11 min read

11 min read

Investing in a short-term rental can be a great way to build wealth and generate a passive income. Financing one, however, isn’t always easy. Traditional mortgages often don’t work for Airbnb and vacation rentals, especially if you’re self-employed or don’t have a W-2 income. This doesn’t mean you’ve hit a wall though.

Many investors turn to short-term rental loans in such situations. This guide will show you how short-term rental loans work and how you can secure one for your rental property. ____________________________________________________________________________

![]() Short-term rental loans allow you to finance Airbnb properties based on rental income.

Short-term rental loans allow you to finance Airbnb properties based on rental income.

![]() DSCR loans do not require income verification, are faster to approve, and have a minimum DSCR of 1.25x.

DSCR loans do not require income verification, are faster to approve, and have a minimum DSCR of 1.25x.

![]() Lenders look for a credit score of 620+, 3–6 months of cash reserves, and properties in STR-friendly locations.

Lenders look for a credit score of 620+, 3–6 months of cash reserves, and properties in STR-friendly locations.

![]() Tax benefits include mortgage interest deductions, depreciation, cost segregation studies, and 1031 exchanges to reduce taxable income.

Tax benefits include mortgage interest deductions, depreciation, cost segregation studies, and 1031 exchanges to reduce taxable income.

![]() Alternative financing options for investors who don’t qualify for DSCR loans include HELOCs, personal loans, and crowdfunding.

Alternative financing options for investors who don’t qualify for DSCR loans include HELOCs, personal loans, and crowdfunding.

