Orange County.

Because home prices are generally higher in California, the FHA sets higher loan limits in certain counties. For 2025, the standard FHA loan limit in most U.S. counties is $498,257. but in many parts of California, the limit can go up to $1,149,825 for a single-family home. This allows more buyers to qualify for FHA financing even in areas where home prices far exceed the national average.

FHA loans in California still require a minimum 3.5% down payment and are available to borrowers with credit scores as low as 580 (or even 500 with a larger down payment). The loan must be used for a primary residence, and the property must meet FHA safety and livability standards.

For many Californians, especially first-time buyers and those shut out of the conventional loan market, FHA loans offer a realistic path to homeownership particularly when paired with expert guidance from Truss Financial Group, a trusted local lender who understands California’s complex housing landscape.

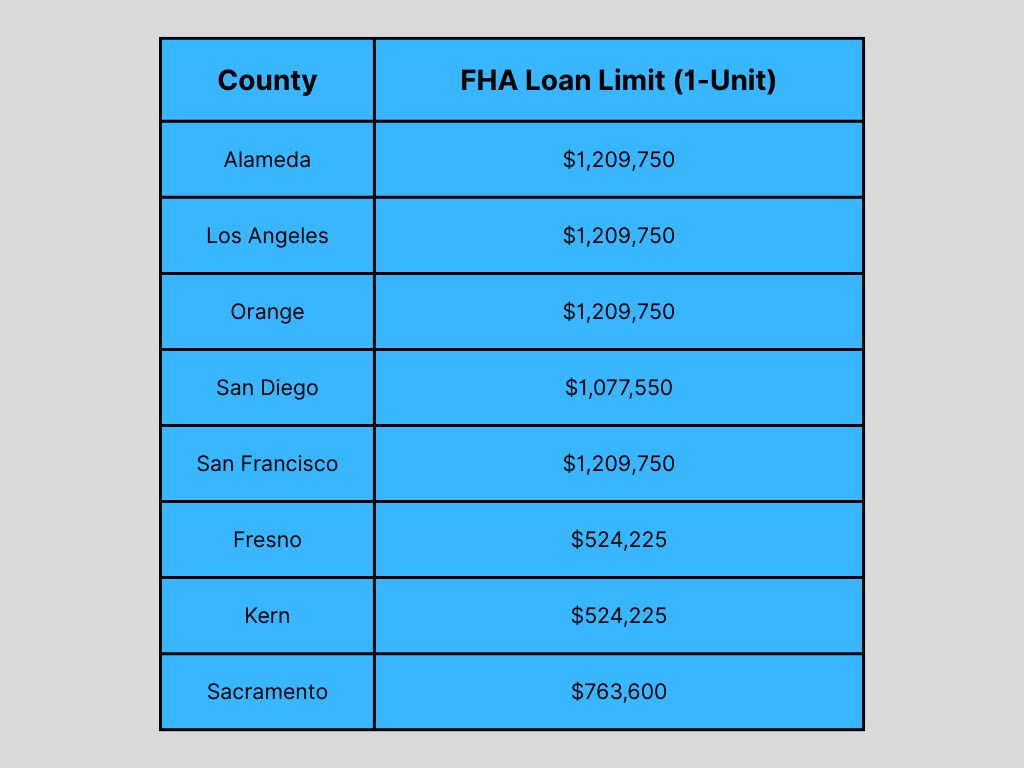

FHA Loans in California Limits

In California's diverse housing market, FHA loan limits are adjusted annually to reflect regional home prices. For 2025, these limits range from $524,225 in lower-cost areas to $1,209,750 in high-cost regions like Los Angeles, San Francisco, and San Diego

Below is a selection of counties with their respective limits for single-family homes:

2025 FHA Loan Limits by County (Single-Family Homes)

Note: Limits for multi-unit properties are higher. For a comprehensive list of all counties and property types, please refer to the official FHA loan limits page.

FHA Loan Requirements in California

Securing an FHA loan in California involves meeting specific criteria related to credit, income, and property standards. Here's what you need to know:

Minimum Credit Score

- 580 or higher: Eligible for a 3.5% down payment.

- 500–579: Requires a 10% down payment.

- Below 500: Generally ineligible for FHA loans.

Note: Some programs, like CalHFA FHA loans, may require higher credit scores, typically around 640 or more

Debt-to-Income (DTI) Ratio

- Ideal: 50% or lower.

