.png "hero-image")

Do you need help buying a house with your budget but have low credit scores?

Don’t let that hold you back. FHA loans may just be the solution to your financing worries! These loans are designed to help first-time home buyers with limited credit history, offering low down payments and flexible requirements.

Don’t know where to start? Don’t worry, we’ve got you covered.

Everything you should know about FHA Loans is in this article. So, sit back and learn. Your dream house may be closer than you think!

What is an FHA Loan?

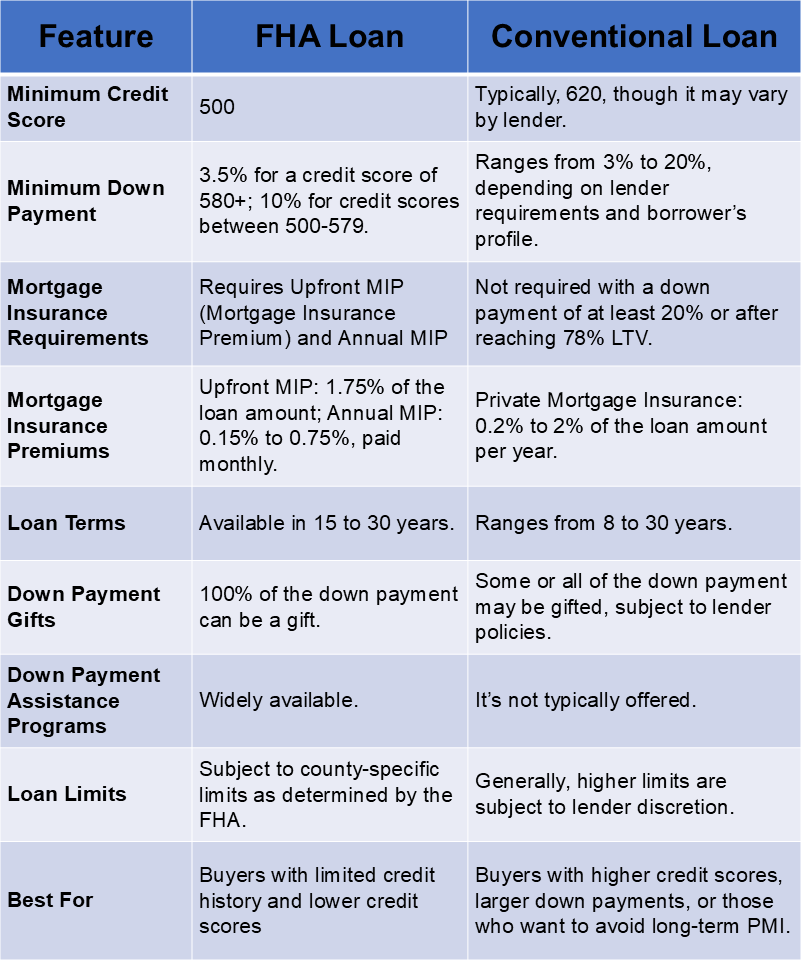

The Federal Housing Administration, or FDA, is a division of the US Department of Housing and Urban Development. It insures the mortgages, but other FHA-approved lenders issue them. FHA loans are typically the best option for first-time homebuyers, especially those with limited savings or credit issues because they require a minimum 3.5% down payment for buyers with a credit score of 580 or higher.

It doesn’t matter that you’ve filed for bankruptcy or don’t fit the standard requirement for a conventional loan, and you can still qualify for an FHA loan. FHA and conventional loans differ significantly in several areas. FHA loans have looser qualification requirements, allowing individuals with lower credit scores or those with credit issues to obtain financing more easily. They also require mortgage insurance regardless of the down payment amount, whereas conventional loans may not require it if the down payment is 20% or more. FHA loans allow down payment gifts from family members, while conventional loans have stricter rules on gift funds. Additionally, FHA loans have specific appraisal standards and potentially higher closing costs. For those with better financial profiles, a conventional mortgage might be more beneficial due to potentially lower interest rates and the possibility of avoiding mortgage insurance.

