10 min read

10 min read

It cannot be very comforting to navigate through a mortgage statement, but once you understand the key components, it can be a potent tool for managing your home loan.

Whether you are a first-time homeowner or someone who’s been paying down a mortgage for years, reviewing your monthly mortgage statements regularly will ensure you’re on top of your mortgage payment breakdown and financial goals.

We’ll cover all the basics and a mortgage statement example so you know exactly what to expect.

A mortgage statement is a detailed document your mortgage servicer issues, usually monthly, which describes the status of your home loan.

It will indicate how your loan principal and interest are allocated, your current mortgage balance, and your payment history record. For those with an escrow balance overview, it will detail contributions for taxes and insurance. All these need to be understood to manage your home loan details well and avoid any surprises.

The important things you ought to know when understanding an example mortgage statement include understanding the details that would help you manage your loan efficiently.

The sections found in a mortgage statement include:

The important things you ought to know when understanding an example mortgage statement include understanding the details that would help you manage your loan efficiently.

The sections found in a mortgage statement include:

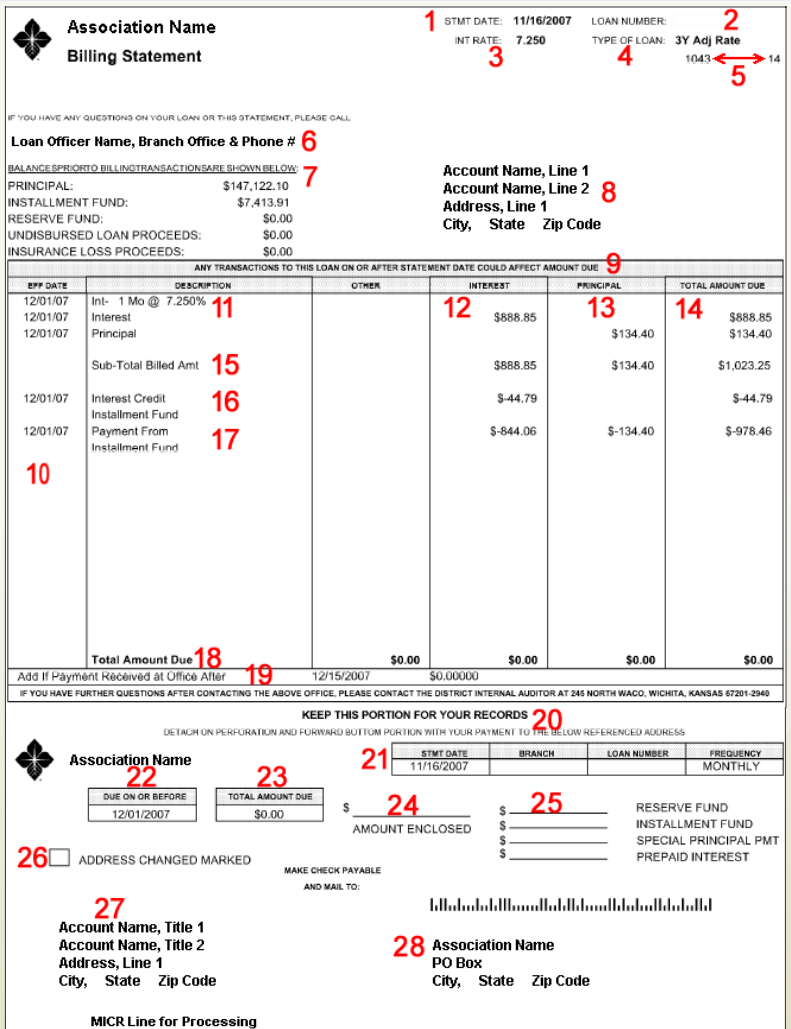

The date your mortgage statement was printed is your statement date. It will thus help you understand where your billing cycle begins.

This section shows you your loan number, which can be used to identify your account. You will use this number if you ever call your servicer for any help.

This section shows how much your mortgage is being calculated. If you have an adjustable-rate mortgage, this rate may change periodically.

Shows the type of loan you have. Some of the common types are a 5-year Adjustable Rate, a Variable Rate, or a Fixed Rate.

This sequence number assures printed statements will be in proper order, and a special handling code can be placed herein to note any specific treatment needed on the account.

The name, branch location, and contact number of the servicing loan officer handling your loan.

This section provides balances as of the statement date, including the outstanding principal amount, which is crucial for understanding mortgage payments and decisions regarding home equity, refinancing, or selling the property. The balances also include amounts for:

This section shows your name and address as recorded in the loan system:

This notice informs you that any transactions between the statement date and the payment due date may impact the amount due on your mortgage.

This column indicates the effective date of each listed transaction. It also includes due dates for amounts owed.

Here, you’ll find information about any interest rate changes on your loan that have occurred since the last billing statement.

The interest column displays interest charges or credits, along with descriptions indicating whether the interest is due or being credited.

This column lists any principal amounts due or credited, with accompanying descriptions to indicate whether they are due or being applied as a credit.