- Exceptions: Some lenders may approve higher ratios with compensating factors, such as a larger down payment or significant savings .

Employment and Income

- Stable Employment: At least two years in the same job or profession.

- Income Verification: Provide W-2s, tax returns, and recent pay stubs.

- Non-Occupant Co-Borrowers: Not allowed in most cases for FHA loans in California

Property Requirements

- Primary Residence: The home must be your primary dwelling.

- FHA Appraisal: The property must meet FHA's safety and livability standards.

- Occupancy: You must occupy the home within 60 days of closing.

- Property Type: Eligible properties include single-family homes and FHA-approved condos.

Apply for an FHA Mortgage Loan Online

Applying for an FHA loan in California has become more streamlined with digital platforms. Here's a step-by-step guide:

- Choose an FHA-Approved Lender: Select a lender approved by the Department of Housing and Urban Development (HUD) to participate in the FHA program.

- Complete the Online Application: Fill out the application form provided by your chosen lender.

- Submit Required Documents: Upload necessary documents, including:

- Proof of identity (e.g., driver's license or passport)

- Social Security number

- Recent pay stubs and W-2 forms

- Tax returns for the past two years

- Bank statements for the last two months

- Proof of identity (e.g., driver's license or passport)

- Review Loan Estimates: Once your application is processed, review the loan estimates provided by the lender.

- Schedule an Appraisal: The lender will arrange for an FHA-approved appraiser to assess the property's value and condition.

- Underwriting and Approval: The lender's underwriting team will review your application and documents to ensure they meet FHA guidelines.

- Closing: Upon approval, you'll receive a closing disclosure outlining the terms of your loan, closing costs, and any other fees associated with your mortgage. Review this closing document carefully .