Who Issues FHA Loans?

The federal government insures FHA loans, although they are not issued by it. They are issues by FHA-approved lenders, such as:

- Banks

- Credit Unions

- Non-banks; Private lenders.

Types of Homes Financed by FHA

Many different kinds of houses can be bought or refinanced with an FHA home loan, including:

- Single-family homes.

- Multifamily residences with two to four units.

- Condominiums.

- Certain manufactured homes (that are fixed on a solid base)

However, all properties, whether old construction or new, must be appraised and approved by FHA. So, you can purchase or refinance your home with an FHA loan as long as it fits the federal requirements.

.png?width=608&height=342&name=image%20-%202025-01-22T162745.660%20(1).png)

How Does an FHA Loan Work?

With a federal loan, you can borrow up to 96.5% of the home's value if your credit score is at least 580, which implies that a mere 3.5% down payment is needed.

Yet this doesn’t mean you can’t obtain the loan if your credit score is between 500-579. You’d just have to pay at least 10% of the downpayment.

Moreover, a borrower can cover the downpayment by using savings, a cash gift from a family member, or even use the down payment assistance programs.

FHA Loan Requirements in 2024:

For borrowers looking to apply for an FHA loan, the FHA establishes minimal standards. Each FHA-approved lender is free to develop its underwriting guidelines, provided that they adhere to the FHA's minimal requirements.

These are the standard requirements to keep in mind when applying for an FHA loan:

1. Credit Score and Downpayment Requirements

FHA has flexible credit requirements. This means that borrowers with credit ratings as low as 500, which falls into the "poor" area for a FICO score, can still apply for FHA loans.

So, if you are capable of paying a down payment of at least 10%, you might be able to get an FHA loan if the credit score you have is between 500 and 579. You can also pay a downpayment of just 3.5% if your credit score is 580 or higher.

2. Debt-to-income Ratio

What exactly is the DTI ratio? Well, It's your monthly debt payments divided by your pre-tax income, aside from things like credit card debt and student or car loans, that also includes your rent or mortgage payments.

When it comes to loan issuance, lenders generally prefer borrowers who have a lower DTI ratio. The FHA typically wants a DTI of less than 43% if your credit score falls between 500 and 579.

- With a DTI of more than 50%, you can still qualify for an FHA loan, but your loan options will be restricted, and you will need to fulfill compensatory factors.

3. Steady Employment Verification

Since mortgages need to be paid back, the FHA-approved lender will demand proof that the potential borrower can do so. The borrower's current and steady employment is a crucial factor in assessing their ability to fulfill their obligation. W-2s, Pay stubs, and tax returns can serve as proof of this.

If you are self-employed, you can still qualify for a FHA loan but there’s a condition. The condition is that you should have a two-year prior experience in the same or related field that you are self-employed in currently. Provided also that you've been self-employed for more than a year.

4. Income

In general, the front-end ratio is the cost of mortgage payments, the tax on your property, the MIP, and any other fees on your homeowners’ insurance against your gross income, and it shouldn’t be more than 31% of your gross income.

While your mortgage payment and all other monthly consumer bills should be less than 43% of your gross income. Also known as the back-end ratio.

5. Mortgage Insurance

Homeowners who obtain loans guaranteed by the Federal Housing Administration (FHA) are required to pay mortgage insurance premiums (MIP) as a protective measure against defaults. MIPs are used by FHA-backed lenders to safeguard themselves against borrowers who pose a greater risk of loan failure.

Every FHA loan has an annual premium of 0.15% to 0.75% in addition to an upfront cost of 1.75% of the loan amount. Premiums must be paid in full at the time the loan is issued.

The length of the loan, the amount borrowed, and the loan-to-value ratio (LTV) are used to calculate the precise annual cost.

6. Property Requirement

The property you’re trying to buy with an FHA loan must fulfill FHA minimum requirements for property and be appraised by a professional who the FHA has approved.

A property inspection is not the same as an FHA appraisal. In addition to making sure the house satisfies fundamental safety and livability requirements, the objective is to make sure the house is a good investment or worth the money you're paying for it.

