15 min read

15 min read

Suppose you’re a high-net-worth individual, retiree, or self-employed borrower with significant assets but limited traditional income. In that case, you may have wondered how to qualify for a mortgage without a steady paycheck.

The answer you’ve been looking for is an asset depletion mortgage. It allows you to qualify based on your liquid assets rather than your income. Lenders calculate your qualifying monthly income by dividing your savings, retirement accounts, or investment portfolios over a set period.

By the end of this guide, you’ll understand how asset depletion mortgages work, who they’re best for, and whether this loan type is right for you.

____________________________________________________________________________

![]() An asset depletion mortgage allows borrowers to qualify based on their liquid assets rather than traditional income sources like W-2s, pay stubs, or tax returns.

An asset depletion mortgage allows borrowers to qualify based on their liquid assets rather than traditional income sources like W-2s, pay stubs, or tax returns.

![]() This type of loan is ideal for retirees, self-employed individuals, and high-net-worth borrowers who have substantial savings but may not have a steady paycheck.

This type of loan is ideal for retirees, self-employed individuals, and high-net-worth borrowers who have substantial savings but may not have a steady paycheck.

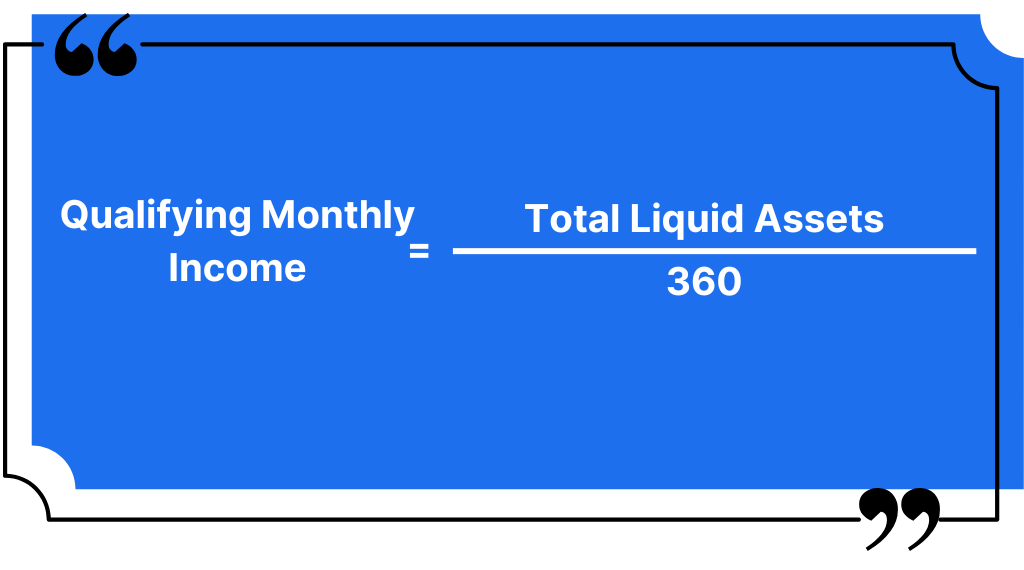

![]() Lenders calculate qualifying monthly income by dividing total liquid assets by 360 months (for a 30-year loan), providing a structured way to determine eligibility.

Lenders calculate qualifying monthly income by dividing total liquid assets by 360 months (for a 30-year loan), providing a structured way to determine eligibility.

![]() Eligible assets include cash, savings accounts, retirement funds, stocks, and bonds, though some may be discounted based on liquidity and lender guidelines.

Eligible assets include cash, savings accounts, retirement funds, stocks, and bonds, though some may be discounted based on liquidity and lender guidelines.

![]() Asset depletion mortgages can be used for primary residences, second homes, and investment properties, but loan terms and down payment requirements vary by lender.

Asset depletion mortgages can be used for primary residences, second homes, and investment properties, but loan terms and down payment requirements vary by lender.

____________________________________________________________________________

An asset depletion mortgage is a non-qualified mortgage (non-QM loan) that allows you to qualify for a home loan based on your liquid assets rather than traditional income sources like pay stubs, W-2s, or tax returns. This type of loan is ideal for individuals with substantial assets but irregular or limited employment income.

You don’t need to provide W-2s, pay stubs, or tax returns to prove income.

Lenders calculate qualifying monthly income by dividing your savings, retirement accounts, or investment portfolios over a set period (typically 360 months for a 30-year loan).

Commonly used by retirees, self-employed individuals, and high-net-worth borrowers who may not meet the income requirements of traditional loan programs but have substantial assets.

This loan program provides an alternative financing option for those with strong financial reserves who don’t meet conventional loans' standard income verification requirements.

Asset-based mortgages are an excellent option for retirees, self-employed individuals, and high-net-worth borrowers who have significant assets but may not have a steady paycheck. Here are some of the most important benefits:

Unlike conventional loans, asset depletion mortgages don’t require W-2s, pay stubs, or tax returns. This is especially beneficial for retirees living off savings or entrepreneurs with fluctuating incomes who might struggle to meet traditional income qualifications.

Instead of focusing on employment income, lenders calculate qualifying monthly income by dividing your savings, retirement accounts, or investment portfolios over a set period. This allows you to leverage your wealth rather than provide consistent earnings.

These loans can be used for primary residences, second homes, or investment properties, giving you more freedom to purchase or refinance based on your financial goals.

Since qualification is based on total assets rather than income limits, borrowers with substantial assets may qualify for larger loans than they would under conventional financing. This is especially useful for those looking to purchase high-value properties or secure better loan terms.