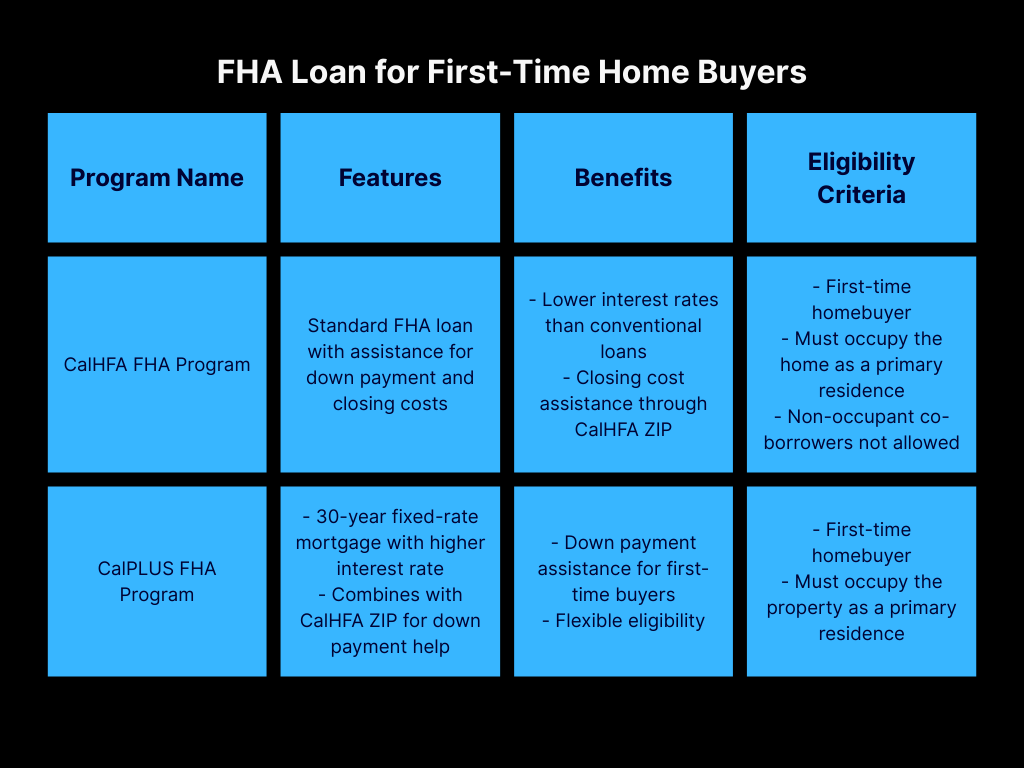

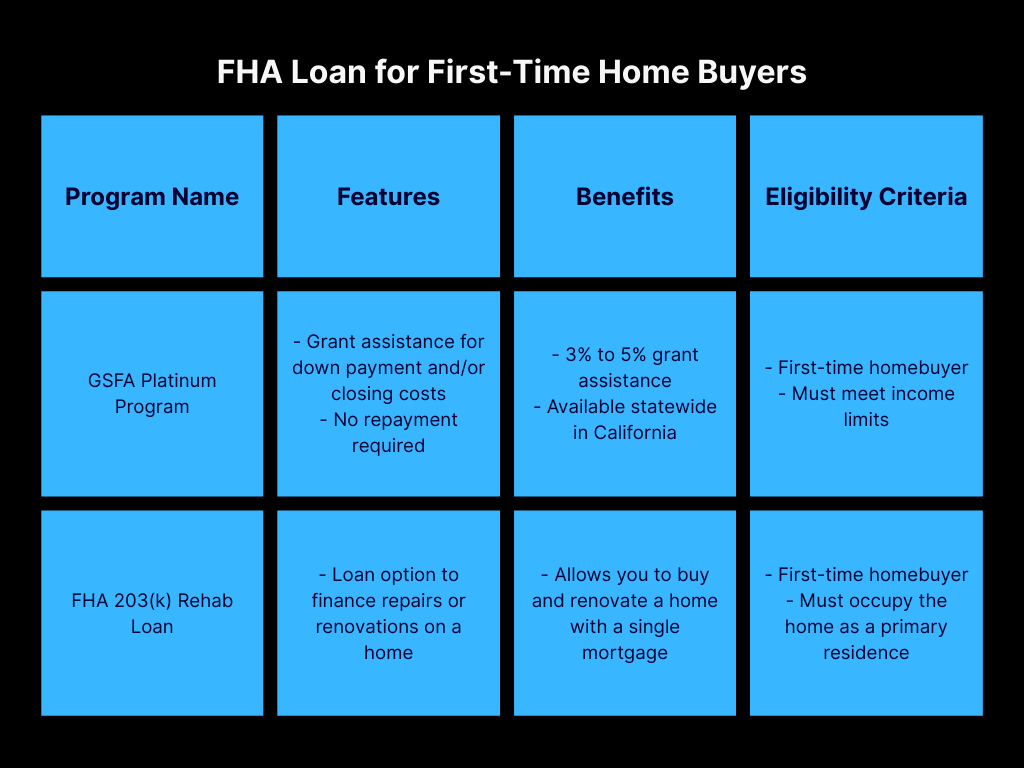

FHA Loan for First-Time Home Buyers

These programs offer unique advantages to first-time buyers in California, helping reduce upfront costs and make homeownership more affordable.