.png?width=608&height=342&name=image%20-%202025-01-22T162852.716%20(1).png)

FHA Loan vs. Conventional Loan

When choosing the best loan option, understanding the key differences is crucial. Here’s a comparison between a FHA loan and conventional loans. Conventional mortgages are not government-insured and are typically preferred by borrowers with good credit and strong financials. They offer advantages such as lower interest rates and fewer insurance requirements compared to FHA loans, catering to those who can afford a larger down payment and meet stricter qualifications.

FHA Loan Rates and Costs:

Although FHA offers affordable loan rates to borrowers. However, there are other negotiable and non-negotiable expenses associated with them, such as Mortgage Insurance Premiums (MIP) and other charges...

Common Myths and Misconceptions About FHA Loans:

Let's debunk some of the myths surrounding these loans.

Higher Interest Rates:

- Myth: FHA loans tend to have higher interest rates.

- Fact: FHA loans often have lower interest rates than conventional loans. However, the annual percentage rate (APR) may be higher due to the cost of FHA mortgage insurance.

Poor Financial Decision:

- Myth: FHA loans are a poor financial decision.

- Fact: FHA loans offer affordable rates and flexible requirements, making them a wise choice for those with both low and high credit scores. They also help buyers reduce their down payment to protect cash reserves.

How to Apply for an FHA Loan: A Step-by-Step Guide

Applying for an FHA loan may seem overwhelming, but it's simple if you follow these steps:

1. Selecting a Lender

Search for lenders online, compare their offers, and read reviews. Choose a mortgage lender experienced with FHA loans to simplify the process.

2. Gather the Necessary Documents

Organize these documents to streamline your application process:

- Government-issued ID and Social Security number

- Pay stubs, W-2s, or tax returns from the past two years

- Proof of consistent employment for at least two years

- Credit report

- Bank records or proof of savings for the down payment and reserves

3. Preapproval and Prequalification

Prequalification helps estimate your borrowing capacity based on credit and income, while preapproval is a more formal process where the lender verifies your financial details and issues a preapproval letter.

4. Apply for the Loan

Submit your application, documents, and any applicable fees to the lender.

5. Underwriting and Approval

The lender’s underwriting team will assess your financial profile and the chosen property to confirm eligibility.

6. Closing the Loan

Sign the final loan documents, pay any closing costs, and receive the keys to your new home!

FHA Down Payment Assistance Programs

FHA loans offer flexible down payment requirements, but assistance programs can help borrowers cover down payments and closing costs. These programs are provided by state or local agencies.

Visit the FHA website or consult your lender to explore available assistance programs.

Pros and Cons of FHA Loans

FHA loans are a great option for borrowers who may not qualify for conventional loans, but they come with their own pros and cons:

Pros

- Flexible credit score requirements

- Low down payment requirements

- Federally backed

- Accessible to both first-time and repeat buyers

Cons

- Higher interest rates

- PMI required for the loan’s duration

- Doesn’t apply to second homes or investment properties

- Strict property requirements

.png?width=608&height=343&name=image%20-%202025-01-22T162933.177%20(1).png)

Conclusion

FHA loans are an excellent option in 2024 for first-time homebuyers and those with less-than-perfect credit. Despite additional costs like mortgage insurance, the benefits often outweigh the drawbacks.

Ready to explore your options? Contact Truss Financial Group to begin your journey toward homeownership. Their team can guide you through the FHA loan process and ensure the best terms for your dream home.

Make your homeownership dream a reality with Truss Financial Group!

FAQs

Is it hard to qualify for a FHA loan?

It generally takes a great effort and time to get any kind of loan, but comparatively FHA loan is easier to qualify for than a conventional loan. However, if the pandemic and the state of the economy, specific requirements for FHA have changed, so the FHA lenders can ask for a higher minimum credit score than they previously would.

What is the maximum amount of loan you can get with FHA?

The amount depends on the area where your property is and your ability to pay back the loan. However, in 2024, the FHA ceiling for single-family home loans was set at $1,149,825.