An asset-based mortgage is designed for borrowers with significant assets but may not have steady employment income. Instead of examining pay stubs or tax returns, lenders assess liquid assets to determine eligibility.

Those with large retirement savings but no regular paycheck can qualify through their retirement accounts, savings, and investments.

Entrepreneurs and freelancers with irregular income streams who might not meet traditional income requirements.

Investors, business owners, and professionals with substantial liquid assets but limited documented income.

Borrowers must have significant savings, investment accounts, or retirement funds that can be used to cover mortgage payments.

Most lenders require a minimum credit score of 620–680, though higher scores can lead to better loan terms and lower interest rates.

While DTI is less important for asset depletion loans, some lenders still evaluate it to ensure borrowers can manage their overall debt obligations.

Lenders typically calculate qualifying income by dividing a borrower’s total liquid assets by a set period (often 360 months for a 30-year loan). This makes asset-based mortgages a great solution for those with wealth but without a traditional paycheck.

Lenders use a simple formula to calculate a borrower’s qualifying monthly income based on their liquid assets.

If a borrower has $1 million in liquid assets:

1,000,000 / 360 = 2,777

This means the lender would consider $2,777 per month as the borrower’s income for mortgage qualification.

Lenders may apply different discount rates based on the asset type to ensure borrowers have sufficient funds for the loan term.

An asset depletion mortgage offers a more flexible way to qualify for a home loan, especially for those with substantial assets but limited traditional income.

In contrast, a traditional loan program relies on steady employment and documented income for approval.

Below is a side-by-side comparison of the key differences.

While an asset-depletion mortgage provides an alternative to homeownership, borrowers should be aware of potential downsides before applying.

Since asset depletion loans fall under non-QM (non-qualified mortgage) loans, they typically come with higher interest rates than conventional mortgages. Lenders charge more due to the lack of traditional income verification, making it important for borrowers to compare rates and assess affordability.

Some lenders may impose higher down payments (often 20%–30%), require larger cash reserves, or have shorter loan terms compared to conventional loans. Borrowers should be prepared for stricter approval criteria and fewer lender options.

Not all mortgage lenders offer asset depletion mortgage programs, so finding a lender may take more time. You may need to look for specialized lenders or private mortgage providers that cater to high-net-worth individuals or those with substantial liquid assets.

Using savings, retirement accounts, or investment funds to qualify for a mortgage could affect long-term financial security. Depleting assets for home financing may reduce liquidity, affect investment growth, or require adjustments to retirement plans. Borrowers should weigh the impact on their overall financial strategy before committing.

Understanding these risks ensures you make an informed decision that aligns with your financial future.

Applying for an asset depletion mortgage is different from the traditional mortgage process.

Here’s a step-by-step guide to help you navigate the process:

Since asset depletion loans rely on bank accounts, retirement savings, and investments, you’ll need to provide detailed documentation of your liquid assets.

The documents you’ll need include:

Having these documents ready will streamline the process and show lenders you have the necessary assets to cover the mortgage payments.

Not all mortgage lenders provide asset depletion loans, as they fall under the non-QM (non-qualified mortgage) category. Since these loans have different underwriting guidelines, it’s important to:

Once you choose a lender, you’ll need to complete the mortgage application and submit documentation for review.

Lenders will evaluate:

Demonstrating strong financial reserves and responsible asset management is crucial for approval.

Once approved, the lender will provide a loan estimate and final closing disclosure detailing the following:

At closing, you will review and sign the final paperwork. Once everything is completed, the lender will fund the loan. You are now officially a homeowner!

Yes, many lenders allow asset-depleting mortgages for investment properties, but the loan terms, down payment requirements, and interest rates may be different from those for primary residences.

Lenders typically accept cash, savings, retirement accounts (401(k), IRAs), stocks, bonds, and mutual funds. However, some assets may be discounted based on liquidity (e.g., retirement funds are often counted at 70–80% of their value).

Yes, most lenders require a down payment of 20–30%, though higher loan amounts or lower credit scores may require a larger mortgage payment.

Yes, if you meet the eligibility requirements, you can refinance an existing mortgage into an asset depletion loan. This is a good option for self-employed individuals, retirees, or high-net-worth borrowers who want to use their assets, such as mutual funds, instead of employment income to qualify.

Yes, you can use an asset depletion mortgage to finance a second home or vacation property, but lenders may have stricter requirements for credit scores, down payments, and asset reserves.

An asset-depletion mortgage is an excellent option for retirees, self-employed individuals, and high-net-worth borrowers with significant assets but limited traditional income.

While higher interest rates, down payment requirements, and lender availability are important considerations, an asset depletion mortgage provides flexibility for those who may not meet the strict income requirements of a traditional mortgage.

Are you ready to explore your financing options?

Contact Truss Financial Group today to learn more about asset depletion mortgages and how they can help you achieve your homeownership goals.

Take your pick of loans

Experience a clear, stress-free loan process with personalized service and expert guidance.

Get a quote

16 min

3 min

-1.png?width=352&name=Blog%20covers%20(4)-1.png)

16 min

Discover your borrowing power and plan your mortgage journey with knowledge on your side.

Get a quoteGet a quote in 3 easy steps

Tell us what you want

Fill out our online form to help us understand your financial situation and loan needs.

We get to work for you

We review your info and look for competitive rates that match your specific goals.

You get a personalized quote

You’ll receive a customized rate quote that meets your unique profile.