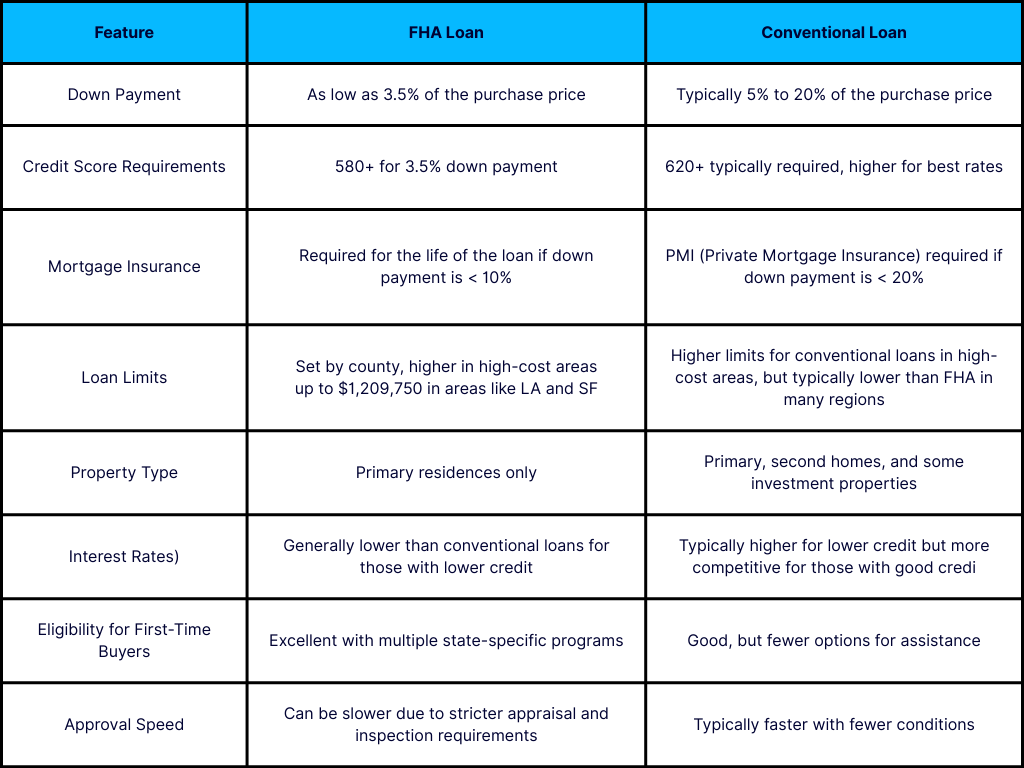

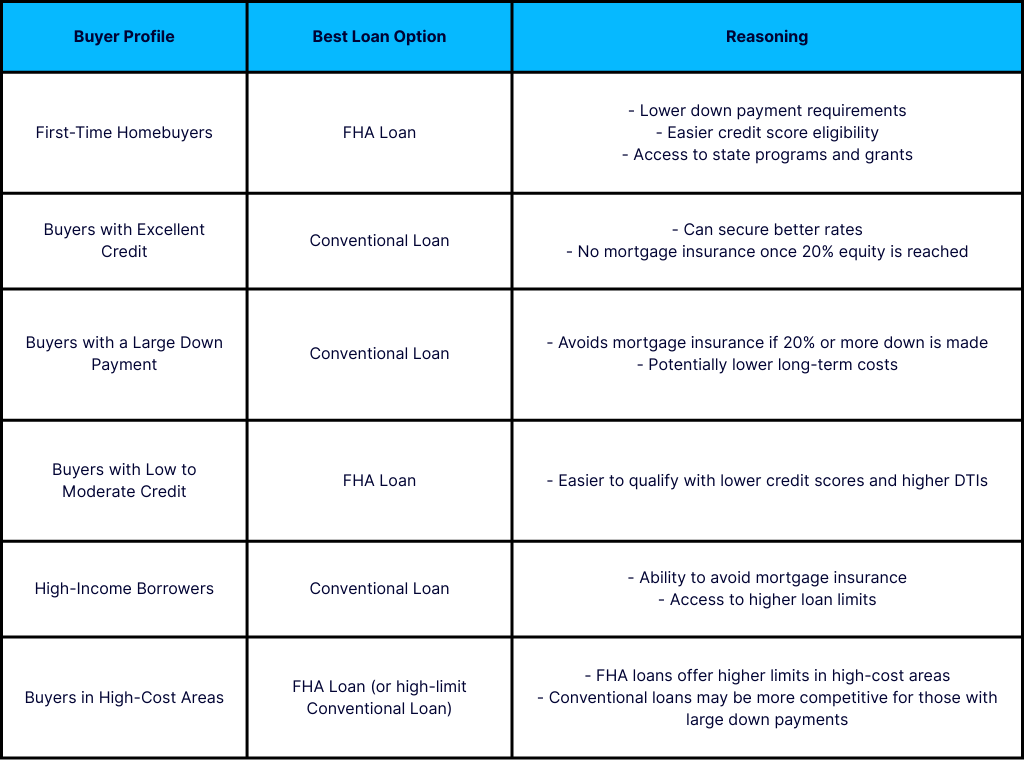

FHA Loans vs. Conventional Loans

FHA and conventional loans offer different advantages depending on a borrower’s financial situation and homeownership goals. Here's how they compare:

Pros and Cons of FHA Loan vs. Conventional Loan

- FHA loans are ideal for first-time buyers, those with lower credit scores, or buyers who can’t afford a large down payment.

- Conventional loans are generally better for buyers with excellent credit, larger down payments, and those who want to avoid mortgage insurance over time.

If you’re uncertain about which option suits your financial situation, Truss Financial Group can help you assess your eligibility and find the best loan type.