____________________________________________________________________________

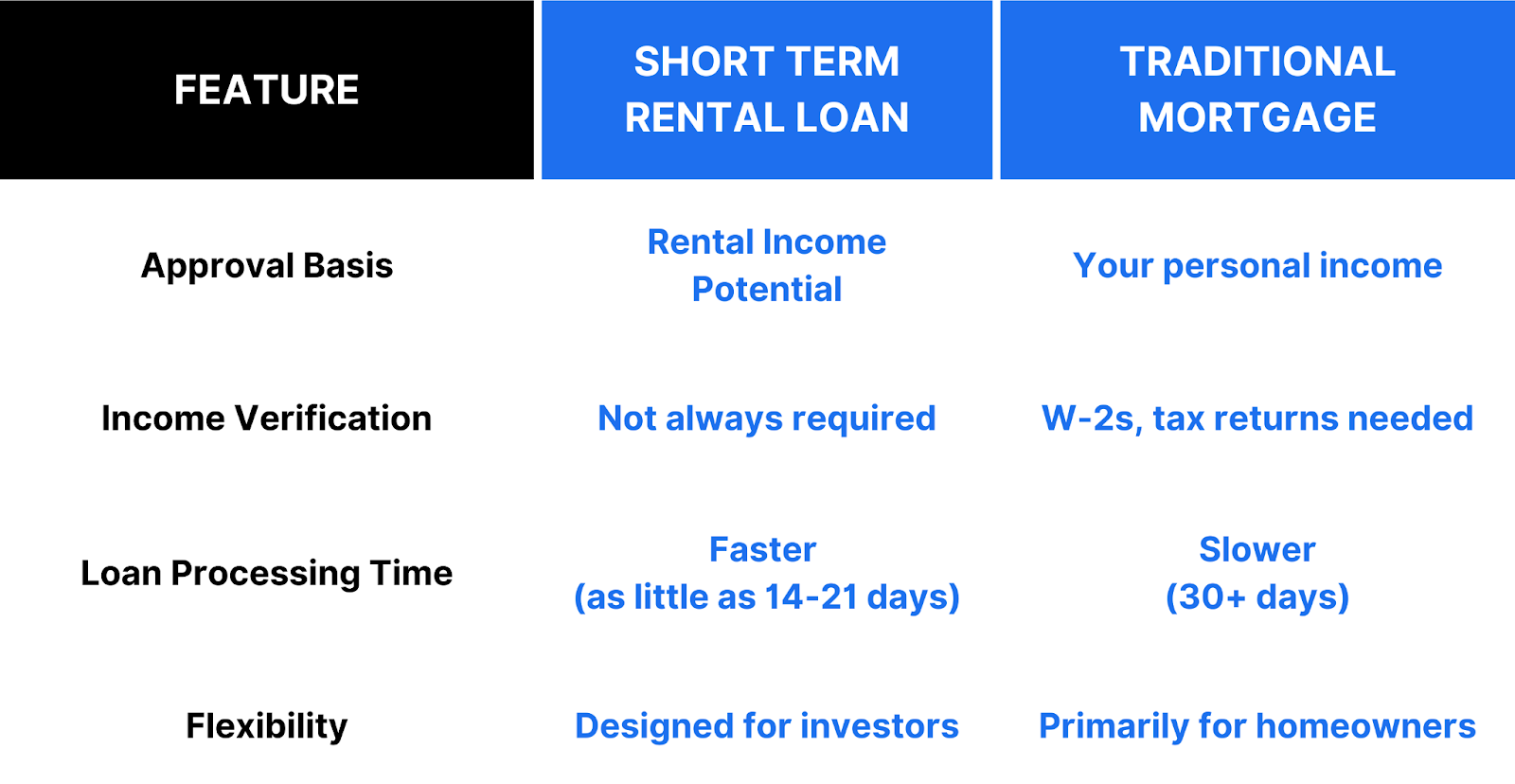

A short-term rental (STR) loan is designed specifically for properties rented out nightly or weekly. Unlike traditional mortgages, which rely heavily on personal income and employment history, STR loans focus on the property’s rental income potential to determine eligibility.

Below in the table, there's a side-by-side comparison between short-term rental loans and traditional mortgages.

When it comes to short-term rental financing, there’s no one solution.

Here are some of the most common types of loans with their key benefits and potential drawbacks:

|

Loan Type |

Best For |

Key Benefits |

Potential Drawbacks |

|

Investors qualifying based on rental income |

No personal income verification, faster approvals |

Requires strong rental income to qualify |

|

|

2. Portfolio Loans |

Investors with multiple properties |

Finance several properties under one loan |

Higher interest rates than DSCR loans |

|

Investors buying and renovating STRs |

Short-term financing for quick purchases and upgrades |

Higher interest rates, must refinance into a long-term loan |

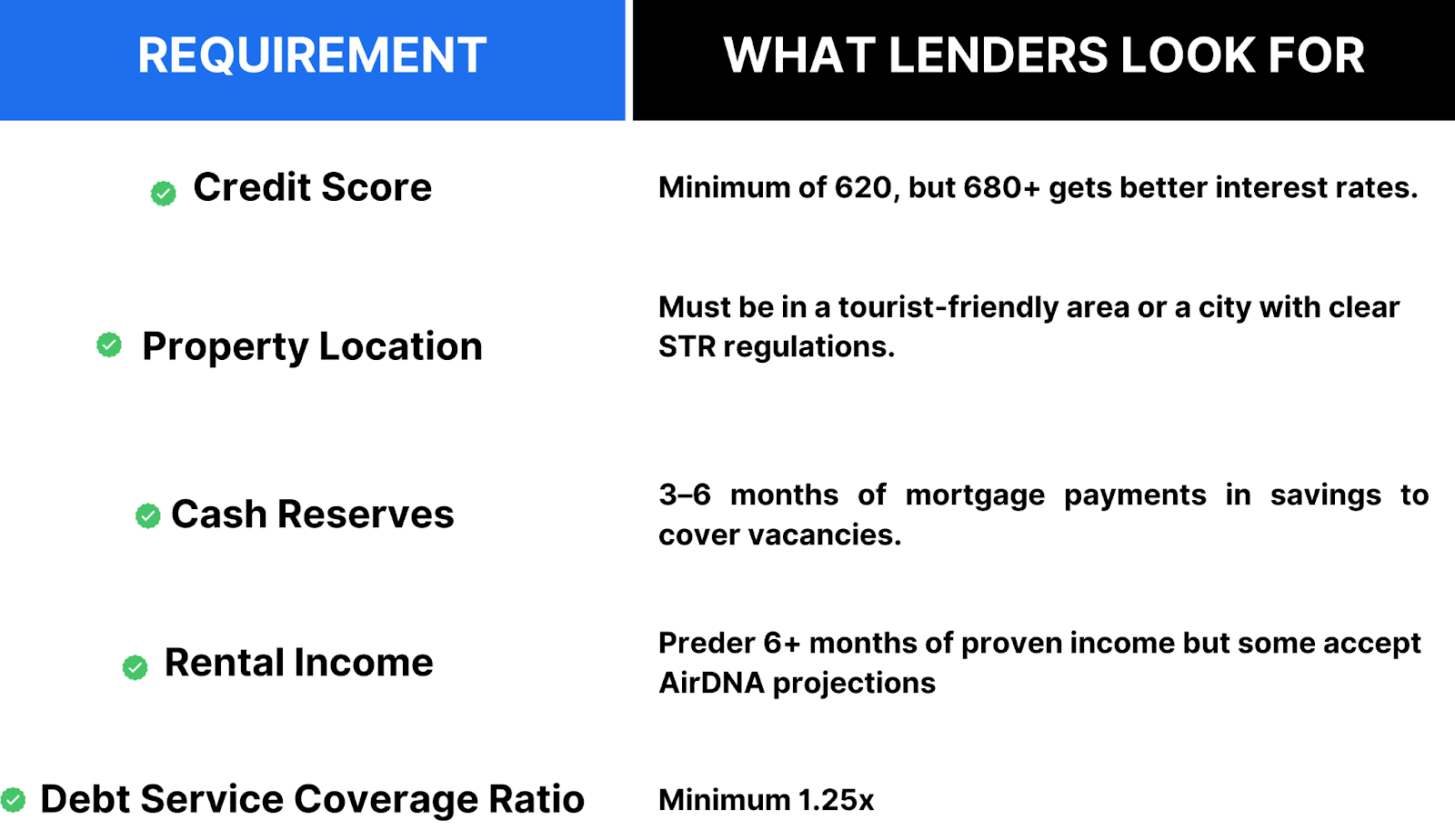

While STR loans offer considerable flexibility, lenders still require minimum requirements, such as:

Most investors overlook a key financing tactic: combining a DSCR loan with a Home Equity Loan of Credit (HELOC).

Here’s how you can use this approach:

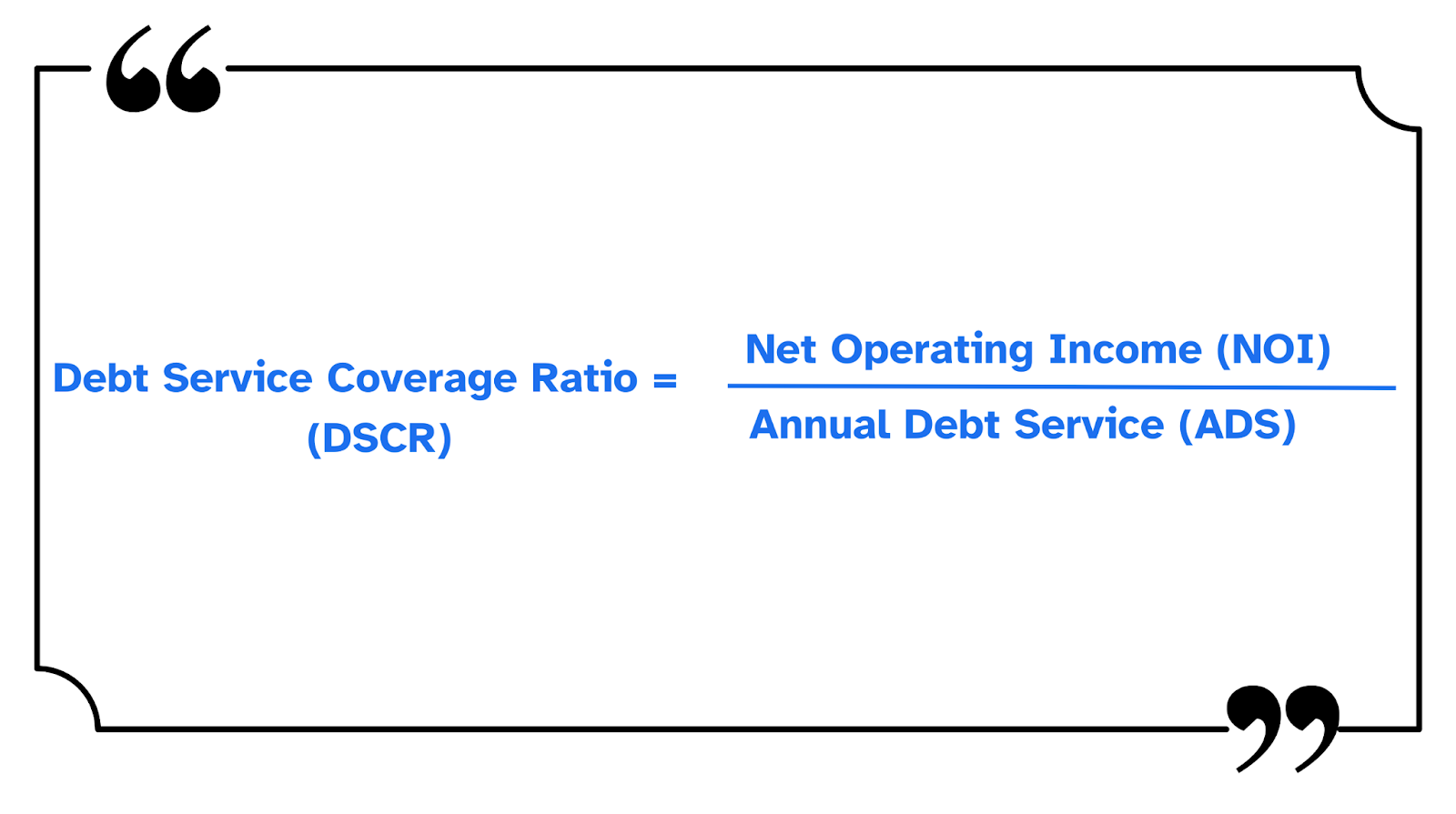

For many investors, DSCR loans are the most accessible way to finance short-term rentals.

Lenders use the DSCR to determine whether a property's rental income can cover its mortgage payments. The formula is simple:

You can also use an Airbnb ROI calculator to make an estimate.