This subheading lists the amount of money due on each, totaling principal, interest, and charges, which may be added as service charges or contributions to escrow.

Reflects the subtotal of the billed amount before adjustments including credits for interest or escrow contributions.

If applicable, this section shows interest credits from your escrow account that will be applied to your payment if not paid by the due date.

Here, the principal amount drawn from your escrow account is shown, applied toward your payment if not paid in full by the due date.

This is the net amount owed, aggregating all interest and principal adjustments. If the sum is $0.00, there is no outstanding payment.

In case your loan payment was delayed, this column shows the late payment fees charged on that loan along with default interest, if there is any such charge. In case a cheque was received post the due date, this column would show the cheque amount with per diem charges for delay in payment also.

This section has a perforated line where you can tear off the bottom portion of the statement for your records, but the top portion is used for the submission of payment.

Here, you will get more information about the statement date and the loan branch, along with the loan number and how frequently you pay.

Here is the due date for your payment. Remit by this date if you wish to avoid late fees or interest charges.

This section repeats the total amount due, which includes all charges for that billing period, as line 18 points out.

Allows you to manually write in the total amount enclosed with the payment coupon when sending a check.

These blank lines enable you to allocate any extra amounts to specific loan categories, such as reserve funds, special principal payments, or prepaid interest.

If you have moved, you can check this box to indicate that your address has changed. There's an area on the back side of the payment coupon where you can provide the new address details.

Shows the borrower's name and address for both the billing statement and the payment coupon:

This section shows the association's name and address, which is aligned to work with a window envelope for easy mailing. It is used to return the payment coupon with your payment.

To understand a mortgage statement example, let’s break it down into digestible sections:

A sample mortgage statement can help illustrate the breakdown of these sections and provide a clear example of what to expect.

Your mortgage statement for mortgage loans will include the mortgage loan number, loan type explanation of fixed-rate or adjustable-rate mortgage, and the current mortgage balance calculation. It may also have important dates, including a mortgage payment schedule and a next-due date.

The most important factor here is the breakdown of what your monthly payment represents and, therefore, how much goes toward paying the principal and interest on the loan versus other costs like adding to your escrow accounts. You may also see if there are fees or adjustments for late payments from past months or changes in your adjustable-rate mortgage. For individuals or businesses managing multiple payments and accounts, using reliable billing software can simplify tracking due dates, automate calculations and ensure you stay updated on your financial records efficiently.

If you have an escrow balance summary, this section shows the funds set aside for property taxes and insurance. Be sure to review this section because any bump in the property taxes or homeowners insurance premiums could raise your mortgage payment or lead to an escrow shortage.

In the case of an adjustable-rate mortgage, your mortgage statement example would thus list the interest rate, the total interest paid, and any upcoming changes based on the loan’s terms. For a fixed-rate mortgage explanation, the statement confirms that your rate is steady throughout the loan term. Understanding loan amortization is crucial to manage your mortgage effectively.

Your mortgage statement is probably one of the most critical aspects of your finances. This is because:

Most lenders now offer online portals for easy access to your mortgage statement template.

Once you log in, you can download both your monthly mortgage statement and annual mortgage statement. Many lenders will mail paper statements if that’s what you want, and you can reach out to customer service to get older statements or to ask for a detailed loan payment summary of a specific period. Using a mortgage statement template excel can help you manage your finances by illustrating tax benefits and potential deductions.

Understanding a mortgage statement is a means of having control over finances.

Reviewing account breakdown mortgage and escrow account contributions including details of loan principal and interest, empowers you to have self-control in making decisions involving your home loan. Making sure to check on your statements regularly keeps you on track with payment history record checks, tracking changes in an interest rate, and avoiding unwanted surprises.

Additionally, if you fall behind by 45 days, you will receive a delinquency notice, which includes details about the outstanding amount, account history, and potential consequences of continued payment issues, such as fees and foreclosure.

A mortgage is a secured loan obtained to buy some property, usually secured through the property itself. The mortgage statement shows the outstanding balance of loans, mortgage payments made monthly, and details on principal and interest.

A mortgage interest statement outlines the interest rate or the interest rate applied to your mortgage. It can be fixed or variable, which influences how the payments of your mortgage are structured over time.

You can get all of your mortgage documents either by logging into your lender's online portal or by requesting paper copies from customer service.

Navigating the details of your mortgage statement can feel overwhelming, but you don't have to go it alone. Our team of experts is here to guide you through the process, ensuring you fully understand every aspect of your home loan. Take the first step toward mastering your financial goals—contact us today!

Take your pick of loans

Experience a clear, stress-free loan process with personalized service and expert guidance.

Get a quote

6 min

5 min

4 min

Discover your borrowing power and plan your mortgage journey with knowledge on your side.

Get a quoteGet a quote in 3 easy steps

Tell us what you want

Fill out our online form to help us understand your financial situation and loan needs.

We get to work for you

We review your info and look for competitive rates that match your specific goals.

You get a personalized quote

You’ll receive a customized rate quote that meets your unique profile.