FAQ

What is the 11-Year Rule for FHA Mortgage Insurance?

With an FHA loan, mortgage insurance (MIP) is typically required for the life of the loan if your down payment is less than 10%. However, if your down payment is 10% or more, you can cancel MIP after 11 years.

Can I Drop Mortgage Insurance Early?

- For FHA loans with a down payment of less than 10%, MIP will last for the entire loan term, and there is no option to remove it.

- For FHA loans with a down payment of 10% or more, you can drop MIP after 11 years.

Can I Refinance to Get Rid of FHA Mortgage Insurance?

Yes, if you want to avoid paying MIP for the life of your FHA loan, you can refinance into a conventional loan once you have 20% equity in your home. Refinancing might be a good option if your home's value has increased or if you've paid down a significant portion of your loan.

What is the upfront mortgage insurance premium (UFMIP) on FHA loans?

The upfront mortgage insurance premium (UFMIP) is a one-time fee that is typically 1.75% of the loan amount. For example, if you're buying a home with an FHA loan for $300,000, the UFMIP would be approximately $5,250. This fee can be rolled into your loan balance.

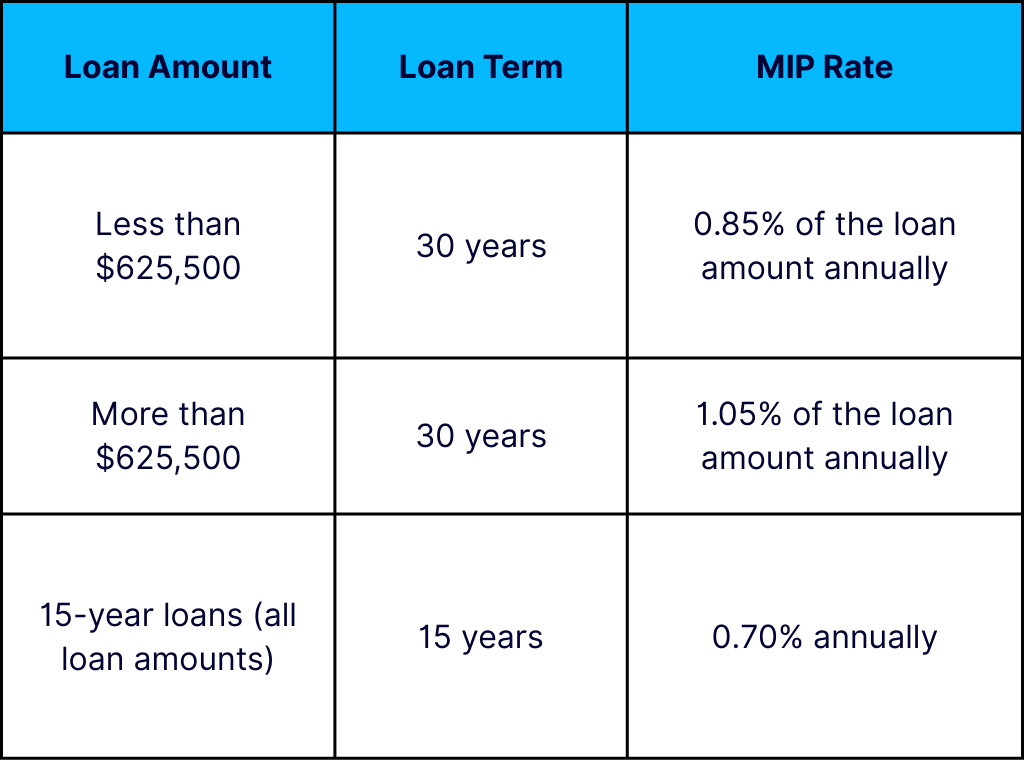

What Are the Monthly FHA Mortgage Insurance Premiums?

The monthly MIP depends on the size of your loan, the length of your loan, and the loan-to-value ratio (LTV). Here’s a general breakdown

Get the information you need to make confident decisions

Discover your borrowing power and plan your mortgage journey with knowledge on your side.

Get a quote- No documents required

- No commitment

- No commitment

Get a quote in 3 easy steps

Tell us what you want

Fill out our online form to help us understand your financial situation and loan needs.

We get to work for you

We review your info and look for competitive rates that match your specific goals.

You get a personalized quote

You’ll receive a customized rate quote that meets your unique profile.