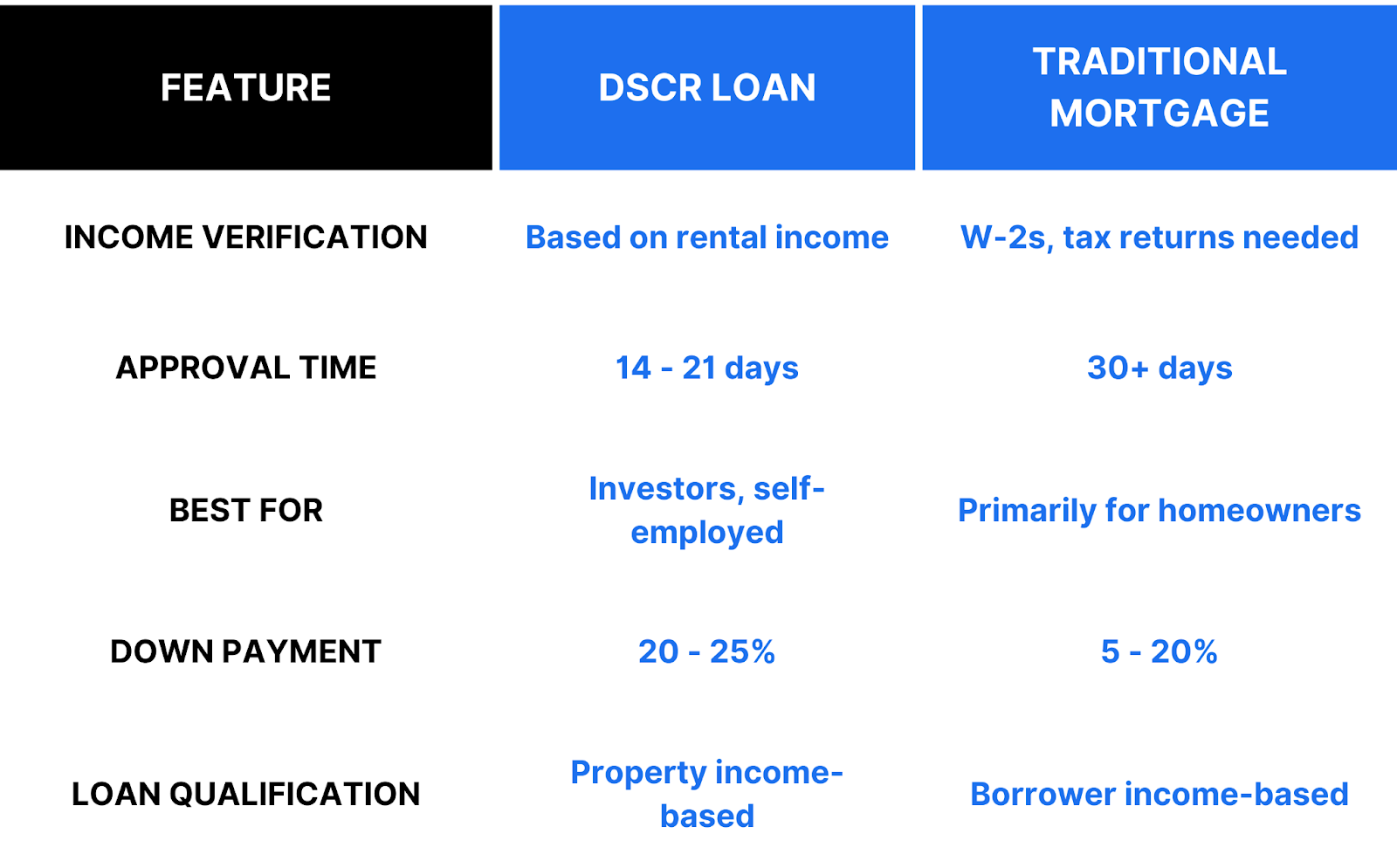

In below table, we have compared DSCR loans with traditional mortgages:

A DSCR loan is the best option if you’re looking to scale your short-term rental business without the hassle of income verification. You can learn more about how DSCR loans compare to other financing options here.

Getting approved for an STR loan is much easier than getting a traditional mortgage. However, lenders still require a few key requirements, have a look at the table below:

![]() Homeowners Association (HOA) & Local Restrictions: Many HOAs and cities have strict rules regarding short-term rentals. Always check zoning laws before applying.

Homeowners Association (HOA) & Local Restrictions: Many HOAs and cities have strict rules regarding short-term rentals. Always check zoning laws before applying.

![]() Seasonal Market Risks: Properties in ski towns may have inconsistent rental income, which could affect DSCR calculations.

Seasonal Market Risks: Properties in ski towns may have inconsistent rental income, which could affect DSCR calculations.

![]() High Personal Debt: While DSCR loans don’t rely on DTI ratios, excessive personal debt might impact your loan terms.

High Personal Debt: While DSCR loans don’t rely on DTI ratios, excessive personal debt might impact your loan terms.

The most profitable short-term rental markets have high tourist demands and strong occupancy rates. 2 of the best markets include:

Phoenix attracts a steady stream of visitors due to its corporate travel market, major sporting events, and year-round warm weather. It has an average daily rate (ADR) of $235.7 and an occupancy rate of 55 %. Investors can expect an annual revenue of approximately $19.8K per property.

Phoenix attracts a steady stream of visitors due to its corporate travel market, major sporting events, and year-round warm weather. It has an average daily rate (ADR) of $235.7 and an occupancy rate of 55 %. Investors can expect an annual revenue of approximately $19.8K per property.

Gatlinburg remains one of the highest cash-flow markets for short-term rentals, thanks to consistent tourism and strong demand for vacation cabins. With an ADR of $328.3 and an occupancy rate of 58 %, you can generate an annual rental income of almost $47.3K.

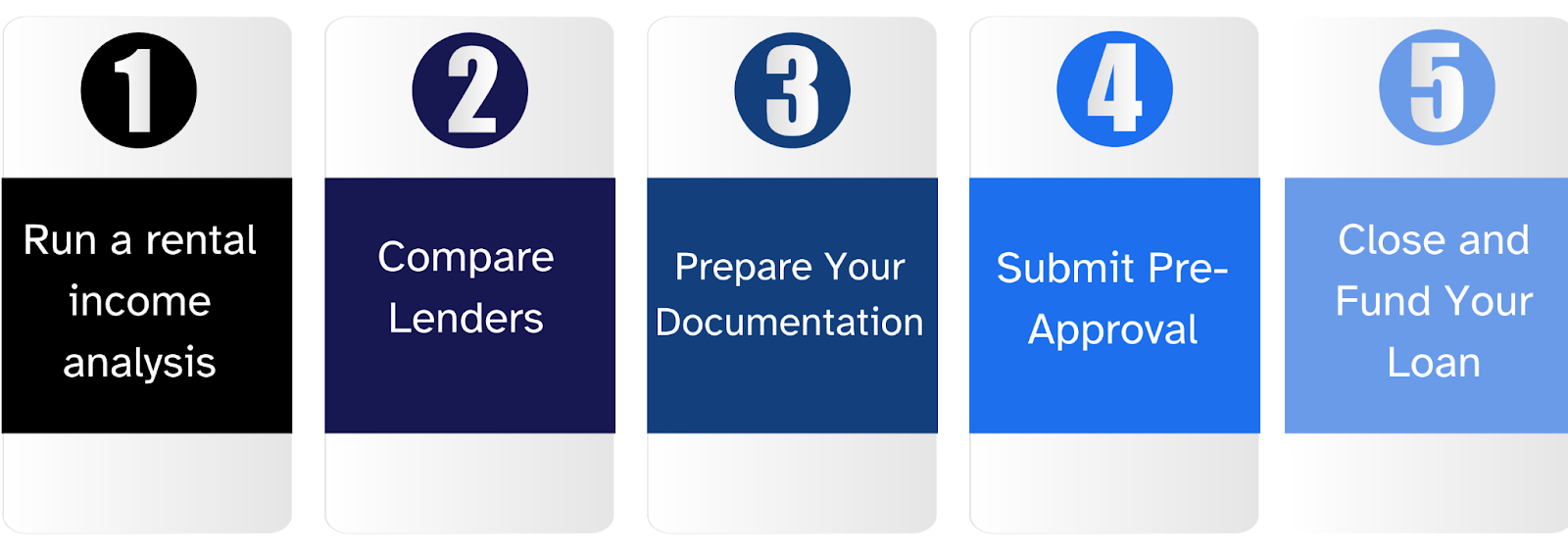

Here are 5 simple steps you can follow to increase your chances of approval.

Lenders want to see whether your property can generate sufficient income to cover the mortgage. You can use tools to estimate:

Once your property is operating, tools such as FreshBooks invoicing can also help you document incoming payments and monitor cash flow more accurately.

Since not all lenders will offer you the same terms, it’s essential to shop around. Your two main options include:

Lenders will require you to have your basic documentation ready to verify your eligibility. Make sure you’ve got these documents at hand:

Once you’ve chosen your lender, you need to submit your pre-approval application. Many DSCR lenders offer pre-approvals in as little as 72 hours.

After approval, your lender will finalize the loan. On average, closing and funding take 14–21 days.

Once the loan is funded, you’re ready to start renting out your property and earning income.

Most investors overlook this, but investing in STR loans comes with significant tax benefits. These include:

One of the biggest advantages is that you can deduct mortgage interest from your taxable income.

Since rental properties lose value over time, the IRS allows you to deduct depreciation as an expense.

Most investors don’t realize they can accelerate depreciation through a cost segregation study.

Instead of spreading deductions over 27.5 years, a cost segregation study breaks the property into different asset classes, allowing you to deduct more expenses upfront.

A 1031 exchange allows investors to defer capital gains taxes when selling one rental property and reinvesting in another.

While DSCR loans are a great choice for many investors, they may not always be the right fit. Other options include:

A HELOC allows you to borrow against the equity in an existing property and use the funds for your short-term rental investment.

Here's how you get personal loan: If you have strong credit (700+), a personal loan can be a quick way to access funding for property improvements or closing costs.

Real estate crowdfunding platforms like Fundrise allow investors to raise capital from multiple backers. You can also seek private investors to help finance your property.

Many investors assume they need a large amount of savings to buy a short-term rental, but that’s not always the case.

Alex, a self-employed entrepreneur in Miami, wanted to enter the Airbnb market. He didn’t have traditional W-2 income, so instead of waiting to save up, he leveraged DSCR loans to acquire three short-term rentals with $0 out-of-pocket.

Here’s how he did it:

Yes, but your options may be limited. Most DSCR loan lenders require a credit score of at least 620. You may qualify for a hard money loan instead.

This depends on the lender. Some require investors to have a professional property management company, while others allow self-management as long as you can show consistent rental income.

Yes. Most lenders allow refinancing, but many require a 6–to–12–month seasoning period before you can convert your existing loan into a new one.

DSCR loans make financing short-term rentals easier, but understanding the requirements and risks is crucial.

Ready to secure financing for your short-term rental? Apply for a loan with Truss Financial Group now!

Take your pick of loans

Experience a clear, stress-free loan process with personalized service and expert guidance.

Get a quote

10 min

.png?width=352&name=Blog%20covers%20(8).png)

15 min

7 min

Discover your borrowing power and plan your mortgage journey with knowledge on your side.

Get a quoteGet a quote in 3 easy steps

Tell us what you want

Fill out our online form to help us understand your financial situation and loan needs.

We get to work for you

We review your info and look for competitive rates that match your specific goals.

You get a personalized quote

You’ll receive a customized rate quote that meets your unique profile.